Shire made a $30bn (£19bn) hostile takeover bid for Baxalta.

Industry overview

Shire is a London-listed drug company, with tax domicile in Ireland and Jersey. Shire develops and provides healthcare in the areas of behavioral health, gastrointestinal conditions, rare diseases, and regenerative medicine. Its main business lies in the area of Attention Deficit Hyperactive Disorder (ADHD) – with brands such as Adderall, Vyvanse, and Intuniv, gastrointestinal dysfunctions – with brands such as Lialda and Pentasa – as well as the Hunter Disease. In 2014, it has been nearly taken over by Illinois-based competitor AbbVie. This proposed $54bn takeover of Shire by AbbVie failed due to recent reforms by the Obama administration aimed at curbing the tax inversion trend in the pharmaceutical sector (i.e. whereby American companies re-domicile abroad for tax reasons). AbbVie was forced to pay a $1.6bn break fee at that time.

During the past years, Shire has made a series of successful acquisitions: it bought New River Pharmaceuticals for $2.3bn in 2007, Viropharma in 2013 ($4.2bn), and NS Pharma in 2015 ($5.2bn). Furthermore, Shire announced plans to acquire the biotech company Biotherapeutics for $300m.

In Q2 2015, Shire reported revenues of $1.6bn, a growth of 11% compared to Q2 2014. The net income in Q2 2015 was $160m.

Baxalta is a rare-disease specialist drug maker, based in Illinois, producing drugs for blood disorders and rare cancers. Its main areas of focus are Hematology, Immunology, and Oncology. In July 2015, the company was created as result of a spin-off from Baxter International, a large US-based producer of Bio Science and Medical Products. Baxter is currently the largest shareholder of Baxalta. However, this recent spin-off is depressing its share price and consequently it is very likely that it will outperform Shire’s valuation (i.e. $30bn) within the near future.

Timeline

On July 1, 2015 Baxalta – the former BioScience division of Baxter International – was created as result of a spin off from the latter. The first proposal by Shire to acquire Baxalta was made on July 10, 2015 and was rejected by Baxalta. This offer was based on a per share value of $45.23 resulting in an enterprise value of $33.9bn. After the rejection, Shire decided to approach Baxalta’s shareholders directly convincing them of the growth potential of the combined entity.

Deal terms

Initially, Shire announced it was ready to pay $45.23 (£28.96) per Baxalta share, a 36% premium on Baxalta’s stock price. Subsequently, Shire’s all-stock offer has fallen in value to around $42 per share. This is equivalent to a deal value of $30bn and a premium of nearly 27% on Baxalta’s share price on August 3, which contrasts an average premium of 50% seen in other recent biotech M&A deals. This proposal values Baxalta at only 5x 2015 sales, which is significantly below the median of 7.2x in the healthcare industry over the past decade.

According to Bloomberg analyst Asthika Goonewardene “Hostile bids typically come with a premium to entice shareholders, so Shire’s offer suggests it may concede that Baxalta is a lower-quality asset”.

Shire has structured its offer as an all-stock transaction for tax reasons but plans to return some cash to Baxalta shareholders via a share buyback after the deal is completed.

On the one hand, Shire’s options are constrained by its inability to “sweeten” the proposal with cash, because this solution would risk tax costs related to Baxalta’s recent spin-off from Baxter. On the other hand, Shire is constrained by the wariness of its own shareholders over any dilution coming from an all-stock deal.

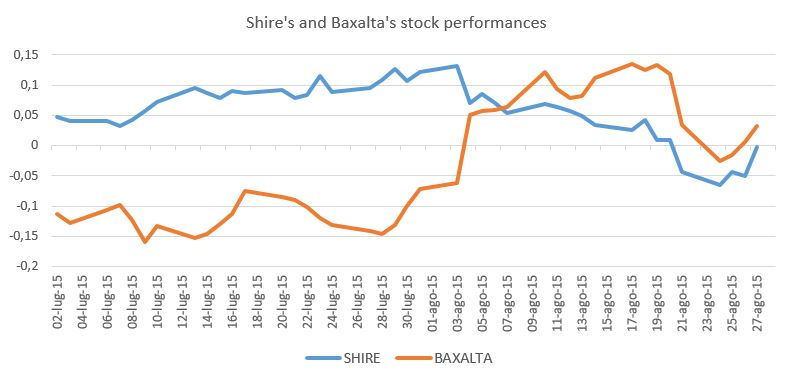

Shire shares are down 10% since the possible takeover has been announced. The drop is from an all-time peak, however, and the stock price is still three times higher than when the current CEO, Mr Ornskov, took office in 2013. This share price drop can be interpreted as a sign that investors are not convinced of the success of the transaction.

Shares in Baxalta jumped almost 6% by the close to $39.79, following reports in the British media that suggested the company’s board was leaning towards entering talks with Shire at some point this week.

Deal drivers

Deal drivers

The deal is in line with the recent consolidation trend in the pharmaceutical sector, which sees companies racing to discover new medicines and innovative medical treatments, before current pipelines and patents expire. This sums up in a high consolidation pressure in the healthcare industry due to rising R&D costs and expiring patents, which is why we have observed so many M&A activity in the pharmaceutical sector during the last months.

If the deal was concluded by the target accepting the offer without putting in place antitakeover measures, one of the world’s biggest makers of rare disease drugs would be created. As a direct consequence, Shire would get closer to the top 20 of global pharmaceuticals groups. Shire claimed that merging the two companies would create “the global leader in treating rare diseases” with estimated combined sales of $20bn by 2020. The field of rare disease treatment is a very attractive business segment and one of the fastest growing areas in the pharmaceutical industry. The new business combination should have projected “double-digit top-line growth” according to Shire. Furthermore, the deal should be accretive to earnings with a breakeven in year one with accretion thereafter, supported by a share buyback program. Also, the returns would be very attractive according to Shire, which expects an IRR of around 10%.

Moreover, more than 30 new product launches are planned with more than $5bn sales potential by 2020. Hence, the future outlook of the combined entity would be strong with a solid balance sheet and stable cash flows to support the M&A activity.

The two companies also share a similar vision of providing innovative medicines to patients with rare diseases. The companies have complementary strengths with Shire bringing experience and high performance and Baxalta contributing with market leadership in rare diseases and oncology as well as a global presence. The aim is to create the number one platform for rare diseases supported by innovation and growth.

One of the drivers behind the proposal is Shire’s ability to lower Baxalta’s tax bill sharply because of the location of the former’s official headquarters in Ireland. Shire wants to move beyond its best-selling treatment for attention deficit hyperactivity disorder into high-margin niche drugs. Therapies for rare conditions such as Hunter syndrome and Fabry disease accounted for 40% of Shire’s $6bn of revenues last year and make up 75% of its R&D pipeline. “The combined entity would have the opportunity to create significant shareholder value in one of the most attractive and fastest-growing segments in healthcare,” stated Shire’s chief executive, Flemming Ornskov. “Together, the companies would be projected to deliver $20bn in product sales by 2020, with the financial and operational firepower to fuel further innovation and growth in rare diseases.”

However, according to Mr Ornskov, the main rationale is strategic. Baxalta, for its part, has continued to argue that Shire’s “lowball” opening shot is not a realistic basis for negotiation and sees stronger growth prospects for itself as a standalone group. Baxalta has accused Shire of opportunism by targeting the company immediately after its spin-off from Baxter and before it had the chance to demonstrate its potential as a standalone company. Baxalta believes that apart from the two companies being manufacturers of pharmaceuticals to treat rare diseases there is little overlap between the companies and thus little potential for synergies. Baxalta focuses mainly on plasma technologies, whereas Shire also uses other biopharma methodologies. These different segments are not easy to combine in a cost efficient way.

However, Baxalta’s stand-alone prospects are much rosier according to CEO Ludwig Hantson. The company is aiming to launch 20 new products by 2020, generating more than $2.5bn in risk-adjusted sales. Its infrastructure and manufacturing “will provide an excellent platform to grow value,” too, Hantson said.

Despite the reluctance of Baxalta’s management to accept the offer, Shire claimed to continue with the transaction. However, in order to reopen the negotiations, Shire needs to go well beyond its recent offer of $30bn.

Evercore and Morgan Stanley are financial advisors for Shire, while Ropes & Gray and Slaughter and May are legal counsel.

To contact the authors:

Giorgia Caruso giorgia.caruso@studbocconi.it

Alexandra Heidemann alexandra.heidemann@studbocconi.it

You must be logged in to post a comment.