On the 8th of April, Mediaset agreed to sell its pay-tv business to the European media conglomerate Vivendi, creating a partnership that is set to trigger the long-awaited consolidation in the industry. In this article, we took in consideration the main drivers of the deal, verifying coherence with industry trends, underlining the structure and trying to define major implications for the Italian industry.

Mediaset

Mediaset (MIB: MS IM) is a multinational media group listed on the Milan Stock Exchange, and mainly operating in the television industry in Italy and Spain. In Italy, Mediaset has two main areas of business:

- Integrated television operations which consist of commercial television broadcasting over three of Italy’s biggest general interest networks (Rete 4, Canale 5, and Italia 1) and a widespread portfolio of thematic free-to air and pay-tv channels (e.g. Mediaset Premium)

- Network infrastructure services and management through the 40.1% holding in EI Towers, the leading independent tower operator in Italy, engaged in network infrastructure management and delivery of electronic communication

In Spain, Mediaset is the main shareholder in Madrid-listed Mediaset España, which is the leading Spanish commercial television broadcaster with two main general interest channels (Telecinco and Cuatro) and six free-to-air thematic channels.

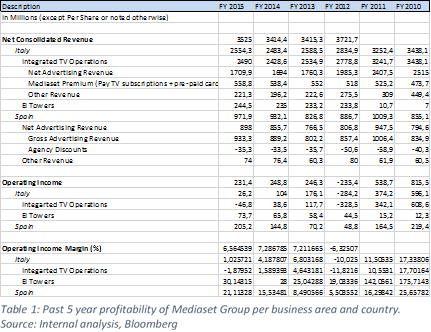

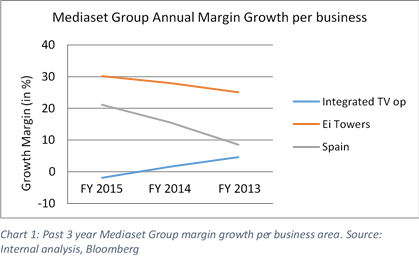

Mediaset Group experienced a fall in EBIT/Net Revenues during the years 2011-2014 due to the challenges it is facing, such as the appearance of online service providers, which could make the system of commercial television broadcasting obsolete. However, over the past two years, the group has been showing signals of financial recovery, sustained by a positive turnaround in EBIT/Net Revenues. In fact, Mediaset has heavily invested in new services, such as Infinity TV, an online platform to deliver on-demand content. Furthermore, Mediaset has strengthened its commercial television broadcasting and pay TV services by acquiring exclusive contents to offer, such as the UEFA Champions League. However, growth does not appear to be solid due to poor performance of some segments, such as the pay-tv service, Mediaset Premium.

Vivendi

Vivendi SA (EPA: VIV) primarily listed and headquartered in Paris, is a multinational mass media company with interests in television, ticket vending, telecommunication, and interactive media. Throughout 2015 Vivendi has divested some non-core investments, including stakes in the Moroccan and Brazilian telecom industries, leaving it with a €6.4bn cash position at the end of 2015. They have currently interests in:

- Universal Music Group (100% ownership), the worldwide largest music corporation international music corporation operating in recorded music, music publishing and merchandising.

- Canal+ Group (100% ownership), is a producer of special-interest channels and a distributor of pay-tv packages, leading in France, Africa, Poland and Vietnam. The group is also involved in producing and distributing feature films

- Vivendi Village (100% ownership), a variety of digital startups offering ticketing, professional recommendation, video-on-demand service and digital radio activities

- Vivendi Content (100% ownership), various studios that aim to develop proprietary content that is earmarked for distribution via Vivendi’s other arms

- DailyMotion (90 % ownership), most visited French website that enables video sharing.

- Various Affiliates, including stakes in Spanish and Italian telecommunication providers and video game developers

Financially the firm has met some challenges in the last few years. The Canal+ Group faces challenged posed by the proliferation of consumption of content online. Same goes for the Universal Music Group with the addition of new forms of consumption, especially music streaming, depressing margins. To counter the decline in operational income, Vivendi has started to invest in new initiatives, whose success is yet to be determined.

Financially the firm has met some challenges in the last few years. The Canal+ Group faces challenged posed by the proliferation of consumption of content online. Same goes for the Universal Music Group with the addition of new forms of consumption, especially music streaming, depressing margins. To counter the decline in operational income, Vivendi has started to invest in new initiatives, whose success is yet to be determined.

Vivendi has been a major play in the media for quite some time; now, however, it is facing pressure on its business model, forcing the company to adapt quickly in sectors where it was traditionally dominant.

Financially, also the other parts of Vivendi performed well, enabling the company to end the year on a positive note with double-digit EBIT growth.

The company is most renowned for its stakes in Universal Music Group® and Canal+ Group®. Together these powerhouses have produced a wide range of media including classic movies such as “A Beautiful Mind” and more modern, popular music like Taylor Swift. Now, however, streaming of music and videos puts pressure on Vivendi’s business model, forcing the company to adapt quickly in sectors where it was traditionally dominant.

Industry Overview

Pay-Tv in Italy

In Italy there are 25 million families, of which around 7 million have subscribed to a pay-tv service. Pay TV services were introduced in Italy at the beginning of the ’90s when the platform Tele+ was created. A few years later, Stream TV started competing with Tele+ until they merged in 2003 giving birth to Sky Italia. In 2005, Mediaset launched Mediaset Premium and it became the main competitor of Sky Italia.

Currently Mediaset Premium lags behind Sky Italia, with 2.0 million and 4.7 million customers respectively at the end of 2015.

Video-on-Demand in Italy

In 2009, Telecom Italia launched Cubovision (now known as TIMvision), the first IPTV (Internet Protocol Television) in Italy. The IPTV system consists of transmitting television services using the Internet, instead of the traditional terrestrial and satellite formats (DTH – Direct-to-Home TV), and it is mainly used to offer VoD (Video on Demand) services including films, TV series, etc., which can be watched on any device, wherever and whenever. In 2011, Fastweb launched ChiliTV, in 2013, Mediaset launched Infinity, in 2014, Sky Italia lunched Sky Online, and finally in October 2015, Netflix, the U.S. giant, arrived in Italy. It is estimated that 1.5 million families have already subscribed to VoD services in Italy.

Trends and Challenges

The success of the VoD represents the main challenge for Pay-TV providers, in fact, customers are increasingly interested in viewing their favourite programs on mobile devices on the go and the VoD services provide the flexibility that customers are looking for. In order to adapt to the growing demand for VoD services, the main Italian providers of Pay-TV services (Sky and Mediaset) launched new VoD platforms (Sky Online and Infinity). However, the penetration of the VoD market is not easy as there are two main challenges: the competition of U.S. giants, such as Netflix, Google Play and Amazon and the necessary development of the ultrabroadband infrastructure in Italy. In fact, the IPTV technology requires a very fast Internet connection (at least 30 Mbps) while the average broadband speed in Italy is just 11.6 Mbps. In April 2015, Telecom Italia and Sky Italia signed a partnership to provide the services of Sky using the broad and ultrabroad bands of Telecom Italia and in August 2015, Telecom Italia signed a similar partnership with Mediaset: two important steps towards Media-Telecom convergence in Italy. From this perspective, the acquisition of Mediaset Premium by Vivendi could offer interesting opportunities in terms of tv-tlc convergence, since Vivendi already owns around 25% of the shares of Telecom Italia.

Terms and Structure

The deal is intended to create an alliance and takes the form of a swap of 3.5% of the equity of each of the two parties as shown in the diagram and explained below:

Vivendi will exchange 0.54% of its share capital in the form of new or treasury shares (with an estimated value of €136m) in return for 3.5% of Mediaset (worth €143m) [1]. Simultaneously, Vivendi will transfer 2.96% of its share capital (€745m) to RTI, a fully owned subsidiary of Mediaset, in return for 100% of Mediaset Premium[2].

Vivendi transfers a total value of €880m, while Mediaset transfers €143m plus Mediaset Premium, giving the pay television company an implicit valuation of almost €740m. This figure is 48% above recent analyst valuations but still well below the €900m implied by Telefonica’s investment in January 2015.

The deal, which is expected to close in September, suggests Telefonica will need to sell their 11.11% stake in Mediaset Premium to allow full ownership and control to pass to Vivendi.

Deal Rationale

Pier Silvio Berlusconi, Mediasets’ Vice President and owner of the company, stated in an interview that this is a pure strategic transaction.

Mediaset will acquire three seats into Vivendi’s board (one of them will be hold by Pier Silvio Berlusconi), while selling an operating unit whose growth margin are decreasing. In this exact moment, acquiring veto power in Vivendi is fundamental to create value for its shareholders. In fact:

- technological progress is merging interests between telecom and media, as previously outlined in the industry overview

- the Italian government has just approved investment to speed up the Italian broadband speed network, with a €6bn plan to build a nationwide fiber optic network by replacing the aging copper wires that run into subscribers’ homes

- EiTower (part of Mediaset) is negotiating with the same Telecom Italia to acquire Inwit (which manage the wireless infrastructure in Italy) and Vivendi has a big stake in Telecom Italia

Therefore, influencing the decision-making process has much more positive impact on shareholders’ value than having cash to distribute them.

On the other hand, Vivendi has now the opportunity to pursue its mission, expanding itself on four level:

- Content level. This transaction comes after recent launch of Studio+ and the acquisition of stakes in production laboratories such as Flab Lab, Banijay Zodiak and Can’t Stop media, and shows Vivendi’s real effort to refocus itself on the entertainment industry, adding Mediaset’s Taodue Company and Medusa Film to its collection of companies producing contents. Vivendi is now ready to fight against production houses like Netflix, producer of successful TV series like House of Cards or Orange is the New Black

- Streaming platform level. As technology progresses, the increased broadband speed allows customer to enjoy high definition content with just an internet connection. This explain favorable prospects to Video-on-Demand (VoD) streaming portal. Vivendi is adding Mediaset’s Infinity and Premium Play to its streaming network, formed by Canal Play in France, and Watchever in Germany

- Pay-tv level. Mediaset Premium has 2m subscribers; Vivendi then will reach a 13m customer base in the pay-tv industry, against Sky’s 12m, putting its Canal Plus desirable to companies who want to advertise their products to a broader European community

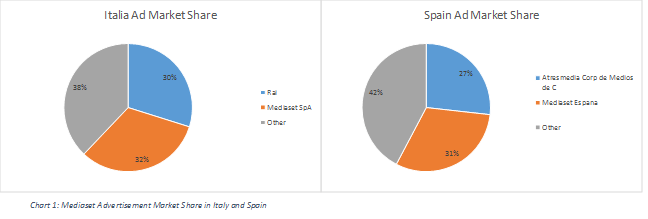

- Advertising market. Mediaset’s revenues are primarily coming from the advertising market, with a 32% market share in Italy and a 30.95% market share in Spain. The two markets have a combined potential value of €5.45B and with this deal, Vivendi is getting a stake of it

Conclusion

The deal, as simple as it seems, creates several scenarios heating the atmosphere within the TMT industry:

- Vivendi could sell its stake in Telecom Italia to Telefonica, as part of the agreement reached with this acquisition, just to make sure that Telefonica will vote in favor of the Inwit sale to Eitower (part of Mediaset)

- Vivendi could sell its stake in Telecom Italia to Orange, raising more cash to fund further acquisition or investments

- Vivendi could retain its stake in Telecom Italia, influencing the decision about Inwit in favor of the Mediaset Group, and then complete takeover of Mediaset in 2019

These scenarios are very different each other but every one of them creates interesting M&A prospects for the European TMT Industry, which is sure to consolidate but still searching for the most creative and profitable way to happen.

_____________________________________________________________

To contact the authors:

Michele Di Paola michele.dipaola@studbocconi.it

Isabella Diplotti isabella.diplotti@studbocconi.it

Harry Blaxland harry.blaxland@studbocconi.it

Niklas Müller niklas.muller@studbocconi.it

Johnathan Riad johnathan.riad@studbocconi.it

You must be logged in to post a comment.