On February 3rd, 2016 ChemChina announced its acquisition of Syngenta’s 100% outstanding share capital at $465 per ordinary share and a special dividend of CHF 5 to be paid only conditionally on the closing of the transaction. The deal comes after several failed acquisition attempts by Monsanto towards Syngenta, declined due to a reportedly too low offer price and more importantly due to a misalignment of strategies between the bidder and the target, which would have harmed Syngenta’s competitive position and long term growth prospects. As reported by Reuters, this deal marks the largest ever attempted overseas acquisition by a Chinese firm. ChemChina is in fact a major player in the M&A market in last months; this latest acquisition would in fact boost its cross border expansion.

Industry Analysis

During the last decade, revolutionary changes in the development of more efficient agrochemicals have been achieved thanks to the enhancements in technology. Moreover, an increase in the adoption rate of innovative products all around the world has augmented the sales value of the agrochemicals market in the recent past.

The global market has been estimated to reach a value of $250.5bn by 2020, with CAGR of 3.2% from 2016 to 2020, being mainly driven by the increasing demand for food together with the growing global population and improving standards in the agricultural farming. Key industry players invest extensively in R&D to expand their product portfolios and to permit the customers to enhance yields. Incessant investments in new product developments, launches, and acquisitions have led to a remarkable growth in the agrochemicals market.

The nature of the agrochemicals market is changing thanks to the entry of large firms via mergers & acquisitions strategies, together with an increasing popularity of genetically modified crops, and increasing pressure on growers to use highly efficient fertilizer products, such as water-soluble fertilizers and controlled-release fertilizers to decrease the cost of crop production. Many large firms have been investing in R&D and have been able so far to subsidize agrochemicals research with resources and revenues from other corporate divisions.

Overall, the global market is marked with intense competition due to the presence of a large number of big and small firms. New product developments, mergers & acquisitions, and expansions are the key strategies adopted by market players to guarantee growth. The main players in the market are: the Israel Chemicals (Israel), Yara International ASA (Norway), The Mosaic Co. (U.S.), BASF SE (Germany), Dow Chemical Limited and Monsanto Co. (U.S.), which collectively account for around 70% of the market share.

ChemChina

ChemChina, the China National Chemical Corporation, is the largest chemical corporation in China and a major player in the chemical industry worldwide. It is a state-owned company. It is not only a chemicals manufacturer but also automobile tyre, pesticide and refined petroleum products manufacturer. More precisely, its product segments are those of agrochemicals, rubber products, chemical materials and specialty chemicals, industrial equipment and petrochemical processing. It is headquartered in Beijing, China, and it has a very well vertically integrated structure, owning production, R&D and marketing systems in almost 150 countries. In the recent past, ChemChina has successfully acquired 9 leading industrial companies in Europe, more specifically in France, United Kingdom, Italy (Pirelli, March 2015, a deal worth $7.7bn) and Germany. The success of its acquisitions lies in the fact that ChemChina keeps investing in the target companies’ development, while trying to maintain their culture in place.

Syngenta

Syngenta is a Swiss agricultural chemicals giant, a world leader in agrochemicals and crop protection, a leading player in the seeds business, committed in the sustainability and enhancement of food security. It manufactures agricultural pesticides and fertilizers products. It is the first company to have introduced integrated solutions for farmers. It is dedicated to rescuing land from degradation, boosting biodiversity and revitalizing rural communities. Syngenta is currently engaged in the development of a remarkable pipeline of innovative crop protection products, which is predicted to have potential total sales of $3 billion in the next future. Its employment base consists of over 28,000 employees in almost 90 countries. Despite Syngenta’s current valuation is negatively affected by short term currency and commodity price volatility, the business prospects are strong. Emerging markets account for over 50% of Syngenta’s sales. The company is listed on the SIX Swiss Exchange (SIX).

Syngenta’s one year stock price performance

Syngenta’s stock price since 2012

Deal drivers

The Board of Directors of Syngenta considers that the proposed transaction respects the interests of the whole stakeholders’ base and so they unanimously recommended the offer to shareholders. The deal will enable strategic continuity and long-term investment in innovation. In fact, it will enable Syngenta to sustain and enlarge its competitive position, while at the same time significantly rising the potential for the seeds business. It will ensure continuing choice for farmers and existing R&D investment across technology platforms. The target’s commitment to cost and capital efficiency will be unaffected by the acquisition. In fact, ChemChina has announced to further enhance Syngenta’s excellent reputation by keeping on investing in its prominent agricultural solutions and innovation capabilities. ChemChina will quicken the implementation of Syngenta’s strategy while boosting Syngenta’s international presence. In fact, the transaction will permit a rapid expansion of its presence in emerging markets and especially in China. Therefore, as recognized by the Chinese corporation, the potential revenues synergies achievable are remarkable, together with an improvement in their cost efficiency measures and the concrete possibility of minimizing operational disruption and execution risk. The above mentioned objectives are reflected in two Syngenta’s commitments already in place which will be perpetuated, that is The Good Growth Plan, which have been explicitly validated by ChemChina, and the Syngenta Foundation for Sustainable Agriculture project. ChemChina is fairly recognizing the potential and high quality of the target’s business. Moreover, Syngenta’s existing management will continue to run the company. More specifically, after the closing of the deal, a ten-member Board of Directors will be chaired by Ren Jianxin, Chairman of ChemChina, and will comprise four of the existing Syngenta’s Board members. “This is absolutely not a China nationalization,” Michel Demaré, chairman of Syngenta, told CNBC.

Structure

On December 9th, 2015 ChemChina announced its first intention to acquire Syngenta for CHF 44bn, that is CHF 449 ($443) per share via a public tender offer on the target’s 100% shares outstanding (i.e. 92,945,649 shares). Syngenta initially rejected the proposal. Twelve days after, ChemChina raised its offer but a group of Syngenta’s shareholders representing 10% of its share capital opposed the deal again. Finally, on February 3rd, 2016 ChemChina announced its renewed proposal for the acquisition of Syngenta’s 98.886% outstanding shares (i.e. 91,909,996 shares) at $465 per ordinary share and a special dividend of CHF 5 to be paid only conditionally on the closing of the transaction. Syngenta’s Board of Directors unanimously endorses ChemChina’s offer. On March 8th, 2016 ChemChina announced it would have executed the transaction via its indirect subsidiary named CNAC Saturn (NL) BV and the Prospectus for the Swiss Public Tender Offer was published soon afterwards. The offer covers the period from March 23rd, 2016 to May 23rd, 2016 with a potential extended period and a cooling-off period going from March 8th, 2016 to March 22nd, 2016. The Public Tender Offer will be open for an initial period of 40 trading days, but it may be renewed for subsequent periods of up to 40 trading days. The purchases will occur either in the open market at prevailing market prices or in private transactions at negotiated prices and it shall comply with related securities laws in Switzerland and in U.S., as it involves not only ordinary shares but also ADR. The transaction is still subject to anti-trust authority approvals and other regulatory approvals in the pertinent countries, but it has already received the Ubernahmekommission approval (the Swiss Takeover Authority), however it is raising legal concerns in the US. It is expected that the transaction will be completed by December 31st, 2016.

ChemChina will make a tender offer for all publicly held registered shares with a nominal value of CHF 0.10 each. Initially, when ChemChina first announced its intention of acquiring Syngenta back in December 2015, the structure of the transaction was remarkably different. More specifically, the Chinese corporation arranged its acquisition plan into two stages: it would have acquired a 70% stake initially for a total of CHF 44bn, that is CHF 449 per share, and then it would have had an option to acquire the remaining 30%. However, the structure was subsequently revised. ChemChina has in the end offered to acquire the company at $465 per ordinary share, payable in cash, together with a special dividend of CHF 5 to be paid only if the deal is successfully closed. ChemChina’s offer sets the value of Syngenta’s total outstanding share capital at over $43bn, which corresponds to a value of CHF 480 per share. The transaction will be financed mainly with borrowed funds. ChemChina agreed to pay Syngenta a breakup fee of $3bn if the offer is dismissed due to the absence of regulatory approvals, especially from the Chinese Authorities or if all conditions set out in the proposals are not fulfilled by June 30th, 2017. In addition to that, ChemChina plans to delist Syngenta in the near future, to then re-IPO the company in few years conditionally on the achievement of its growth and expansion objectives.

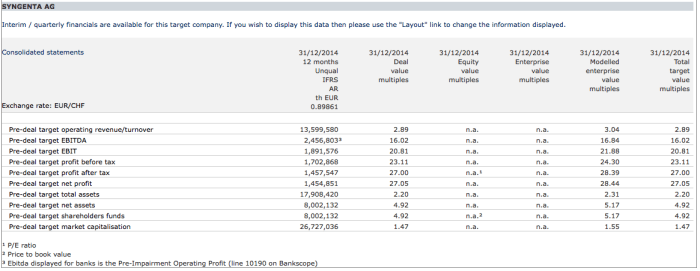

Syngenta’s summary fundamental pre-deal

The public tender offer, as mentioned above, covers exactly 91,909,996 shares, which to be precise represent approximately 98.886% of the target’s share capital. The minimum acceptance level is fixed at 67%. To better clarify the structure of the deal, two scenarios must be recognised. The first one is the following: if ChemChina and/or its subsidiaries ends up holding more than 98% of Syngenta’s voting rights, the cancellation of the remaining shares is envisioned. The second scenario instead foresees that if ChemChina holds, directly or indirectly, between 90% and 98% of the target’s voting rights, it is intended that Syngenta will be merged with a Swiss company, which in turn is directly or indirectly controlled by ChemChina. In this last case, the holders of the remaining Syngenta shares would be compensated in cash, but would not receive any shares in the surviving entity.

The offer price, which is $465 (i.e. CHF 480, EUR 425.62) per share, is considered to be fair according to Syngenta’s shareholders. It, in fact, represents a rumour date bid premium of 44.14 %, based on the closing share price of CHF 333 on June 20th, 2014, which is precisely the last day of trading before Syngenta became a potential takeover target (before Monsanto’s offer). It represents instead an announced date bid premium of 22.36%, based on the closing share price of CHF 392.3 on February 2nd, 2016. The offer price with dividends implies a premium of 31.1%, and the offer price without considering dividends implies a premium of 26.9%, to the volume-weighted 60 trading days’ average price of all on-exchange transactions in Syngenta Shares executed on the SIX before the acquisition announcement.

Syngenta’s share price highlights

| Date | Price | |

| Stock price 3 months prior to rumour | 21/03/2014 | 265.52 EUR |

| Stock price 3 months prior to announcement | 03/11/2015 | 309.10 EUR |

| Stock price prior to rumour | 20/06/2014 | 273.69 EUR |

| Stock price prior to announcement | 02/02/2016 | 353.24 EUR |

The advisors for the transaction are: for Syngenta, J.P. Morgan, Goldman Sachs, Ubs, Baer & Karrer (legal), Davis Polk & Wardwll LLp (legal), N+1 Swiss Capital (for Fairness Opinion); for CNAC SATURN (NL) BV, Credit Suisse (lead manager), HSBC, China International Capital Corporation LTD, CCB International Capital LTD, China CITIC Bank Internationa LTD, Georgeson INC., Homburger AG (legal), Simpson Thacher & Bartlett LLP (legal).

Sources and References: Nasdaq, Bloomberg, Reuters, Zephyr, Financial Times, Companies’ annual reports and websites

To contact the authors:

Giorgia Caruso giorgia.caruso@studbocconi.it

Francesco Maria Fama francesco.fama@studbocconi.it

You must be logged in to post a comment.