Deutsche Bank or the art of tripping over coffee tables

Deutsche Bank AG is a German financial giant, founded in 1870 and headquartered in Frankfurt. It operates with more than 100,000 employees in over 70 countries and has been trying for a long time to become a global investment banking powerhouse of proportions similar to the American bulge brackets. To achieve this goal, it used to leverage on an outsized FICC division, but this strategy has faltered ever since the financial crisis. The faltering investment banking division caused DB to report losses of around EUR 750m in 2017, its third year in a row, with EUR 1.4bn and EUR 6.8bn in 2016 and 2015 respectively.

Deutsche Bank’s net losses mentioned above can be mainly attributed to a long series of fines, whose impositions have put the bank in severe danger of failure. The latest fines it had to pay were:

- February 2018: USD 70m to the U.S. Regulator for ISDAfix’s manipulation, a benchmark for interest rates derivatives and other financial instruments, occurred between 2007 and 2012;

- May 2017: USD 41m to settle Federal Reserve allegation of money laundering;

- January 2017: USD 7.2bn to the U.S government for mis-selling subprime mortgages, packaged into bonds, to U.S. investors in 2005. The U.S. government initially asked for the huge amount of USD 14bn, the second hardest fine in history of financial institutions.

In accordance with the recovery plan aimed to collect cash from the markets, John Cryan, the bank’s CEO since July 2016, has structured two main solutions:

- April 2017: increased capital by EUR 8.0bn through a share offering. The subscription price was set at EUR 11.35 and about 99% were successfully exercised. This capital’s injection increased CET1 ratio to 14.1%;

- February 2018: it has announced its willingness to sell shares of its DWS asset management business. DWS has about EUR 700.0bn under management and is believed to be worth between EUR 6.0 and 8.0bn. It contributes to less than 10 percent of the group’s revenues, but is highly profitable. Hence, with the sale of a 25 percent stake, Deutsche Bank aims to raise around EUR 2.0bn. In addition, Japanese insurer Nippon Life plans to buy a 5% stake in the DWS offering as part of a strategic alliance to give the DWS asset management business increased exposure in Asia.

“While Deutsche Bank is selling part of its crown jewels, the flotation also gives greater flexibility to DWS and could be positive for the unit”, commented Philipp Haessler, an analyst with Equinet Bank AG in Frankfurt.

- For 2017 DWS reported net revenues of EUR 2.5bn (-16.0% y-o-y), EBIT of EUR 720m up from a pre-tax loss of EUR 206m in 2016, net inflows of EUR 15.0bn up flat AuM growth in 2016, as well as management fee margin of 31bps on AuDM and 76bps on active equity positions. Results were impacted by the sale of Abbey Life resulting in EUR 1.0bn goodwill impairment, driven by market concerns about Deutsche Bank.

The Asset Management Industry

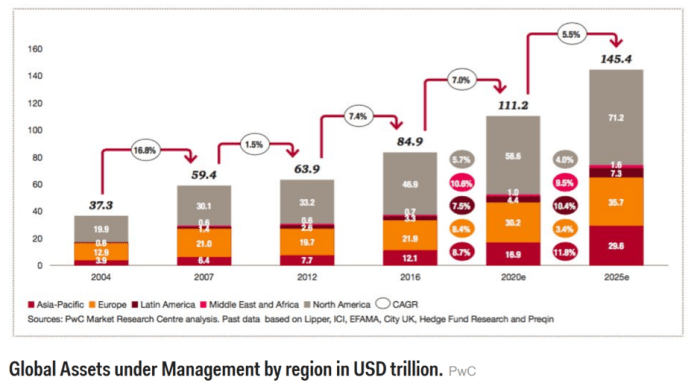

A recent study out of PwC has found that financial institutions, asset managers in particular, are experiencing a slew of changes in the coming years. Consensus, too, predicts that total AuM will increase significantly in the SAAAME area (South America, Africa and Middle East) area. Furthermore, PwC states that this growth can be attributed to three factors: i) increased incentives to take part in individual retirement plans; ii) the heightening number of ultra high net-worth clients in developing economies; and iii) new initiatives by sovereign wealth funds to outsource their discretionary management asset pools. As of 2016, the PwC report estimates the global AuM to amount to around USD 84.9tn in 2016, growing at a CAGR of 6.16% to USD 145.4tn in 2025.

Pairing the positive net inflows projected in the near future, are increased cost. Regulatory complexity and pressure is expected to laden an upward drag on compliance costs, especially in the European Union. The case could be the opposite in the US, pending loosening of existing regulation by FINRA under the Trump administration. In any case, few but vanilla-based asset classes will fall outside the regulatory territory, which may stifle the innovative momentum initiated by the lengthy high-conjuncture of low rates in the past years. Compliance costs and regulatory fees, then, are expected to weigh down the P’n’Ls of managers seeking to diversify their existing asset classes.

Asset and wealth managers have not been dormant, however. Investments into technological, rather than financial, innovation have become a common addition to R&D budgets across the industry. New technologies, such as artificial intelligence, data mining and quantitative strategies have infiltrated the infrastructures of even the most traditional managers, and the industry now calls for a different kind of professional, be it a private banker or account manager.

One development of the asset management industry in particular, has been the popularisation of the Exchange Traded Fund (ETF). ETFs offer a passive solution to otherwise heavily managed investment strategies and are expected to make up 35% of all invested assets by 2020. Their performance is linked to either a stock index or a customised portfolio of diversified equity and debt positions.

Structure and Financials

As previously stated, Deutsche’s goal is to raise cash and realise the asset management industry’s higher valuation multiples. However, as DWS is an integral part of its strategy, it has chosen a very specific structure for the IPO.

The bank’s original plan was to float between 20% and 25% of DWS’ equity by selling a minimum of 20% and potentially adding 2.4% via an upsize option and 2.6% to cover an eventual over-allotment. Given the pricing range of EUR 32-33, this would raise EUR 1.3-1.7 bn for Deutsche and give a valuation of around EUR 6.5 bn. Thus, in any case Deutsche would retain majority control.

However, to further enhance control the bank chose to list DWS as a Komanditgeselschaft auf Aktien (KgaA) or a partnership by limited shares. This specific structure decreases outside investors control and allows DB to effectively make key decisions without having to consult DWS’ board.As Deutsche Bank declared in its IPO prospectus, this could cause a substantial discount for the company’s valuation. Further, this was also noted by large German institutional investors, who were especially wary given DB’s troubled past. Hence, winning the Japanese Nippon Life Insurance as cornerstone investor has been viewed as vital for the deal, especially given the recent surge of volatility in equity markets.

In the end, all went well with Deutsche being able to sell 22.5% of DWS at an issue price of EUR 32.5, raising about EUR 1.4 bn.

| Owner | Ownership |

| Deutsche Bank | 77,75% |

| Nippon Life Insurance Company | 5,00% |

| Free Float | 17.5% |

Although the offering went ahead successfully, questions about the banks ability to pull of its turnaround remained. This culminated in CEO John Cryan’s dismissal and the appointment of DB’s head of retail Christian Sewing to take his post. Will he manage to bring Deutsche back to its glory days or is he another revolving door candidate?

Deutsche Bank is global coordinator on the IPO, while Barclays, Citi, Credit Suisse, BNP Paribas, ING, Morgan Stanley, UBS and UniCredit are bookrunners. Commerzbank, Daiwa, Banca IMI, Nordea and Santander are co-lead managers.

Sources and References: Bloomberg, Business Insider, Companies’ websites, Financial Times, Reuters, Pensions and Investments, Wall Street Journal

To contact the authors:

Davide Martintoni davide.martintoni@studbocconi.it

Edoardo del Vecchio edoardod@usc.edu

Lorenzo Quaglia lorenzo.quaglia@studbocconi.it

Niels Carl niels.carl@studbocconi.it

Niklas Mueller niklas.mueller@studbocconi.it

You must be logged in to post a comment.