On October 31st, French automotive vehicle manufacturer PSA has announced its merger of equals with the Italian-American FCA group in an all-stock transaction. The deal will create world’s 4th largest automotive manufacturer and significant synergies for both groups.

Companies’ Overview

PSA

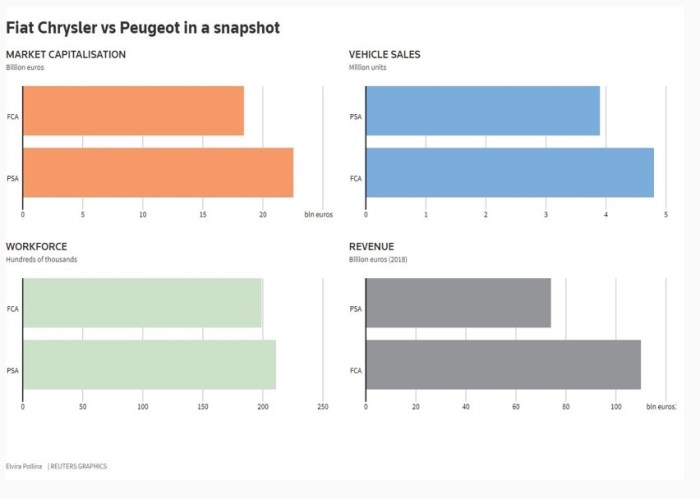

Founded in 1976, PSA Group is a French automotive company that is the result from the merger between Citroën SA and Peugeot SA. It is listed on Paris stock exchange where it is a component of the CAC 40 index. PSA owns five car brands in its portfolio: Peugeot, Citroën, DS, Open, and Vauxhall. The last two were acquired from General Motors in 2017 for a deal value of £1.9bn. PSA also offers a wide array of mobility services under its Free2Move brand, a product line aimed to meet the growing needs of automobile users. With 3.9 million sold vehicles in 2018, PSA is the 9th largest auto manufacturer in the world.

Under the current CEO, Carlos Tavares, PSA has undergone a great strategic overhaul which led to a significant turnaround for the company after the French government bailout in 2012. Mr. Tavares managed to lead the company from net losses to profits in just 3 years and in 2017 company resumed paying dividends after a 6-year break.

FCA

Fiat Chrysler is an Italian-American multinational automobile manufacturer, created after the acquisition of Chrysler by Fiat in 2014. Fiat was founded in Turin in 1899, whereas Chrysler was founded in Detroit in 1925. In 2018, the corporation was ranked 8th world’s largest motor vehicle manufacturer with 4.8 million sales worldwide. FCA owns 9 brands, of which best-selling are Fiat, Ram, Jeep, Chrysler, and Dodge. Fiat Chrysler is headquartered in Amsterdam for tax purposes, while its main R&D and manufacturing centers are located in the Detroit metropolitan area, Turin, and Campo Largo, Brazil. The company is cross-listed on the NYSE and Borsa Italiana, in which it is a component of FTSE MIB.

Until 2018, Fiat was led by Sergio Marchionne, who became the CEO of the struggling company in 2004 and brought it back to profitability in one year. In 2009, he became the CEO of Chrysler, after Fiat agreed to acquire 20% of the U.S. car manufacturer, which in turn allowed Fiat to re-enter the U.S. market. In 2011, Chrysler became profitable again after a 5-year break. With Sergio Marchionne behind the wheel, the company enjoyed years of car sales growth. After Marchionne’s death in July 2018, the company was run by Michael Manley since.

Industry Overview

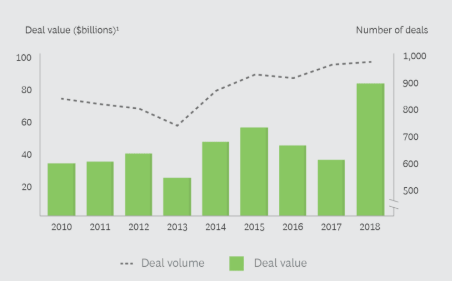

The global automotive market is going through its greatest change ever. Automakers are considering different means of autonomous driving and electric-powered vehicles, forcing them to alter their business models and product portfolios. All this comes at a time where sales have started to decline, and the market is becoming more susceptible to external shocks. The grinding 2019 demand backdrop in key regions will reflect declining volume and compressed margins, forcing automakers to react defensively for the first time since the end of the 2008-09 global financial crisis. In particular, it is expected a decrease in vehicles sold worldwide of about 2% in 2019 with respect to 2018.

Within the automotive industry, Original Equipment Manufacturers (OEMs) and suppliers alike are actively considering a range of joint ventures, partnerships, and alliances in order to stay competitive as the automotive landscape evolves. Industry leaders have recognized that their existing capabilities are not evolving quickly enough to compete effectively with new market entrants from the technology sector. Through strategic alliances, industry incumbents are able to shoulder the upfront costs of new technologies, including the data analytics, artificial intelligence, and advanced telematics necessary for self-driving cars.

Acquisitions continue to remain a key growth strategy for auto OEMs and suppliers. While alliances and partnerships are being considered as a potential alternative to full-scale mergers by major players, both acquisitions and partnerships seem to be driven by the desire to control costs and gain a stronghold in emerging technologies. In fact, although global M&A activity may be stagnant, the auto industry is a global deal-making bright spot. Record mergers, acquisitions, and investment activity attest to the magnitude of the technological and societal changes transforming the business. In a period of unprecedented transformation, auto companies are using deals to jump-start initiatives and gain access to technology, divest assets that no longer make sense for their strategies, and stay a step ahead of activist shareholders. There thus are four main trends fueling the activity:

• automakers and suppliers are using deals as a shortcut to innovation, scale, and growth;

• traditional companies looking to expand into new products and services are competing – and partnering – with investor-backed tech firms looking for deals to scale up their businesses;

• traditional automakers and suppliers are selling or spinning off assets that don’t fit their strategy for the future;

• activist shareholders looking for returns are prodding companies to make changes.

Deal Rationale

The FCA-PSA merger will create the world’s fourth-largest automaker with 8.7m in annual vehicle sales, leaving it behind only Volkswagen, Toyota and the Renault-Nissan group. The companies expect to make €3.7bn of savings without closing plants, and to achieve around 80% of the synergies within the first four years. According to analysts, the synergies amount to €3bn to €6.6bn, equivalent to about 25-55% of combined estimated 2020 earnings.

The combined group will be the biggest in Europe, with a market share of more than 25% of the region’s SUV market and selling twice as many commercial vehicles as the next largest competitor, Renault-Nissan.

FCA, after failing to close the deal with the Renault-Nissan group earlier this year, is trying to get access to the electronic platforms needed to be competitive on the electronic vehicle market, where the group is weak today, and to reduce its current CO2 emissions. As stricter anti-pollution rules are expected to be enforced by 2021, heavy investments into electric and hybrid vehicles are needed to meet the target reduction in vehicle CO2 emissions. According to the strategy firm PA Consulting, FCA faces €700m in emissions fines unless it radically turns down its current emission levels.

By contrast, FCA strong presence in the US market will enable PSA to expand its geographical coverage and reach new markets (North and Latin America) where the group has historically been weak. Moreover, the premium segments of FCA will enable the new group to enlarge its product portfolio and be competitive in all the segments.

Despite the huge synergies in place, the deal is not solving all the issues of the two groups. Being both weak in the Chinese market, a region that has provided fat profits for rivals, the group has still to find a way to increase its market share in Asia. In the first half of 2019, PSA sold 77,000 cars in China, some 11,000 more than FCA, for combined market share of about 1%. By contrast, VW has sold 2 million alone. Thus the newly merged company will still be a long way from conquering the Asian market.

Deal Structure

The transaction is an all-stock 50-50 merger valued at €40bn. To achieve the 50-50 shareholding, FCA will pay out to its shareholders a special dividend of €5.5bn and the company’s stake in its robotics arm Comau (valued at ~€250m), while PSA will offload its shares in parts manufacturer Faurecia (valued at ~€3bn). According to Philippe Houchois, an analyst at Jefferies, this means that PSA is “paying a 32% premium to assume control of FCA”, as after the beforementioned adjustments, FCA equity contribution to the new company will be around €5bn smaller than PSA. The deal has already been approved by the board of PSA and FCA is expected to follow. The new company will establish its headquarters at a neutral location – in Netherlands – while maintaining its listings in New York, Paris, and Milan. Board of Directors will consist of 5 nominees from each PSA and FCA, while Chairman’s position will be retained by PSA’s Carlos Tavares. PSA is advised by Perella Weinberg and Messier Maris & Associés while FCA is advised by Goldman and d’Angelin & Co.

Sources and References: Companies’ reports, Financial Times, Thomson Reuters, CNBC, Bloomberg, Forbes, Autonews.

To contact the authors:

Francesco di Carlo francesco.dicarlo@studbocconi.it

Giovanni Recordare giovanni.recordare@studbocconi.it

Paulius Andzelis paulius.andzelis@studbocconi.it

You must be logged in to post a comment.