Introduction

Euronext pulled off a €4,325 billion offer to the London Stock Exchange for the acquisition of Borsa Italiana group, which will count for an important proportion (34%) of the new group’s total revenues. The offer made with the strong support from Cassa Depositi e Prestiti through CDP Equity and Intesa Sanpaolo beat the competition of Deutsche Boerse and the Swiss SIX. The deal will be financed using a bridge loan and long-term financing. They will be implemented thanks to existing cash, new debt and new equity (private placement to CDP Equity and Intesa Sanpaolo; right offer to the shareholders of Euronext). The transaction, that is expected to be accretive to the adjusted EPS, will create the leading player in European capital markets infrastructure and the largest exchange group in Europe with over 1800 listed companies and more than €4,4 trillion of combined market capitalization. The transaction is expected to be completed in the first half of 2021, even though it is still subjected to the approval of Euronext and LSE shareholders, of regulators in Italy, United Kingdom, United States, Belgium and France, of the German antitrust and European commission.

Borsa Italiana SpA: Company Overview

Borsa Italiana SpA was founded in 1808, following the privatization of the exchange and has been operational since January 1998. Since its foundation, the firm, which is responsible for the organization and management of the Italian stock exchange, has been trying to build an infrastructure which enables the access of international capital. Borsa Italiana’s primary objective, indeed, is to ensure the development of its markets, maximizing the liquidity, transparency and competitiveness while pursuing high level of efficiency.

To achieve its objective, Borsa Italiana has to complete many tasks. In fact, it defines the rules for admission, suspension, exclusion and listing on the market for issuing companies and intermediates. Moreover, it oversees the transaction, check the obligations of issuers and operators, supervise listed companies’ disclosure and provides market data services. Eventually, it developed a fully electronic trading system for real-time execution of trades which enables also brokers who operate from abroad to participate through remote membership.

Borsa Italian merged with London Stock Exchange plc, creating the London Stock exchange group in 2007, which is the leader in Europe for trading of equity, ETF, covered warrant, certificates and fixed income instruments.

Borsa Italiana manages the Italian stock exchange, known as Borsa di Milano. It is the 9th oldest Stock exchange in the world and the 16th in term of capitalization. The total capitalization of the listed companies was €651 billion at the end of 2019, up of 20,1% from 2018. Among the Italian stock exchange Borsa Italiana manages equity markets such as MTA and AIM Italia, fixed income markets such as MOT and ExtraMOT, ETP markets such as ETFplus and Derivatives markets such as IDEM and IDEX. Borsa Italiana recorded revenues for €178,9 million and earnings for €128,4 million in 2018, with a growth of 4,7% and a decline of 4,1% year on year respectively.

Euronext: Company Overview

Euronext is a pan-European exchange group, created in 2000 by the merger between the Amsterdam Stock Exchange, Brussel Stock exchange and Paris Bourse. Since its creation, Euronext has kept growing, making it the largest stock exchange in Europe and one of the largest in the world. In fact, Euronext represents the leading listing and trading venue in Europe with €4,5 trillion combined market capitalization and more than 1500 listed companies at the end of 2019, making it the largest liquidity pool in Europe.

Its growing process began in 2001 and 2002 with the acquisition of London International Financial Futures and Options Exchange and of the Portuguese stock exchange, for €893 million and €134 million respectively and this first part ended with the merger with New York Stock Exchange in 2007, giving the origin to NYSE Euronext.

The NYSE Euronext split up in 2014, with the spin-off of Euronext, which returned to be a standalone European Exchange. In 2014, indeed, Euronext decided to pursue an initial public offering and listed in Amsterdam, Brussel, Paris and Lisbon. Since then, Euronext decided to strengthen its European footprint and diversify its revenue stream by acquiring FastMatch, a global FX spot market operator in 2017 for $153 million. Later, Euronext acquired the Irish stock exchange in 2018 for €137 million and Oslo Børs VPS in 2019 for about $18,19 per share, making a total valuation of $783 million.

Euronext offers plenty of services besides the organization and management of many European stock exchanges. The company operates regulated equity and derivatives markets and is the largest center for debt and funds listing in the world. It represents a single-entry point to multiple listing markets, which include ETF, warrants, certificates and commodities. Eventually, it provides advanced market data services and a range of indices and index solution. Euronext had revenues for €679,1 million and net profit for €222,0 million with a growth of 10,42% and 2,77% year on year respectively.

Industry Overview

Exchanges cover a primary role into the financial industry. There are two main types of exchanges: Organized Security Exchanges and Over the Counter Exchanges (OTC). The first one provides liquidity by employing a market maker that makes sure that buying and selling orders are executed.

An OTC provides access to securities not available on standard exchanges such as bonds, ADRs, and derivatives. Fewer regulations on the OTC allows the entry of many companies who cannot, or choose not to, list on other exchanges.

Usually, stock exchanges offer three different but interrelated services:

- Capital markets: composed of primary and secondary markets. The most common capital markets are the stock market and the bond market. Capital markets seek to improve transactional efficiencies.

- Information services: offers information and data products, such as indexes and benchmarks, real time pricing data, product identification and reporting, as well as network connectivity and server hosting services.

- Post trade: the process that occurs after a trade is completed. Exchanges offer risk management services, clearing and settlement.

In the European region, there are multiple stock exchanges among which five are considered major: London stock exchange (~$4.6tn); Euronext (~$3.8tn); Deutsche Börse (~$1.8tn); Six Swiss Exchange (~$1.5tn) and Nasdaq Nordic (~$1.4tn).

The Euronext – Borsa Italiana deal will create a true backbone for the Capital Market Union in Europe.

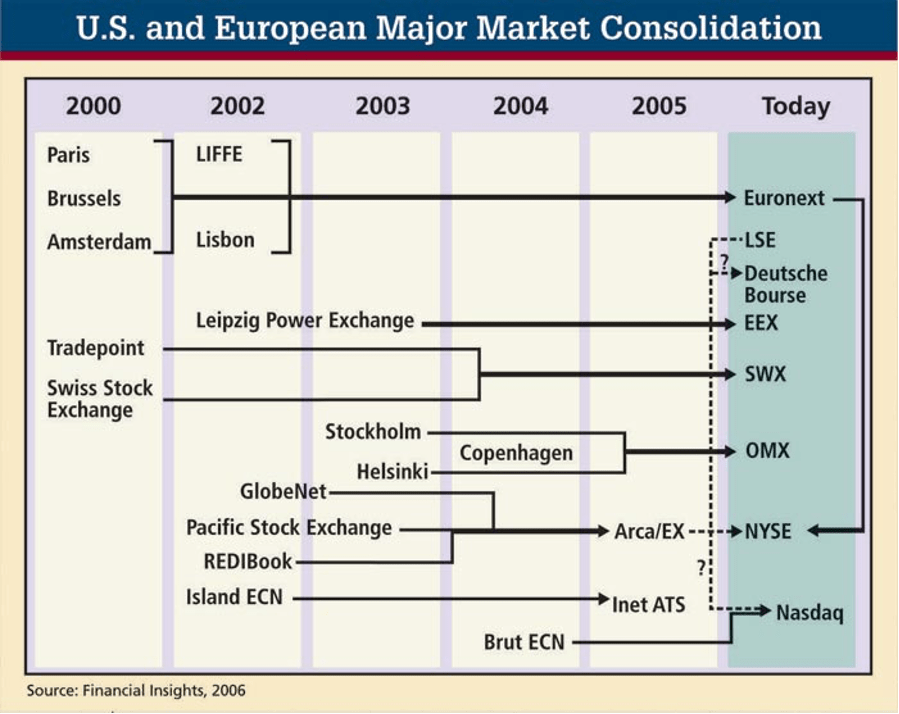

To better understand the picture in which the deal took place, it’s worth analysing the evolution of the European stock exchanges. The first move towards providing a single venue for trading European stocks emerged in the mid-1980s in London (under the name of SEAQ International), with a telephone-based trading system able to attract significant volume and liquidity. The advances in technology were one of the most important drivers of growth and by 1998, every major European stock exchange had gone electronic.

The consolidation trend dates back to the early 2000s when two developments increased the appeal of cross-border trading in Europe. The first one is the adoption of the Euro by a growing number of countries and the subsequent removal of some regulatory restrictions on capital flows which reduced the intra-European currency exposure, making cross-border investment more desirable. The second aspect was the emergence of an equity culture across Europe. In fact, there was a gradual increasing acceptance of equity as a financing tool compared to the more bank-oriented systems of the previous years. In this situation, stock exchanges began to have a greater incentive to expand across national boundaries.

More in general, stock exchanges can grow organically by increasing listings, developing, and marketing new data products, and branching out into other asset classes, such as derivatives. They also can grow inorganically by acquisition of other exchanges, ECNs, clearing venues or technology companies. For instance, Germany’s Deutsche Bourse has grown vertically within its country, owning both clearing and exchange technology firms as well as a derivatives exchange. Euronext, on the other hand, has chosen a more horizontal approach, merging several European markets onto one.

A consolidation of European stock exchanges gives rise to different benefits for the financial sector. The establishment of compatible or shared trading platforms is a source of operational economies of scale and it favours investment banks and brokers that can engage in cross-border transactions at a lower cost. Moreover, trading economies of scale are realized from the attainment of heightened market liquidity and reduced market fragmentation.

Nowadays, a consolidation desire is still alive, also beyond the EU. It’s worth mentioning the Hong Kong exchange $39 billion bid (in 2019) to take over the London Stock Exchange (LSE). This deal would have created a global market infrastructure leader, but was then dropped for different reasons, including the fact that the Hong Kong offer was contingent on the LSE not merging with the UK-based data company Refinitiv.

Eventually, the environment of European stock exchanges will be impacted by Brexit. London is the biggest share trading centre in Europe, handling as much as 30 per cent of the €40bn daily market but, in a no-equivalence scenario, some of that trading will move to cities such as Amsterdam and Paris because EU-based institutions will be barred from trading in London. To this regard, it’s important to bear in mind that a positive final equivalence decision is a unilateral and discretionary act of the EU Commission.

Deal Rationale

Euronext’s 3-year plan objective is to create the largest liquidity pool within the European capital markets union with the acquisition of Borsa Italiana. The acquisition includes numerous financial institutions under Borsa Italiana, such as CC&G, MTS and CSD Monte Titoli. The aggressive expansionary strategy coupled with the occupation of multiple ETFs, including Amsterdam, Brussels, Paris will Entrench Euronext’s position to become the leading financial institution within the European market.

Euronext’s acquisition of Borsa Italiana is a big step to creating the backbone of the Capital Markets Union in Europe and setting a foothold for future expansion within Italy and outwards from it. The Borsa Italiana Group (Borsa Italiana, MTS, CC&G, CSD Monte Titoli and related companies) generated revenue of €464m and an EBITDA of €264m in 2019 at 57% margin and it will comprise 34% of Euronext’s combined revenue. Following the acquisition, Euronext foresees no expected change in dividend policy (50% of reported net income), a strong deleveraging profile (expected to be below 3x Net Debt/EBITDA by the end of 2022) and an expected rating from S&P Global Ratings of “investment grade”. The addition of Monte Titoli to Euronext’s CSD franchise will increase the assets under their custody from €2.2 trillion to €5.6 trillion

The financial impact of the acquisition would boost the Combined Group (Euronext and Borsa Italiana) numbers up to €1.3bn and an EBITDA of €711m for FY2019, with the last twelve months revenue of €1.4bn and EBITDA of €795m as of June 2020. Their portfolio will be significantly diversified with a leading franchise covering fixed income trading, the consolidation of a CSD and a multi-asset clearing house to enable product innovation.

The combination of Borsa Italiana and Euronext will strengthen their listing franchises to facilitate access to equity financing, with a specific focus on SMEs (Small and Medium-sized Enterprises), family-owned and tech companies. This will further the development of ELITE, an international capital raising platform for fast-growing and ambitious companies within Europe. Their presence within Italy and newly-obtained portfolio will make them the leader in listing and trading of equities and cash equities in Europe.

Source: Euronext

Deal Structure

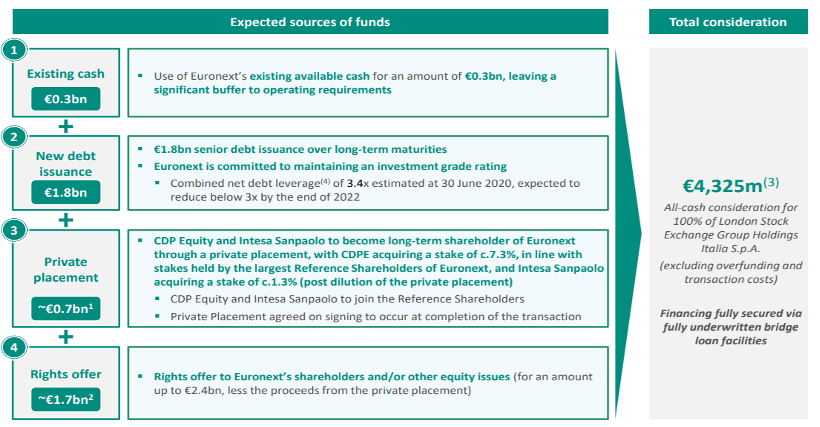

On the 31st July, The London Stock Exchange Group entered an agreement to sell its 100% stake at London Stock Exchange Group Holdings Italia S.p.A., which is the holding company of Borsa Italiana to Euronext N.V. The acquisition holds an equity value of €4.33bn, plus an additional amount reflecting cash generation upon completion. The acquisition of Borsa Italiana also includes multiple companies within the Borsa Italiana group that facilitate revenue generation and data processing within the Italian financial markets, including MTS, CC&G, CSD Monte Titoli.

The cash consideration amounts to €4.33bn with the financing fully secured through a bridge loan facility. The valuation of Borsa Italiana at €4.33bn is represented at 16.7x of its 2019 adjusted EBITDA.

The final financing of the acquisition includes:

- €0.3 bn of use of existing cash

- €1.8 bn of new debt to be issued

- €2.4 bn of new equity to be issued, including a private placement (€0.7 billion) to CDP Equity and Intesa Sanpaolo and a right offer to Euronext’s existing shareholders (including CDP Equity and Intesa Sanpaolo)

Euronext will try to maintain an IG credit rating, a net leverage below 3x by 2022 and no change in dividend policy. The run-rate synergy arising from this acquisition would amount to an additional €60m pre-tax per annum by year 3, through €45m of expected cost synergy and €15m of expected revenue synergy. Euronext expects to incur €100m of restructuring cost to deliver these synergies.

CDP Equity and Intesa Sanpaolo intend to be long-term reference shareholders for Euronext and will enter into an extension agreement before the completion of the contract. Acting jointly, CDP Equity and Intesa Sanpaolo will have the right to propose one third of Euronext’s Supervisory Board seats, which will have a CDP Equity representative. The agreement will include the lock-up of the reference shareholders’ ordinary shares in Euronext in the duration of three years. The Borsa Italiana group will maintain its current relationship, structure and functions within Italy, with its central and financial functions based in Milan and Rome.

The company will approve the transaction on the 20th Nov. The completion of the transaction is expected for the first half of 2021.

Click here to download the official article.

Key Sources and References: Euronext Website, Borsa Italiana Website, Financial Times, UBI Banca Website, Intesa Sanpaolo Website, Other sources as illustrated in the official article.

To contact the authors:

Andrea Zenoniani

Matteo Pavoni

Alberto Tricarico

Christian Filipovic

Francesco De Benedittis

You must be logged in to post a comment.