Introduction:

On February 3rd 2020, Takeaway.com acquired Just Eat PLC for €6.5bn, creating the largest food delivery platform outside of China under the name of Just Eat Takeaway.com NV, with a pro forma €1.2bn in revenues.

Industry Overview:

Ever since Pizza Hut launched its online pizza ordering service back in 1994, the online food delivery business has been growing. Due to the increasing presence of smartphones in the past 5 years, online food delivery has become both an efficient and effective way to eat.

At first, companies such as Just Eat and Takeaway.com thrived on offering a Restaurant-to-Consumer[1] experience. However, as competition intensified, companies such as Uber Eats that started off as Platform-to-Consumer[2] by providing the delivery logistics, have forced Restaurant-to-Consumer platforms to also offer an in-house delivery service.

[1] Restaurant-to-Consumer: Online food platform on which clients order. Restaurants are in charge of dispatching the order to the client (takeaway or delivery). An example of this business model is Domino’s pizza.

[2] Platform-to-Consumer: Online food platform on which clients order. Delivery is outsourced to companies that focus on delivering the order.

Furthermore, this sector is set to continue growing in the coming years. As a matter of fact, COVID-19 has strengthened its growth prospects as the online food delivery sector is estimated to account for 20% of the restaurant market by 2024 (forecast was 14% prior to the global pandemic). According to Statista.com, the revenue of the sector is expected to be worth more than $28bn in 2024 in Europe. This is due to the fact that sector revenues are expected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% from 2020 to 2024.

The users of online food delivery are also anticipated to grow to 274 million[3] in 2024 in Europe. Another interesting figure is the potential growth of the Average Revenue Per User (ARPU) which is expressed as Revenue divided by the number of users. The Platform-to-Consumer ARPU is expected to remain the same in the coming years as both revenue and number of users grow similarly ($96.6 per user). On the other hand, the Restaurant-to-Consumer is predicted to grow from $104.1 to $108.8 per user in between 2020 and 2024.

Companies’ Overview:

· Target: Just Eat PLC, UK (LSE:JE) – €7bn Market Cap:

Since its foundation in 2001 in Denmark, Just Eat has undergone several changes. In 2005, Bo Bendtsen, Just Eat’s co-founder, bought out most of its founders and investors and moved the company to the UK. After successfully receiving funding, Just Eat was able to consolidate its position through multiple partnerships (e.g. Alloresto in France and Restaurant Web in Brazil) and acquisitions (e.g. Urbanbite in the UK and YummyWeb in Canada). On April 3rd 2014, Just Eat carried out its IPO on the London Stock Exchange at £2.60 a share. In the last few years, Just Eat has established itself as one of the market leaders in the online food order and delivery service, yet it has been experiencing a slowdown in growth, partially due to the resignation of Just Eat’s first CEO, David Buttress in 2017 because of family issues.[4]

· Bidder: Takeaway.com N.V. (AMS: TKWY) – €5bn Market Cap:

Takeaway.com is an Anglo-Dutch company specialized in online food ordering and home delivery, its primary purpose is to connect restaurants with customers from the comfort of their homes. The company started to be targeted by venture capital funds in 2012, successfully raising €13M and €74M. In 2016, the company was floated at a valuation of €993M. That same year, the company decided to change its strategy and sell off its UK business to focus in other countries such as Belgium and Germany.

Deal Structure:

In the final structure of the transaction, Takeaway.com acquired Just Eat’s shares with an all-share offer, through which Just Eat’s shareholders own 57.5% and Takeaway.com’s shareholders 42.5% of the combined group share capital. Although the deal was already completed in March 2020, the two companies only started to integrate their operations in late April after approval from the Competition and Markets Authority.

Back in July 2019, Just Eat and Takeaway.com reached a first agreement through a scheme of arrangement. In September, Eminence Capital, a hedge fund, and second-biggest shareholder in Just Eat dismissed the deal due its “highly opportunistic” character. Following this conflict, Naspers, a South African tech conglomerate, decided to seize the opportunity and make a hostile all-cash offer of £4.9bn (£7.1 per share). Just Eat’s board rejected that offer as it “significantly undervalued” the business. This led to a competitive bidding period between Takeaway.com and Naspers which ended with an all-share offer from Takeaway.com, implying a value of £9.16 per share and another one from Naspers for £8.00 per share (all-cash).

Eventually, the target’s shareholders opted for the all-share offer. It consisted of 0.12111 new shares in Takeaway.com for every share in Just Eat, which represented a bid premium of 30.11% based on a closing share price of £7.04 on February 8th 2019, the day before the initial rumour. A bid premium of 14.13% was also paid based on the closing share price of £8.03 on December 18th 2019.

Just Eat PLC was advised by Goldman Sachs, UBS and Oakley Advisory Ltd, while Takeaway.com was advised by Bank of America and Lazard.

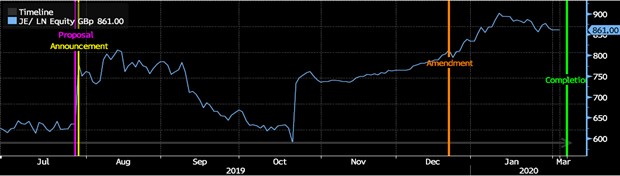

Below is a visual representation[5] of the evolution of Just Eat’s share price at the different stages of the deal. At the end of July 2019, when both parties reached a first agreement, Just Eat’s share price bounced by around 16%. More than 6 months later, Just Eat traded one last time under the ticker JE to close at £861 per share, a 26% increase to pre-acquisition stock price.

Deal Rationale:

In 2018, two of the main competitors of Just Eat, Deliveroo and Uber Eats significantly increased their respective market shares, intensifying the competition in the sector. Accordingly, Peter Plumb, CEO of Just Eat, shifted the company’s strategy which entailed significant investment and that slowed earnings growth in the short-term. This created a climate of tension in between shareholders and the board, which eventually led to Peter Plumb’s resignation in early 2019, 16 months after joining the company.[6]

In order to recover from this period of decline, Cat Rock Capital Management LP, one of the main shareholders, (1.91%) expressed that a merger with a group within the same industry could solve their issues. Following this statement, Just Eat rapidly found a first agreement with Takeaway.com in August 2019. Just Eat’s management and a significant percentage of the shareholders were immediately in favour of this deal because it would address most of the problems of the company: increased competitiveness, an experienced CEO (Jitse Groen – Founder and CEO of Takeaway.com since 2000) and a cultural shift – innovative and entrepreneurial culture.

Firstly, this deal could create the largest food delivery platform outside of China with a pro forma €1.2bn in revenues, combining three of the four major food delivery companies in the UK, Netherlands, and Germany. Secondly, it could assemble a reliable management team with decades of combined experience in the sector and a successful M&A track record.

From a synergy-oriented point of view, they are only expecting to save around €20m annual pre-tax cost since there is a limited amount of overlapping in the countries of operations. However, they have a number of strategies they can exploit across the group to create value:

- Expanding Takeaway Pay, a new service that allows corporations to provide employees with meal benefit plans with the aim to replace company canteens

- Partnership with large restaurant chains

- Competitive pricing: keeping the business as the lowest cost platform

- “One Company, One Brand and One IT Platform’[7] philosophy across the combined group whilst retaining the strengths of Just Eat in its individual markets

Furthermore, given the scale and the financial resources of the combined group, they could invest in strengthening their competitive position and leveraging their investments in technology, marketing, and delivery services.

Key takeaway:

A special feature of this transaction was the bidding war in between Naspers with its all-cash offer and Takeaway.com with its all share-offer. The main distinction between cash and stock transactions is that in the former case, acquiring shareholders should take into consideration the marketability of the shares, the value of the underlying stock and the impact of the transaction itself. Indeed, the shareholders take on the entire risk that the expected synergy value embedded in the acquisition premium will not materialize. In a stock transaction, the synergy risk is shared in proportion to the percentage of the combined company the acquiring and selling shareholders will own.

Usually, an all-cash offer is preferred, especially in highly competitive environments. Nevertheless, Takeaway.com managed to win the deal, partially thanks to Bank of America’s involvement in the transaction. They helped Takeaway.com by presenting their strategy to Just Eat shareholders through several roadshows and conferences. They also backstopped Just Eat’s revolving credit facility for £350m[8] which facilitated the merger.

[3] Statista.com

[4] Nytimes.com

[5] Bloomberg Terminal

[6] Ft.com

[7] Justeattakeaway.com

[8] Bankofamerica.com

To contact the authors:

One thought on “Just Eat – Takeaway.com: All-share or all-cash offer”

Comments are closed.