Introduction:

On the 8th of October 2020 Morgan Stanley announced the acquisition of the investment management firm Eaton Vance for approximately $7 billion. This deal marks the second bout of expansion for the investment bank’s strategic strengthening within Institutional Securities, Wealth Management and Investment Management after it acquired E*Trade in October 2020. Amongst other reasons, Morgan Stanley’s main purpose is to take advantage of more structured fee-based revenue streams.

Companies’ Overview:

Morgan Stanley

Founded in 1935, today Morgan Stanley is one of the most famous global investment banks and an important member of the Fortune 500 list. Morgan Stanley (NYSE: MS, Market Cap: $135.7 billion) generated revenues of $48.2 billion (2020, 16% increase YoY), a pre-tax income of $14.4 billion (2020, 28% increase YoY) and a net income of $11.0 billion (2020, 22% increase YoY).

It is organized into three divisions:

- Institutional Securities – Encompasses all IB and S&T activities for corporate and institutional clients such as corporate lending, capital raising and financial advisory. It generated 54% of their total revenues, delivering $25.95 billion (2020, 27% increase YoY) and a pre-tax income of $9.2 billion (2020, 67% increase YoY).

- Wealth Management – Provides specialized financial services and solutions to individuals and corporate clients including credit, brokerage, investment consulting, asset and liquidity management. This division generated $19.1 billion (2020, 7% increase YoY) and a pre-tax income of $4.4 billion (2020).

- Investment Management – Separated into Asset Management and Investment sub-groups this unit provides asset and investment management services to individual and institutional clients. The division generated revenues of $3.7 billion (2020, unchanged from last year) and a pre-tax income of $870 million (2020, 12% decrease from last year).

Eaton Vance Corp

Eaton Vance Corp, founded in 1924, is one of the oldest investment management firms in the United States. Its business consists of managing investment funds and providing management and advisory services tailored to individuals and institutions globally. Through its subsidiaries and affiliates, Eaton Vance manages active equity and income across a diverse range of asset classes including bank loans, municipal, high-yield and investment grade bonds. It also includes both open and closed-end funds in their management portfolio that they provide to their clients.

Before the 2000s Eaton Vance held management assets worth around $12 billion, but, after a series of restructuring and the acquisition of Atlanta Capital Management and Fox Asset Management, in 2001 this value sprung to $54.6 billion, solidifying the company’s position as an influential investment manager. In 2007, prior to the Financial Crisis, Eaton Vance tripled its assets under management to $158.1 billion. Currently, it oversees over $500 billion in assets making it a key entity within the investment advisory sector.

Eaton Vance (NYSE: EV, Market Cap: $8.2 billion) generated revenues of $1.73 billion (2020, 2.8% increase YoY), a pre-tax income of $334 million (2020, 40% decrease YoY) and a net income of $133 million (2020, 69% decreases YoY).

Industry Overview:

In recent years, the asset management industry has been reshaped by many forces: the longest-running bull market in history, lower fees that bring to shrinking margins and a different composition of portfolios.

The persistence of a bull market has represented an important driver for the steady and relevant growth of the asset management industry since 2008. The total value of global assets under management rose from $38.5 trillion in 2008 to $88.7 trillion in 2019, displaying a compounded annual growth rate of 7.88%. Moreover, it is expected to grow even more in the future according to PwC, which estimates a value of $145.4 trillion by 2025.

As to portfolio composition, the environment of low interest rates and the shift in the clients’ needs also pushed asset managers to look for new more profitable and satisfying instruments. Active core products dramatically declined as people moved towards passive instruments, given their lower fees and no risk of underperforming. Indeed, the former accounted for proximately 60% of total assets under management in 2003 but only for 33% in 2019, whereas the latter recorded a growth of 28% in just 2019. In the future, the active core products market share is expected to further reduce since investors are doubtful about the capacities of managers to add real value given the higher costs.

Finally, alternative and ESG investments are becoming more and more relevant for asset management firms. The total allocation to the alternative side rose from 10% in 2003 to 16% in 2019, but it has become the largest revenue pool and it is expected to account for 49% of global revenues in asset management by 2024. In addition, sustainable investments have experienced an important rise in prominence in asset management, driven by more ESG data, higher investors’ demand and growing regulatory pressure.

Also, as a direct consequence of recently lower fees, the asset management industry has been facing another important trend – consolidation. After a long period of inactivity from 2009 to 2017, the turning point occurred in 2018 when the number of M&A deals in the industry started increasing significantly. Between 2018 and 2019, 253 deals with a combined value of $27.1 billion were announced. The same trend can be deemed true also for 2020, as the investment management-related M&A activity in the US was valued at around $30 billion, with more than 250 operations. Although the industry remains very fragmented with the top 10 asset managers that only account for 35% of market share, this is a clear clue that something is changing, with the market pushing small players to consolidate or specialize in niches.

Reasons behind consolidation:

- These operations are sought after with the aim of obtaining economies of scale and cost – cutting since there has been downward pressure on margins due to a shift to passive funds run by giants like Vanguard and BlackRock, that cut their fee levels in order to increase their flows. There has been a decrease in fees both in active and passive products with an average decline between 2012 and 2017 of 14.3% and a collapse of 19.4% until 2025 is expected.

- Another driver is the willingness of big asset management firms to get bigger and expand their expertise and investment portfolio. Now, many investors are looking for fewer organizations to provide advice and expertise, which enables them to build a complete portfolio.

- PE funds, whose targets are becoming the standalone players, and investment banks are pushing for consolidation. As to PE funds, they consider consolidation a good exit strategy, whereas investment banks want to improve their asset and wealth management division in order to give real stability to the overall organization. They are aiming to make their revenues more dependent on asset management fees, which are more predictable and reliable, rather than trading and investment banking fees which are more volatile.

Banks such as Goldman Sachs, J.P. Morgan and Morgan Stanley have increased their asset management division with acquisitions during this time period. Moreover, even giants in the industry like UBS and State Street are entering in talking for the opportunity to combine the units.

Deal rationale:

Since the 2008 Financial Crisis, Morgan Stanley has been conducting multiple notable acquisitions for various reasons: increasing economies of scale to reduce the pressure from digitalized low-cost investment funds, digitalization of banking capabilities due to the increasing technological benefits and competition during the COVID-19 pandemic, portfolio diversification. More specifically, the deal with Eaton Vance constitutes a further step into the strategic transformation of Morgan Stanley, which has started with the acquisition of full control and integration of retail brokerage joint venture Smith Barney, renamed as Morgan Stanley Wealth Management in 2012. Recently, the acquisition of E*Trade, with a best in class direct-to-consumer digital channel, has contributed to strengthening the scale of the Morgan Stanley Wealth Management Franchise.

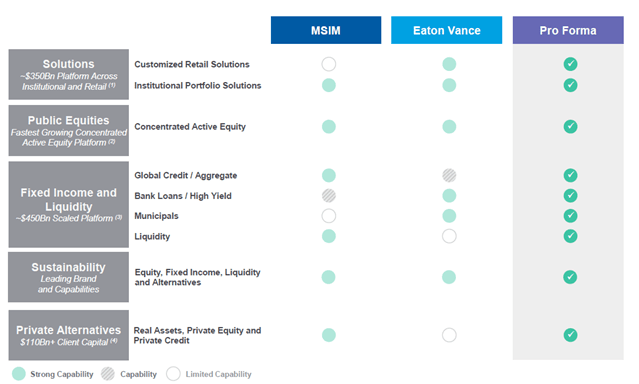

With over $500 billion in assets under management, Eaton Vance would contribute to Morgan Stanley’s Investment Management division with a strong complementary position in key strategic areas, such as responsible investing through Calvert, a pioneering firm in researching and offering ESG investment strategies. Thanks to the acquisition of Eaton Vance, Morgan Stanley will also take control of Parametric, a leading firm providing custom portfolio solutions, whose rise represents another important trend in the industry. Moreover, although much smaller, Eaton Vance’s strong position in high yield bank loans and municipal bonds will expand Morgan Stanley’s fixed income business and bring about an interesting diversification. The other important element is Eaton Vance’s powerful U.S retail distribution (95% of gross sales in the US), which is expected to enrich MSIM’s international distribution.

The deal can also rely on a strong cultural alignment, explained by a solid historical relationship, limited overlap in investment capabilities, well-defined growth opportunities and low execution risk. A transaction, therefore, that is deemed to be very attractive also for shareholders, benefitting from long-term financial returns. It is worth mentioning that this acquisition is also coherent with Morgan Stanley’s strategic direction towards more structured fee-based revenue streams, with a reduced reliance on institutional trading and investment banking revenues. In addition, cost synergies equal to around 4% of MSIM and Eaton Vance expenses are expected.

The acquisition of Eaton Vance creates a leading asset manager with high quality complementary platforms in key secular growth areas.

Source: Morgan Stanley website

Deal structure:

The deal, which is expected to close in the second quarter of 2021, will be financed 50% in cash and 50% in stock. In particular, under the terms of the transaction, Morgan Stanley will compensate the target’s stockholders by paying $28.25 and issuing 0.5833 common shares for each Eaton Vance share. However, as part of an election procedure included in the agreement, Eaton Vance shareholders will be allowed to choose either an all-cash or all-stock consideration. Given that on 8th October – the day of the announcement of the merger – Morgan Stanley’s shares were trading at about $48.50, the total consideration implied ranges around $56.50 per share, with a premium of 38% on Eaton closing price of $40.94 on the same day. In addition, Eaton Vance will pay, out of existing balance sheet resources, a one-time special cash dividend of $4.25 per share before the closing of the deal.

By financing the transaction with 50% cash, Morgan Stanley will use around 100bps of excess capital. However, its CET1 ratio is expected to remain well above the minimum requirement in the long term according to Fitch that expressed positive views on the acquisition upon its announcement. Indeed, in light of Morgan Stanley’s success in past integrations and resilience during the pandemic, the rating agency noted that the incremental integration and execution risks stemming from the deal should not put excessive pressure on the rating outlook of the investment bank which was negative at the time. This statement is further reinforced by considering that Morgan Stanley will likely halt its M&A activity in order to work on the integration of recently acquired E*Trade as well as of Eaton Vance itself, whose transaction is also expected to be marginally accretive.

On the sell-side, Houlihan Lokey Capital Inc and Centerview Partners LLC acted as financial advisors, while Wilmer Cutler Pickering Hale & Dorr LLP, DLA Piper LLP and Simpson Thacher & Bartlett LLP were the legal advisors. On the buy-side, Davis Polk & Wardwell LLP offered legal representation.

References: FactSet, BCG, Bloomberg, CityWire, CNBC, Eaton Vance Corp, Financial Times, Fitch, Morgan Stanley, PwC, Reuters, SeekingAlpha

To contact the authors:

Rebecca Beatrice Revelli

Christian Alan Filipovic

Matteo Pavoni

Alberto Tricarico

Andrea Zenoniani

You must be logged in to post a comment.