Introduction:

Perella Weinberg Partners (“PWP”), a New York-based boutique investment bank focused on M&A, agreed to go public through a merger with a Special Purpose Acquisition Company (SPAC) on Wednesday 30th December 2020.

Backed by banking entrepreneur Betsy Cohen, FinTech Acquisition Corporation IV will acquire Perella Weinberg in a deal that has an implied equity value of about $977 million, representing a strategic bet on SPACs.

Companies’ Overview:

Target: Perella Weinberg Partners

Perella Weinberg Partners is a leading independent global financial services and advisory firm, founded by Joe Perella, Peter Weinberg and Terry Meguid in 2006. The company started its activity with two offices: New York and London. Subsequently, it expanded its business, opening other six offices in the US and two in Europe (Munich and Paris).

PWP has always been centred on providing trusted and independent advice. In particular, it advises corporations, institutions and governments on M&A, financial restructuring, capital structure, private capital advisory and strategic advisory initiatives. PWP has deep expertise in six industry verticals: Consumer, Energy, Financial Services, Healthcare, Industrials and TMT.

Two important recent transactions on which PWP advised are the AT&T acquisition of Time Warner for $108.7 billion in 2018 and the acquisition of a majority stake in Coty’s Professional Beauty and Retail Hair businesses by KKR ($4.3 billion plus $1.0 billion investment in convertible shares) in 2020.

Bidder: FinTech Acquisition Corp. IV

Incorporated in Delaware by the banking entrepreneur Betsy Cohen in 2018, FinTech Acquisition Corp. IV is a blank check company (SPAC) based in Philadelphia, regulated by the SEC. It was created with the objective of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more firms. Thus, the company has no operations and has not generated any revenues.

Through this SPAC, Betsy’s entrepreneurial and experienced vision was focused on identifying disruptive businesses providing innovative technology services to the financial industry with particular emphasis on businesses that provide data processing, storage and transmission services, databases and payment processing services.

Its team has successfully navigated 13 companies in private-to-public transitions with a combined 150+ years of experience in the financial services industry. They have a proven track record of impressive shareholder returns across five combinations to date and a celestial reputation with institutions for quality asset selection.

SPAC’s Overview:

- What is a SPAC?

SPAC, otherwise known as Special Purpose Acquisition Company, is a shell company whose sole purpose is acquiring or merging with a private company (the target) without having it undergo the process of the initial public offering since the SPAC is a registered and publicly traded company. SPACs themselves have no commercial operations with their only assets being the cash raised by its IPO.

- How is a SPAC formed and when does a deal happen?

Typically, a renowned investor (the Sponsor) raises money from a group of investors and pools the funds into one vehicle (forming the SPAC). A prospectus is issued once the SPAC lists on the market.

After the funds raised by the public are set in trust to be used for the acquisition/ or merger, the sponsor usually has up to 2 years to acquire a stake in a private company before it must dissolve and return the funds held in the trust to their investors. In the meantime, the money sits in the bank generating a nominal yield until a deal happens.

The key to attracting funds lies in trusting well-known and successful institutional investors that can convince the public with their expertise to identify and invest in an unknown target.

- What are the advantages of SPACs over IPOs?

Many companies look for a SPAC as a potential sponsor to go public when they cannot or when alternative forms of financing are insufficient or scarce. Despite having similar underwriting fees, SPACs are indeed cheaper due to lower direct expenses and indirect costs.

In addition, since there is much less scrutiny by auditors or regulating bodies such as the SEC, a SPAC transaction may allow the company to go public months before it would do in the context of an IPO. SPACs may also be beneficial in that they provided the listing company with superior price discovery, given that the price is not set by the projections of the bankers, but rather by competing sponsors.

A notable example of a company preferring SPACs over IPOs is WeWork, a commercial real estate company that provides office workspace. WeWork’s filing for an IPO led to its valuation plummeting from $47 billion to the public valuation of $10 billion. Now they are currently in talks to go public via a SPAC.

- Where do SPACs come from and where are they headed?

Present since the 1990s, SPACs have not garnered any attention up until 2003, when a lack of opportunities and compelling returns for public investors prompted a response from entrepreneurs to seek alternative means of obtaining growth capital and equity financing.

As investors seek to streamline the public offering process and leverage a booming stock market, since 2014 there has been a global surge in the involvement of SPACs within the stock exchange with no signs of slowing down: a 4x increase in SPAC IPOs (248 IPOs) with a sixfold increase in capital ($83.3bn) in 2020 compared to 2019 with most of them headquartered in the U.S.

Initially, they primarily targeted the public sector of energy, financial services, consumer goods and various other government contracting markets within high-growth developing economies. Nowadays, their key sectors include technology, biotech, consumer goods and financial services.

Deal Rationale:

Ever since it was founded in 2006, investment banking boutique Perella Weinberg Partners has been speculating on when to go public. In order to raise funds and inaugurate a new phase of growth, the firm has been anticipating its listing by increasing the number of team members, consolidating its international presence and separating asset management to focus on deal-making.

On December 30th, 2020, PWP announced that it entered into a definitive business combination agreement to finally debut on the market via a merger with a SPAC. According to Bloomberg analysts, this move does not only represent a business opportunity for the investment bank looking to grow its existing franchises, but the decision also places “a strategic bet on SPACs as a growing fee segment for Perella Weinberg’s franchise”.

In the absence of such potential synergy, it is possible to recognize one of the reasons why the IPO route was excluded. More importantly, whereas the merger terms imply a target valuation of $977 million, i.e. 15x expected earnings, an IPO would have never been able to raise these big sums and achieve a similar multiple, even in the case of smaller proceeds, due to a way more conservative valuation.

Finally, thanks to net cash proceeds of up to $325 million, the merger with the SPAC will deliver on two other important goals: clearing PWP’s debt ($215 million) and redeeming a portion of ownership ($110 million).

Deal Structure:

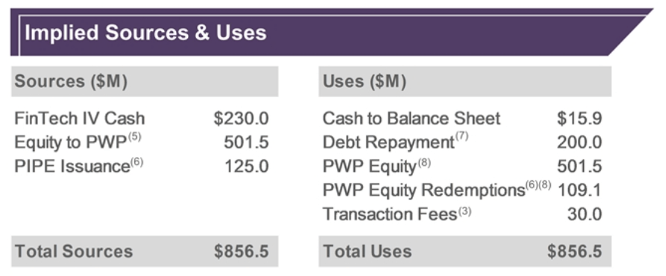

The cash portion of the acquisition, expected to close in the first half 2021, will be financed by FinTech IV’s $230 million cash in trust, $105 of which the SPAC raised in September through an initial public offering (IPO). The other $125 million comes from a fully committed private placement in public equity (PIPE) at $10.00 per share from institutional investors, including Fidelity Management & Research Co. LLC, Wellington Management and Korea Investment & Securities.

The new combined entity will receive net cash proceeds of $325 million from the transaction. $215 million of these will go first towards repayment of PWP’s outstanding indebtedness, while up to $110 million will be used to redeem a portion of ownership interests by non-working PWP equity holders. The remaining part will be used for general purposes. At the end of the deal, PWP expects to have no debt and access to additional liquidity.

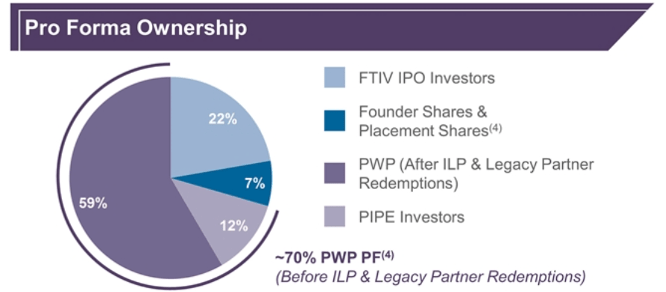

The merged entity will list on Nasdaq under the symbol ‘PWP’. Existing PWP equity holders, including current working partners and employees of the firm, will remain the largest investors by rolling over significant equity into the combined company, with working partners and employees retaining approximately 50% ownership immediately following the transaction.

After the announcement of the $978 million merger, FinTech Acquisition’s shares were trading at $11.59, thus experiencing a 6.9% increase on the previous price. Such a modestly positive reaction to the deal suggests the pricing is reasonable but not bargain basement.

On the sell side, Perella Weinberg Partners LP is serving as exclusive capital markets and financial advisor and Skadden, Arps, Slate, Meagher & Flom LLP are acting as legal counsel. On the buy side, Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC and Financial Technology Partners are serving as financial advisors and Goldman Sachs & Co. LLC and J.P. Morgan Securities LLC are acting as private placement agents.

References: FactSet, Businesswire, Reuters, Bloomberg, SEC, CNBC, Yahoo Finance

To contact the Authors:

You must be logged in to post a comment.