SGFER – BSMAC

Deal Overview

- Potential Target: Toshiba

- Industry: Energy Systems & Consumer Electronics

- Estimated EV: $17.864B

- Toshiba share price: $34.85 (as of 6.4.2021)

Back in April 2021, the international private equity firm CVC Capital Partners announced their offer of 5,000 yen per share, an accumulated $20.8B, for the acquisition of Toshiba. The buyout firm’s proposal included a 31% premium on Toshiba’s share price, which jumped by the daily limit of 18% on the day after the announcement. The Toshiba deal would have been the second deal for CVC in Japan this year after the firm has bought the personal care division of Shiseido Co. in a $1.5 billion deal back in February.

The proposal aimed to speed up decision-making at the company and would have led to the biggest voluntary delisting in Japan’s economic history. Toshiba is now in search of a turnaround opportunity. The bankruptcy of its American nuclear power plant builder, Westinghouse, has led to a prospect of a forced delisting in 2017. Two years of negative net worth and a series of recent accounting scandals have not helped improve the situation. However, the offer by CVC did not seem to be the opportunity they were hoping for. The offer got declined due to a lack of detail and has put question marks over the future of further acquisition proposals. Therefore, this report is intended to provide a deep analysis of Toshiba, its value, and its market environment.

Companies Overview – Toshiba

Headquartered in Tokyo, Toshiba was founded in 1875 under the name of Tanaka Engineering Works, being the first Japanese company that produced telegraph equipment. It eventually changed its name to Toshiba when former Tanaka Engineering merged with Tokyo Shibaura Electric in 1939.

After the second world war, a careful specialization on consumer electronics, made Toshiba grew rapidly and expand on an international level.

During the 1990s Toshiba adopted the “concentration and selection” approach to achieve sustained growth, meaning that they concentrated resources on sectors with high growth potential and selectively promoting the ones already mature. This led to focus resources on semiconductors and expand on the P.C. business.

In addition, to manufacture a variety of consumer and business products, Toshiba also builds HD televisions, laptop computers, DVD players, digital video recorders (DVRs), printers, lighting products, medical imaging equipment, surveillance systems, and liquid crystal display (LCD) devices. It also has an important role in industrial electronics.

In 2015 Toshiba had to face a debilitating accounting scandal, followed by the bankruptcy of its nuclear power division, Westinghouse, in 2017. Those events had an impact on the company’s reputation and sales, leading to sell off multiple divisions (such as the medical devices business, ultrasound X-ray equipment)

Resiliently, Toshiba came back from this difficult moment even stronger, fully focusing on its six divisions

1. Energy systems & solutions: main business areas are power generation systems for nuclear power, thermal power, and renewable energy.

2. Infrastructure systems & solutions: main areas are water supply and wastewater treatment systems, railway transportation systems, and defense electronic systems

3. Building solutions: such as elevators, airport ground lighting systems, air conditioners, heat pump hot water supply system

4. Retail & printing solutions: main areas are POS systems, inkjet heads, and automatic identification systems

5. Electronic devices & storage solutions: such as semiconductors

6. Digital solutions (AI and ICT infrastructure)

Toshiba closed last fiscal year with ¥3.3 billion in sales, counting more than 120.000 employees with more than 50 subsidiaries all over the world. Considering its financial structure, ROE and ROA have followed the same path in the last years, plummeting to a negative level. ROI instead, decreased from 6.6% to 1.8% between 2018 and 2019 but last year it gained back at 8,9% surpassing the earlier peak. Particularly interesting is to look at the net debt/equity ratio: it went from positive 24% to negative 62% between 2018 and 2019. Toshiba is listed in the Tokyo and Nagoya stock exchanges (TOSBF).

State of the Industry – Miscellaneous

To diversify or not to diversify is one of the most challenging strategic questions. After reaching a certain stage of maturity, Toshiba began to diversify its portfolio in order to minimize its market risk. Their diversification led to what we know as one of the largest global conglomerates in the world, their products and services ranging from consumer electronics to infrastructure systems to IT solutions.

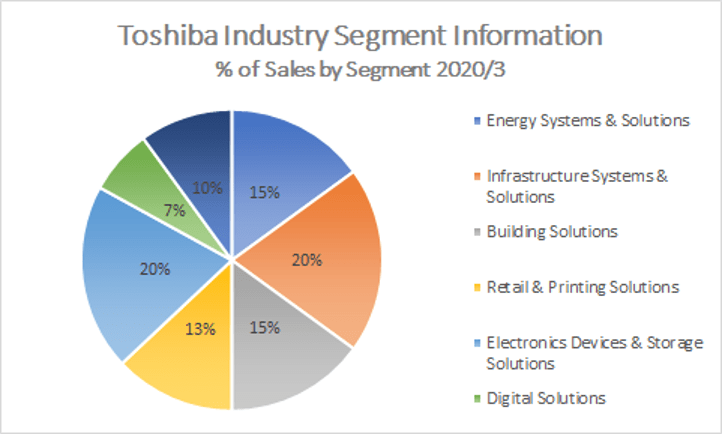

Own Illustration – Source: Toshiba Website, Investor Relations

Toshiba has an extremely diversified and balanced portfolio (according to revenue) with most of its focus revolving around its Infrastructure Systems and Solutions (transport infrastructure, industrial computers & machines, etc.) and the Electronic Devices & Storage Solutions (semiconductor and HDD manufacturing). These industries comprise the cornerstone of Toshiba’s beginnings and expansion. But with such broad products and services offered in the Infrastructure segment most of the relevant events occur in the industry of Electronic Devices & Storage Solutions.

With an ever-growing demand for semiconductors in virtually all industries, Toshiba is struggling to meet the demand and streamline its supply chains. According to a study of Fortune Business Insights over the 2020-2027 period, the global semiconductor market size stood at $513.08 billion in 2019 and is forecasted to reach $762.73 billion by 2027, exhibiting a 4.7% CAGR during the term. Rising consumption of electronic appliances around the globe but also the emergence of AI, IoT, and machine learning technologies are pushing and will push the growth of the industry in the near future.

In light of these circumstances, Toshiba has recently decided to extend its production facilities for silicon nitride substrates in Japan. Toshiba is driven by the concern to cut power consumption in automobiles and industrial equipment. With their recent exit from the LSI (large scale integration) industry in October 2020, Toshiba will be allocating their new funds to the analog IC (integrated circuit, microcontrollers for motor) industry in order to achieve a larger market share and set itself as a major analog IC manufacturer.

Toshiba was known as one of the leading P.C. manufacturers back in the 1990s and early 2000s, however, they officially exited the market in 2020. Toshiba had sold 80.1% of its stake to Sharp in 2018 and selling its remaining 19.9% shares in 2020. Thus, the Electronics devices & solutions segment can now be broken down into semiconductors and hard disk drives (HDDs).

Financial Analysis

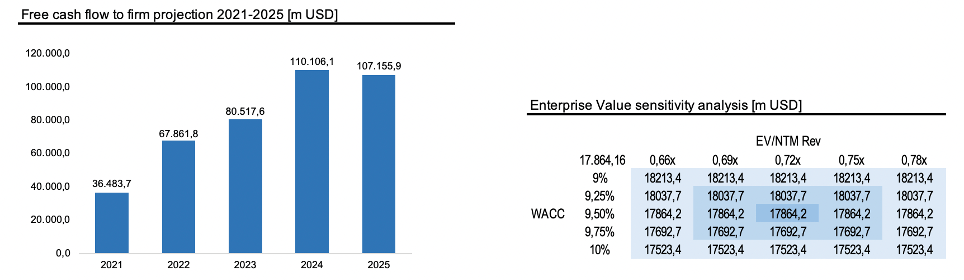

To assess the value of Toshiba we applied both a comparable company analysis and a DCF. Through the former, we obtained an average and a median of EV/Sales respectively of 1.6X and 1.1X for the peer group. Toshiba is roughly in line with it having a ratio of 1.2X. Instead, the average and the median of the EV/EBITDA are respectively 14.6X and 12.1X, while Toshiba is priced relatively higher having an EV/EBITDA of 19.1X.

To get a view that is not affected by the mood of the market, we also deployed a DCF valuation while applying a WACC of 9.50% and an exit multiple (EV/NTM Sales) 0.72x. From a conservative DCF analysis, we retrieved an enterprise value (EV) of about $17.864 billion and an implied share price of ¥4’518.09.

The valuation is in line with the current share price of ¥4’510.00 as of May 19th. However, it must be stressed that there is consensus from analysts of the fact that Toshiba could be worth way more due to its 40% stake in the unlisted Kioxa, or former Toshiba Memory. Analyst estimates of the market capitalization of Kioxa range from roughly ¥1.2 trillion ($11 billion) to ¥2.6 trillion. This implies that Toshiba’s 40% stake may be valued at anything from ¥500 billion to twice as much, with this broad divergence owing to the oscillations in memory chips prices.

Although from an institutional perspective a price of about ¥5000 may be seen as attractive and would imply a fair premium, activists are firmly convinced that the Japanese company is worth more. In the latest Shareholders’ meeting, 3D Investment Partners suggested a valuation of ¥6500, pointing to factors such as the strong intellectual property and admired brand.

Investment Thesis

Toshiba’s diversified portfolio includes a range of technological products and services that are extremely relevant and in-demand to this day. With a strong presence in semiconductor manufacturing and reallocation into the building of analog integrated circuits, Toshiba has acquired a favorable position for the near future considering the shortage of semiconductors in the world market. The recent technological trends and innovations both benefitted and set back Toshiba’s storage solutions sector which primarily concerns the manufacturing of HDDs. HDD manufacturing has seen and will see a steady rise in the demand for cheap, large storage of information. However, their price-performance ($/GB storage) has exhibited a downward shift, and the increasing demand for compact and powerful SSD storage in laptops, tablets, and smartphones presents an uncertain future. Especially, now that SSDs are becoming cheaper and occupy a larger share of consumer electronics than before.

Despite achieving a significant setback in the renewables sector in 2020, the demand for renewable projects will sharply increase by 2021. Pairing this with the increasing demand for infrastructure and renewable energy solutions (wind, solar, hydrogen), Toshiba has bright prospects for the future, especially in developing countries where the need for transport infrastructure and water management is a key component for improving population welfare.

Toshiba’s recent financial performance does not indicate an efficient use of resources available and this may have been a reason for CVC targeting Toshiba. Making it private and restructuring its management and governance to create a profitable investment was a key consideration in their acquisition. Considering that their portfolio is so large, there are bound to be reporting and efficiency issues. Toshiba’s large portfolio presents both an asset and a liability; negative market trends in one sector can shield its losses, but the potential for innovation and technological improvement will not significantly improve its earnings. Toshiba’s continuously dwindling revenues and accounting irregularities present a serious long-term financial issue and unless certain amendments are considered, Toshiba will not enjoy the reputation it once held. At this rate, companies such as Hitachi, Mitsubishi, Sony, and Panasonic will overtake Toshiba and force a complete reorganization of the firm.

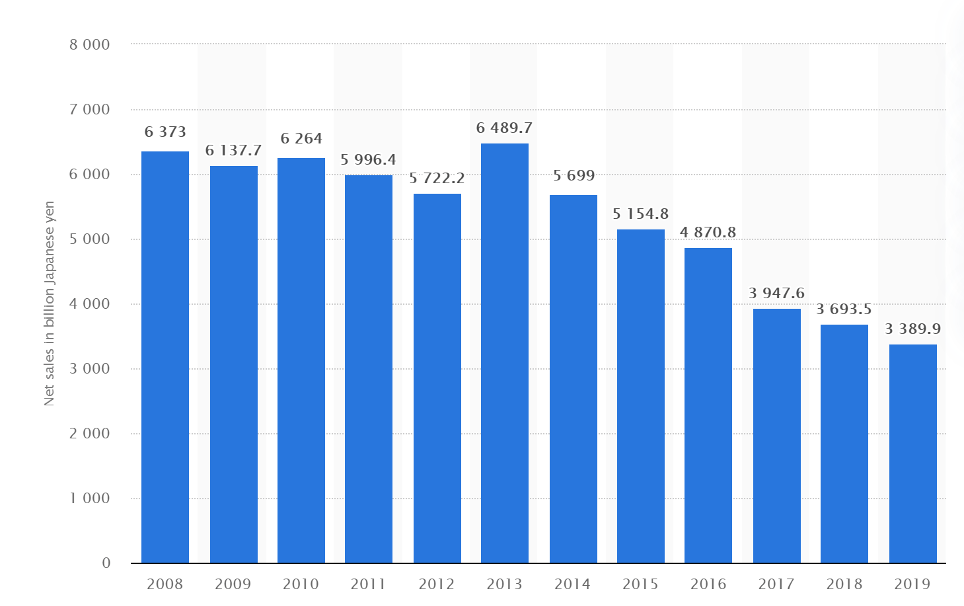

Source: Statista

In the last century and at the beginning of the 2000s, Toshiba was one of the most known Japanese brands. But in recent years it had to face ethical scandals. In 2015 the company admitted having falsified its accounts because they set unattainable goals. After the scandal Toshiba has gone into a profound restructuring, the group even sold some of its important assets in order to focus primarily on its core businesses. Thus, they don’t produce personal computers and TVs anymore, and to offset liabilities Toshiba had to sell the division that oversaw “chip” production.

Despite the restructuring, Toshiba has not fully recovered, never reaching the level it was at before the ethics charges.

The strategy aimed by CVC is to make Toshiba private to drastically change its governance structure. This will lead to faster decision-making, a crucial aspect required in our modern world. Nowadays Toshiba has reached a dimension that makes it too slow and rigid. CVC will carefully analyze each division and for any of them decide to hold or sell, but this time also more from a financial point of view.

The offer from the PE fund came in a difficult moment for the company, in fact, there were frictions between shareholders and the management. This is not the first time that the company has butted heads with activist investors, therefore going private could be a strategic solution.

All in all, there is consensus from analysts that, for CVC or other PE firms, it could be a great deal since the past private equity investments in Japan turned out to be really successful. This is due, apart from the multitude of factors mentioned above, to the availability of cheap funding and the generally high cash flow generated by Japanese companies.

Authors

Christian Alan Filipovic

Pietro di Santo

Silvia Maifrini

Mattia lamonaca

Kilian Veeser

You must be logged in to post a comment.