On September 15th, Adobe announced it would purchase Figma for $20bn, making this acquisition the 8th largest M&A deal in the TMT sector in 2022. Since the announcement, this operation has drawn criticism over the price paid by Adobe and the target’s valuation. Are those concerns legitimate? That’s what we will evaluate in this article!

First, we will review how Adobe has surfed the wave of cloud computing. Then, we will see how Figma has successfully disrupted the tech giant and cannibalized its products. Finally, we will assess whether this acquisition was overpaid and evaluate how this acquisition has transformed the future of Adobe.

Adobe Inc, a software giant that successfully rides the wave of cloud computing

Adobe Inc. (NASDAQ: ADBE), originally known as Adobe Systems Incorporated, is a world-leading computer software company. It is headquartered in San José, California, and was founded by John Warnock and Charles Geschke, who decided to create the company after leaving Xerox PARC in December 1982. Today, Adobe offers a wide range of products and services that professionals, businesses, and consumers use.

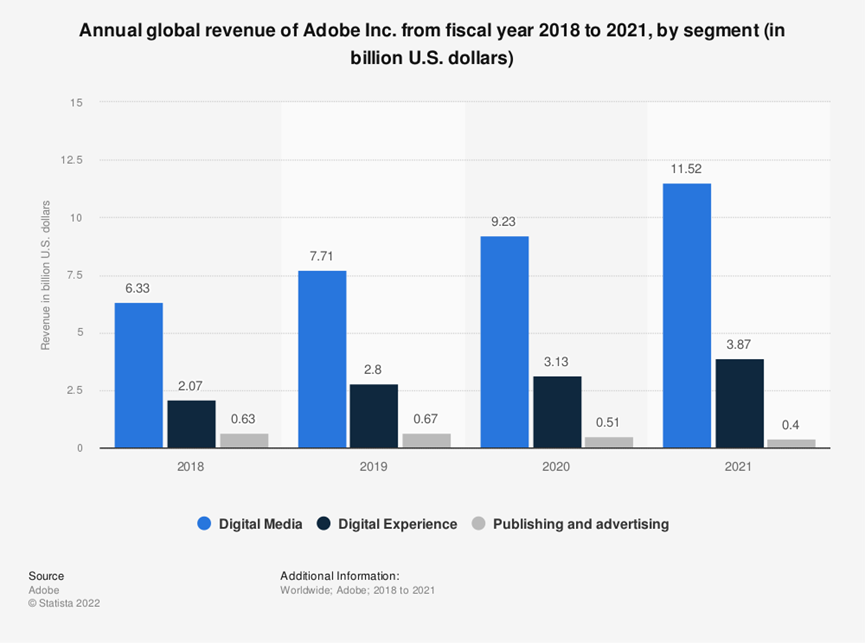

The company operates through three business segments: Digital Media, Digital Experience, and Publishing.

Digital Media accounts for the most considerable fraction of Adobe’s revenues (approximately 73% of FY2021 revenues). Two main segments drive sales: Creative Cloud, consisting of Photoshop, Illustrator, Premier Pro, InDesign, and Document Services, made up of the Acrobat product family (Acrobat, Sign, Scan). It allows individuals and firms to create and promote creative content. In addition, Digital Experience (approximately 24% of 2021 revenues) provides top-notch solutions for marketing, analytics, advertising, and commerce. In contrast, the Publishing segment (around 3% of total revenues) addresses different market opportunities, from traditional document publishing to eLearning solutions and web development.

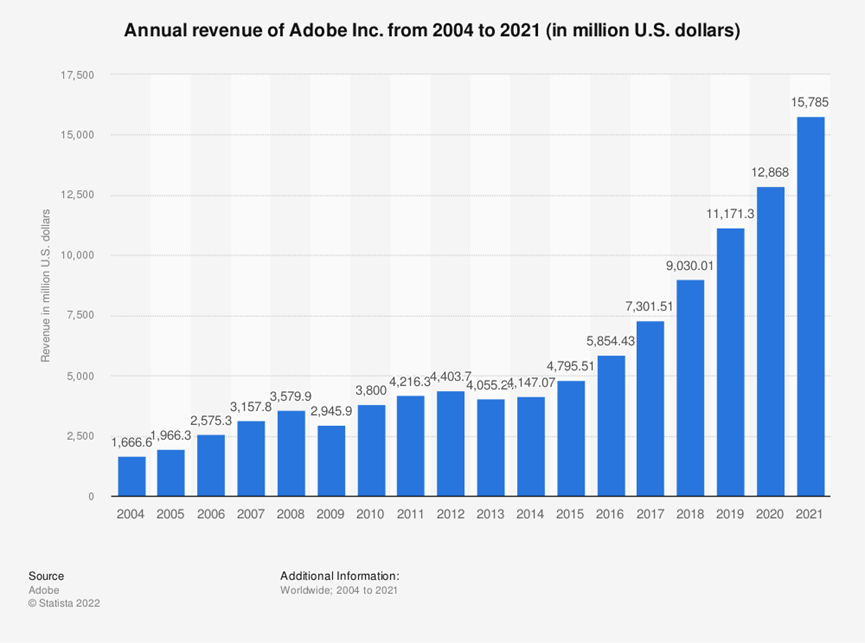

Shantanu Narayen has been Adobe’s chief executive officer, chairman, and president since December 2007. When he took over the company, Adobe sold its users’ Software on disks. However, he was the first to understand the transition towards cloud computing, embracing the change and moving Adobe’s sales online on a subscription basis. In 2007, Adobe generated around $4.2bn in annual sales. Thanks to his guidance, Adobe is now a leading software giant, with total revenues of $15.79bn in FY21 (up 23% year-over-year).

As of November 10th, Adobe has a market capitalization of $151.79bn and employs 25,988 people. The company has recently reported a Q3 net income of $1.14bn and revenues of $4.43bn, up 13% year-over-year. However, the results were below analysts’ expectations, together with its Q4 revenue guidance. As a result, Adobe’s shares have lost 42% for the year, compared with a 35% decline for the S&P 500 software and services group.

Figma Inc., the challenger that disrupted the model

Figma Inc. is a collaborative design web platform based in San Francisco, California. It provides an intuitive interface that allows software developers and designers to collaborate remotely, from preparing slides for presentations to designing user interfaces.

The company idea came from the current CEO, Dylan Field while studying computer science at Brown University, where the co-founder Evan Wallace had studied graphics and was a teaching assistant. Mr. Field dropped out at 19 after accepting a $100,000 grant from Peter Thiel, a libertarian venture capitalist that notably co-founded PayPal and Palantir Technologies. By providing such fellowships, Mr. Thiel wanted to allow the best scientists and entrepreneurs to avoid wasting time on traditional university education.

Ten years ago, when Figma started, it was impossible to believe that sophisticated design could be delivered online in a web browser. Today, the company represents one of the main dangers to Adobe’s business along with other platforms such as Canva. It allows access to intuitive design tools accessible from all over the world.

Figma’s customers count companies as Airbnb, BMW, and Zoom, and about half of its total revenue comes from outside the United States. The deal would be a success for different venture capital investors who backed the project. The investors include Kleiner Perkins, Greylock Partners, Andreessen Horowitz, Index Ventures, and Sequoia Capital, who led a deal in 2019 when the company was valued at $440m.

Figma’s CEO, Dylan Field, believes that the acquisition offers several opportunities to Figma, allowing it to achieve its primary mission: making design accessible to everyone. On Adobe’s side, the deal will enable the company to expand its market share in the growing segment of collaborative-design-workspace). In addition to its existing product Adobe XD which generates $15m of Annual Recurring Revenue (ARR), this deal will provide an additional $400m of ARR for Figma. This transaction demonstrates Adobe’s commitment to focus on the Software as a Service business model (SaaS).

SaaS, a highly competitive and dynamic market

Software as a Service is a way of delivering applications over the Internet as a service. Instead of installing and maintaining Software, users can access it via the Internet. SaaS applications are sometimes called Web-based, on-demand, or hosted Software and run on a SaaS provider’s servers. The provider manages access to the application, including security, availability, and performance. SaaS is one of the three core cloud-based service models alongside platform as a Service and Infrastructure as a Service. Common examples of core business applications with widespread usage delivered via the cloud include Human Resources, Enterprise Resource Planning, and Customer Relationship Management. This model removes the need for organizations to purchase software licenses and eliminates the initial upfront cost involved in implementing and maintaining the complex IT infrastructure needed to deploy Software or applications. The types and number of users of SaaS products have increased rapidly in recent years: it was initially positioned as ideal for startups, but now small and medium enterprises are finding SaaS an affordable solution that empowers agility and digital transformation, and the most important tech companies are starting to use them, as it is demonstrated by the intensive use of Figma by Microsoft in the last years.

In 2020 and 2021, the global SaaS market size was valued at $121.33bn in 2020 and is projected to reach $702.19bn by 2030, growing at a CAGR of 18.82%. The growth in SaaS is attributed to the rapid adoption of cloud-based platforms during the pandemic. SaaS platforms played a vital role in keeping the entire business processes efficiently operating and under control. This was achieved through various features of SaaS platforms such as remote access, digital data exchange, automated reporting, and real-time work floor control.

The projected growth is attributed to an increase in the adoption of SaaS platforms by enterprises to gain strategic and competitive advantages over their competitors. Large companies are increasingly leveraging SaaS software to exploit the possibilities of Big Data. However, the small and medium-scale enterprise segment is expected to grow the most, and this trend will likely continue between 2023 and 2030. Adobe appears to be particularly well-positioned to benefit from the growth of this market. The acquisition of Sigma is expected to pursue this orientation for the company’s future.

Did Adobe overpay Figma?

On September 15th, Adobe announced that the definitive merger agreement had been signed to acquire Figma. The deal amounts to $20bn, which will be paid half in cash and half in stock. The cash consideration is expected to be covered by cash on hand and a term loan, if needed. In addition, about $6 million in restricted stock units will be distributed to Figma’s CEO and employees in the four years after the deal’s closing.

Following the announcement, Adobe’s shares experienced a sharp drop of 17% compared to the previous day. The adverse market reaction might be explained by the concern that Adobe overpaid Figma (50x annualized 2022 forward revenues). This transaction appears slightly anachronistic given the tech crash of the last months; even before the start of the bearish sentiment, its valuation in 2021 would have been roughly $10bn. The highest-valued comparable stocks are currently valued at around 30-35x.

Moreover, Figma is expected to contribute to the group’s profitability starting three years after closing: this implies that, in an optimistic scenario, for at least two years, the acquisition might negatively affect Adobe’s earnings. This, coupled with market analysts’ revised revenue estimates for the acquirer for the fourth quarter, creates the perfect storm. Adobe has a reputation and track record of weathering some disappointment; however, its stock has historically traded at a premium compared to its relatively slim growth profile. This acquisition announcement pushes the decline even further from all-time highs.

The acquisition is still subject to regulatory approval, and the decision to move forward is ultimately in the hands of Figma’s shareholders. Once all conditions are cleared, the closing will take place, ideally in 2023. Dylan Field, CEO, and co-founder of Sigma, will retain his position at the head of the company and will report to David Wadhwani, president of Adobe’s Digital Business.

Purchase or being disrupted, could Adobe make a different choice?

From a strategic standpoint, the acquisition allows Adobe to consolidate its position in the highly profitable cloud-based design market. Nevertheless, some argue that Adobe overpaid Figma because it attached an exorbitant 50x revenue multiple to the transaction in a period when the prevailing revenue multiple for public SaaS companies is 7x. However, this position needs to consider essential nuances and strategic implications that explain why Adobe is willing to pay such a significant premium for Figma. Indeed, the high price tag indicates that Adobe’s top management perceived this operation as necessary for the company’s survival.

The first reason Adobe acquired Figma is to remove the firm from the competition. It allows the company to de-risk one of the two major threats to Adobe’s medium- to long-term profitability: the other existential threat being Canva. Before the acquisition, Adobe was losing to Figma on all fronts. According to the innovator’s dilemma, incumbent companies have all the means to retain their market shares against new entrants, but they are often pushed out of the market by the latter. This is because, while incumbents focus on serving high-value clients, new entrants serve low-value clients but apply incremental improvements that allow them to attack incumbents’ market shares progressively. This is precisely the death spiral Adobe was locked into.

In fact, while Adobe’s Creative Cloud targets professional graphic designers willing to pay premium subscriptions to access apps, Figma adopts a freemium business model which allows anyone to become an app designer. This difference in the business model allowed Figma to outperform Adobe from a commercial point of view to the extent that in 2022 Adobe was forced to slash its revenue forecast for this product line by more than 70% (from $600m to $150m).

However, Figma’s commercial success is not only the result of a better business model but also of a product more suited to the nature of the market. Indeed, the pandemic has shifted designers’ preferences in favor of collaboration-oriented solutions rather than monolithic platforms that hardly allow sharing of projects among multiple parties. In such an environment, Figma’s flexible platform has allowed the startup to cannibalize Adobe’s market shares. Therefore, to prevent Figma from further cannibalizing its market shares, Adobe’s top management decided to engage in a killer acquisition. The decision has allowed Adobe to de-risk one of the biggest threats it faces and will permit Adobe to include new technologies in its product mix.

The second reason why Adobe acquired Figma is that it saw the opportunity to open a new market it could not access previously. Indeed, while most of Adobe’s clients tend to be professional graphic designers, Figma offers a far more intuitive solution that anyone can use. Completing the acquisition gives Adobe access to a larger Total Addressable Market, thus removing one of the constraints that Adobe faced when it came to its top-line growth.

The third reason why Adobe paid a considerable premium for Figma is that it faced a substantial opportunity cost for not acquiring the firm. Indeed, Figma had previously been courted by other potential acquirers (i.e., Microsoft) and was rumored to be moving toward an IPO. To avoid missing the opportunity to acquire its competitor, Adobe wanted to ensure that the transaction went through, so it offered the most it reasonably could. Eventually, the offer was accepted.

Sources: Financial Times, Forbes, The Wall Street Journal, Yahoo Finance, Nasdaq, Reuters, Statista, Adobe, Figma, BCC Research, PR Newswire

Authors: Giulia Duca, Stefano Stompanato, Giulio Pampaloni, Giovanni Candiago

Head of TMT division: Paul Thiriot

You must be logged in to post a comment.