INTRODUCTION

On March 15th, Swisscom concluded binding agreements with Vodafone Group Plc to acquire 100% ownership of Vodafone Italia, marking the culmination of negotiations that began in February, at a price of EUR 8 billion, paid entirely in cash and funded through debt.

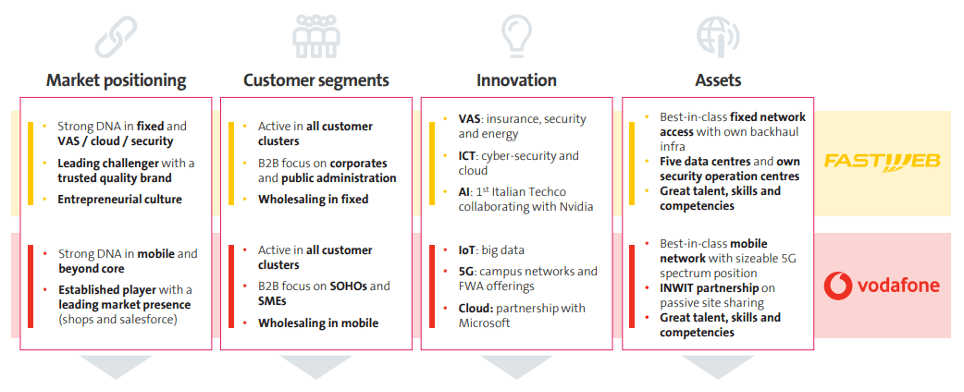

The intention behind this acquisition is to merge Vodafone Italia with Fastweb, Swisscom’s subsidiary in Italy, which it had acquired in 2007, to create one of the most powerful telecom players in the Italian market. The Fastweb expertise in FTTx and 5G infrastructure combined with Vodafone Italia customer base in mobile and broadband services is expected to create a robust entity capable of offering enhanced services to a wider customer base.

Vodafone will return a part of the proceeds from this deal, 4 billion euros, to shareholders through a buyback: investors have responded positively, with the stock showing an increase of approximately 4% on the morning of the day of the announcement.

COMPANIES OVERVIEW

Vodafone Italia S.p.A.

Vodafone Italia S.p.A. is an operating subsidiary of Vodafone Group Private Limited (LSE:VOD). Established in 1995 and formerly known as Vodafone Omnitel B.V., it is currently based in Ivrea, Italy. Vodafone Italia S.p.A. is a mobile operator and provides mobile telecommunication services to customers in Italy. Vodafone Italia S.p.A. offers 4.5G LTE Advanced Pro services in the city of Bologna, Florence, and Palermo; and fixed-wireless access products (Vodafone, 2024).

Source: Vodafone Group plc Annual Report

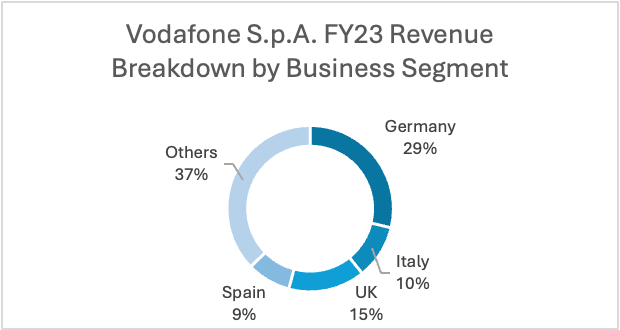

Vodafone Italia S.p.A. is a 100% wholly-owned subsidiary of Vodafone Group Private Limited (LSE:VOD). As of year ending 31 March 2023, Vodafone Italia S.p.A. contributes ~10% of the group’s total revenues (Vodafone, 2024).

Source: Vodafone Group plc Annual Report, Orbis, Capital IQ

Vodafone Italia S.p.A.’s main business segments are Mobile Service (~70%) and Fixed Service (~30%). Mobile Service segment includes voice, data, and messaging plans lasting between 3 to 36 months, tailored to meet the needs of customers in Italy. Fixed Service segment includes connectivity and digital services such as cable TV and video-on-demand services. (Vodafone, 2024)

Financial Analysis

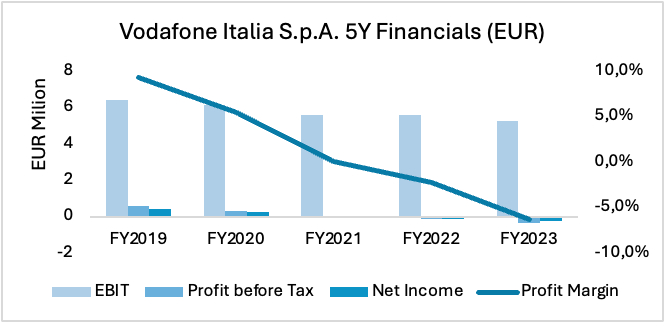

Vodafone Italia S.p.A. has reported a drop in profits and a rise in its cost base such as licence and spectrum costs. The ongoing efforts to break even over the past 5 years has proved to be a challenge for management.

Source: Vodafone Group plc Annual Report, Orbis

From FY2019 to FY2023, Vodafone Italia S.p.A. has seen EBIT decreasing at ~5% Y-o-Y on average. The decline in operating revenue is largely driven by continued price pressure in Mobile Service segment, which has seen increased price competition resulting in a lower active prepaid customer base and ARPU. Net Income has decreased 45% from FY2019 to FY2020 before decreasing steeply from 2021 to 2023. This translates to a decrease in profit margins from FY2019 to FY2023. Similarly, Cash flow has seen steady decreases of 10% Y-o-Y on average from FY2019 to 2023.

Currently with 5,857 employees, Vodafone Italia S.p.A. is planning further restructuring as its parent looks toward another round of cost-saving exercise to reduce costs in the bank. Over the past 5 FYs, Vodafone Italia has seen number of employees decrease by ~0.3% Y-o-Y on average and has announced to cut a further 1,000 jobs in response to its underperformance (Reuters, 2024). Management have attributed the underperformance to rate cuts driven by heightened competitiveness within the telecommunications markets and a lack of industrial vision set by the government.

Swisscom AG

Swisscom AG (SWX: SCMN), established in 1998, is a leading Swiss information and communications technology company with headquarters in Worblaufen, Switzerland. The company provides mobile, internet and digital TV, as well as IT and digital services to both business and private customers. The company provides 81% of the Swiss population with 5G+ and has expanded its optical fibre coverage to 46%, expecting it to grow to 57% by 2025. Through Fastweb S.p.A, the company reaches more than 3,4 million customers in Italy with increasing focus on network infrastructure control and innovation and aims to become a leading AI provider on the market.

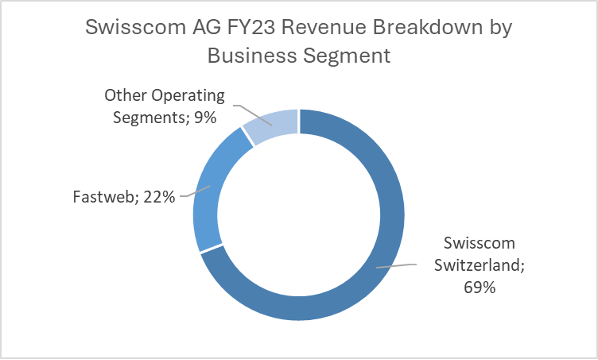

Swisscom AG is 51% owned by the Swiss Confederation and is also present in Italy through Fastweb S.p.A, a telecommunications operator entirely owned by Swisscom Italia Srl, an Italian subsidiary. Fastweb S.p.A’s share of total revenues of Swisscom AG amounted to 22% in 2023.

Swisscom AG’s business is split into Swisscom Switzerland (which includes Residential Customers, Business Customers, Wholesale, and Infrastructure & Support divisions), Fastweb S.p.A, and Other operating segments which supplement the company’s core business activities.

Source: FactSet

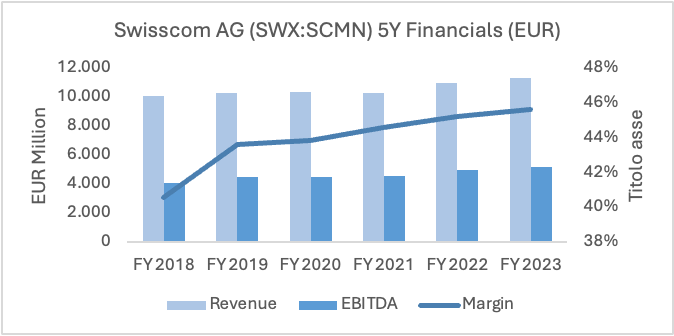

Financial Analysis

Swisscom AG’s EBITDA Margin shows steady growth over the last 5 years, with average increases of 1% Y-o-Y. Although revenues from telecommunication services fell by 2.3% in 2023, mainly due to price erosion, revenue from IT services continued to grow with the demand for cloud, security, IoT and SAP solutions. Fastweb’s revenues also showed significant growth of 6.3% in 2023, influenced primarily by the increase in the subsidiary’s customer base. Swisscom AG’s historical free cash flows show a significant increase in FY 2019 (81% Y-o-Y) and relatively steady figures in the following years. In FY2023, the free cash flow amounted to 1.81 Billion EUR, an 18.6% decrease Y-o-Y, mostly reflected in the changes in working capital (namely a decrease in operating liabilities).

Source: FactSet

INDICATIVE VALUATION BY BSMAC

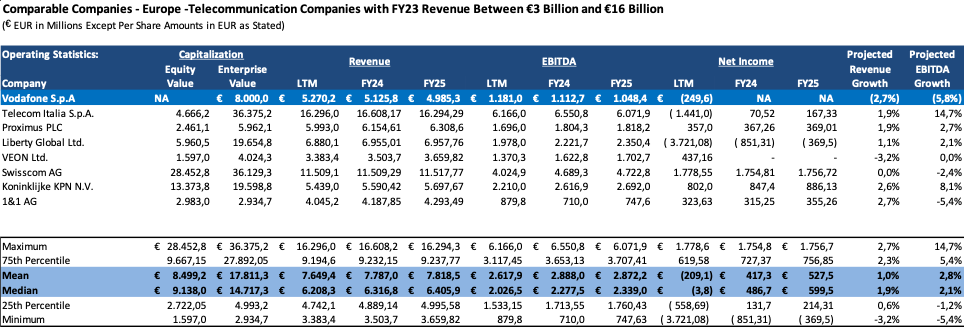

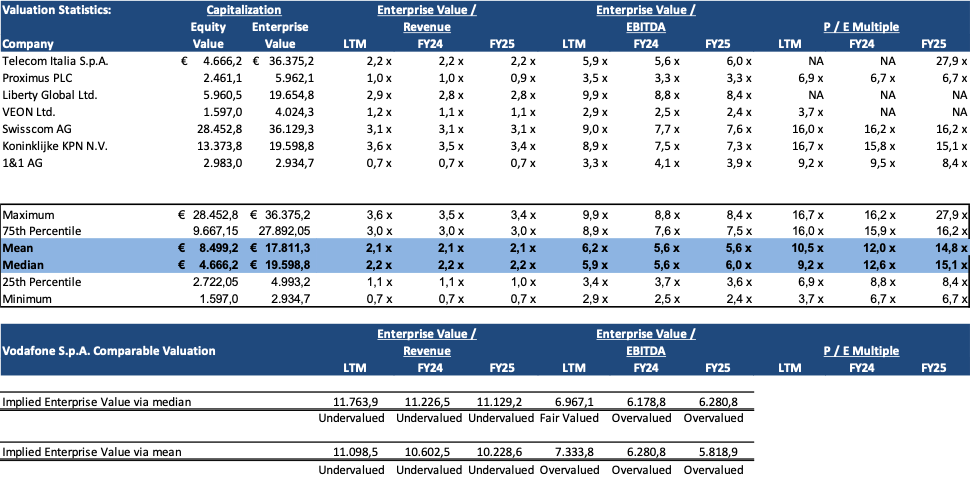

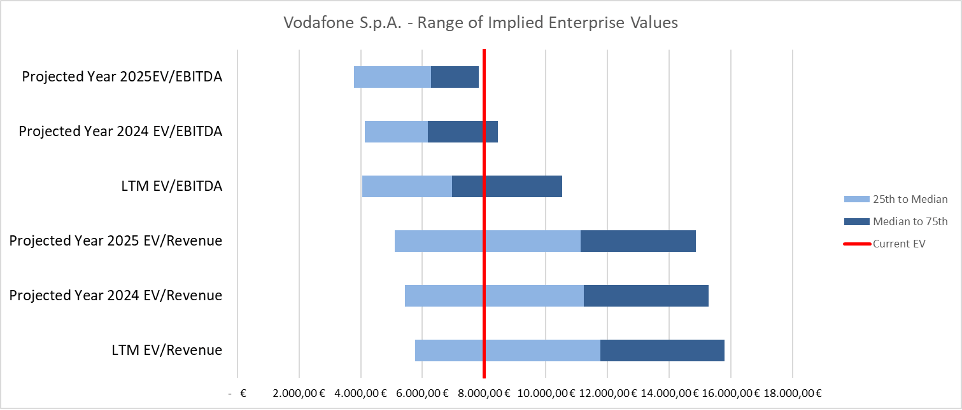

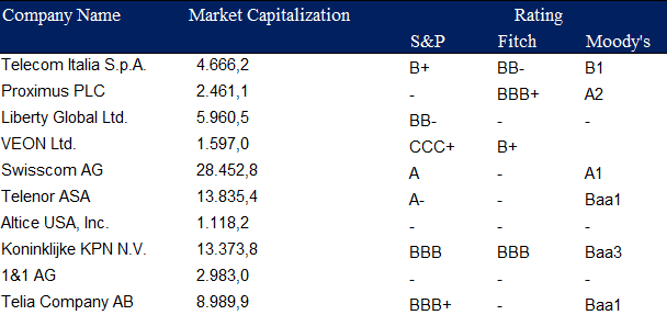

Due to limited publicly available information on Vodafone S.p.A., we conducted a Comparable Companies Analysis (CCA) to determine a range of possible Enterprise Values (EV) for the target, given its current EV of EUR 8 million. It is important to note that the implied valuation from trading comps is not meant to be a precise measure, but rather to set parameters for the target company based on the current market pricing of comparable companies, which might be skewed by irrational market sentiment.

We identified seven companies similar to Vodafone S.p.A. in terms of industry, geography (all operating in Europe), financials (Revenue, Revenue Growth, EBITDA Growth), and risk profiles. Our analysis suggests an implied EV ranging from EUR 7 million to EUR 11 million based on the last 12 months’ figures. Specifically, the current EV appears slightly overvalued compared to the industry’s median EV/EBITDA multiples due to projected declines in Vodafone’s EBITDA for 2024 and 2025. However, it seems undervalued relative to the industry’s mean EV/Revenue multiples. In summary, the EUR 8 million valuation aligns more closely with the mean EV/EBITDA multiples of comparable companies.

Source: Vodafone Group plc Annual Report, Capital IQ, Orbis

MARKET OVERVIEW

In an economic and political context characterized by a rapid and unpredictable landscape, technology, media and entertainment, and telecommunications (TMT) companies are racing to solidify a niche in the extremely competitive TMT marketplace.

The Telecom industry has a risk universe that is arguably more complex and fast-changing than any other sector. Macroeconomic headwinds, ranging from the cost-of-living crisis (49% of consumers say pricing changes are hard to understand) to ongoing supply chain disruption, present a continued threat to financial resilience and stability. New technologies, from generative AI (GenAI) to stand-alone 5G, raise fresh questions around business resilience and service innovation. Meanwhile, enterprise transformation initiatives are expanding in scale and scope. Sustainability is now a major consideration at the board level, while diversity and inclusion (D&I) initiatives and hybrid working models continue to transform ways of working. The industry value chain is also shifting, as infrastructure carve-outs and consolidation reshape telecommunications market structures.

Market Size and Dynamics

Delving into a more precise analysis of the market we start from an analysis of both European and International competitive landscape, focusing on the concentration of the market. From a worldwide perspective, the big players are concentrated in the largest markets (i.e. USA and China) where few firms dominate the market: half of the top 10 global telecom companies, are based in the United States (Comcast, Verizon, AT&T…).

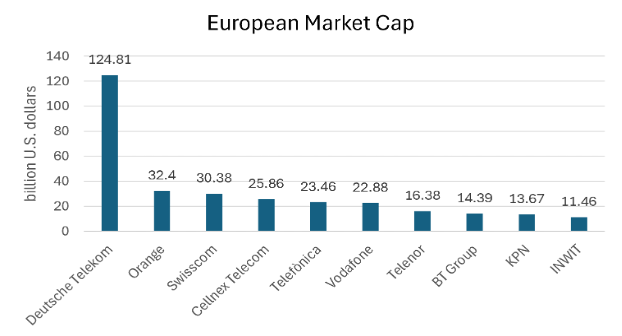

The European telecommunication sector is less concentrated and it is only represented by Deutsche Telekom in the leading 10 telecom companies, which ranks fifth globally with a market cap exceeding 124.8 billion $. Swisscom and Vodafone hold the twentieth and thirtieth positions with respectively 30.38 and 22.88 billion $.

Source: Statista

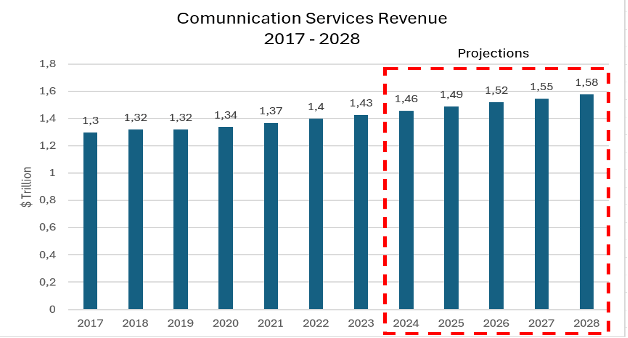

With the rise of new technologies such as GenAI, the expansion of the Telecommunications sector will be driven largely by video traffic, global data consumption over telecom networks will nearly triple, from 3.4 million petabytes (PB) in 2022 to 9.7 million PB in 2027. However, even though companies maintain their long-standing focus on cost cutting, optimisation and automation, providers appear to have little to no pricing power on increasingly commoditised connectivity and data services and consequently, revenues from internet access will rise at only a modest 4% CAGR to $921.6 billion through 2027. Similar conclusions can be derived if we consider all the revenue for the industry. In this case the CAGR is even smaller with a value around 1.71% for the period 2022-207 (see graph below).

Source: Statista

At the same time, telecommunications companies must make heavy investments in the costly infrastructure that enables them to serve customers. The transition to 5G continues and newer technological standards (generative AI) require huge investments. More precisely, telcos are projected to invest $342.1 billion in their networks in 2027 alone just to keep the pace with new technologies.

Impact of M&A Deals

In light of inflationary pressures, constraints on capital expenditure, increased financing costs and competitive market conditions in many geographies, telecom operators are seeking to transform their businesses through M&A. Telecom players will seek to gain economies of scale and synergies through mergers that enable them to pool resources and share the burden of investing in the integrated and scalable 5G networks that customers need.

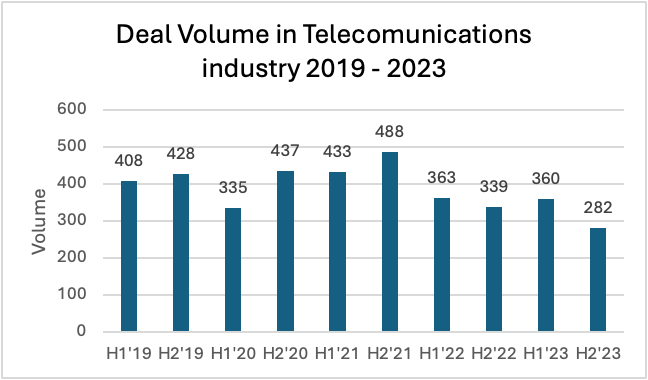

Analysing recent deal values’ trend, we can notice that throughout 2023 deals values remained lower than in the prior two years. The decline in deal activity during the second half of 2023 is attributable to factors such as more restrictive monetary policy, the effects of inflation on consumers, geopolitical conflicts and a changing regulatory environment. Additionally, valuations of companies are often more sensitive to bank rates in TMT than in other industries, which has created a valuation gap between buyers and sellers.

Source: PWC 2024 global TMT outlook

Looking forward in 2024, there are reasons for optimism about dealmaking. According to a PWC’s report, advances in generative AI and other new technologies, more certainty around interest rates, record levels of capital to invest by private equity (PE), and pent-up demand for dealmaking all point towards an increase in the deal activity in 2024. However, the upcoming elections in the US, the UK and other countries may slow the process of authorization for large deals and narrow the window for IPOs. In addition, TMT companies, are focused more on cost reduction and/or avoidance than in recent years, and investors have increasingly prioritised profitability relative to revenue growth in evaluating deals, creating a scenario that may hinder the M&A deals.

DEAL RATIONALE

This strategic acquisition is set to strengthen Swisscom position in the competitive Italian market, where Vodafone Italia and Fastweb are key players in both mobile and broadband services.

The acquisition aligns with the objectives of the CEO Margherita Della Valle (Vodafone) who has been focused on addressing and optimizing Vodafone’s market presence in regions where the return on capital has been less than ideal.

Swisscom objective is to establish a strong presence in the Italian telecom market through synergies based on improved scale, convergence and infrastructure. Becoming the number two in the market with a strong and balanced position across customer segments (26 % mkt share in mobile sector and 31% mkt share in fixed broadband – according to investors presentation on 15 March 2024).

Swisscom is estimating synergies with an approximate figure of 600 million euros annual run rate, which will be achieved after a five-year mark from the merger. We can break down the 600 million euros as follows:

240 million will come from savings in direct costs, mainly obtained by migrating Fastweb’s mobile customers onto the Vodafone network (now Fastweb is a MNVO paying WindTre and Telecom Italia for the network usage, by moving to a proprietary network those costs will be eliminated).

360 million will come from optimization of services provided by Vodafone and economies of scale (in areas such as sales and distribution, consolidation of overlapping functions) and network integration.

Synergies breakdown of Fastweb and Vodafone S.p.A.

Source: Swisscom Investors Relations

The synergy post-merger will not be immediately visible, but will be subject to a ramp-up process, Swisscom expects to reach 70% of synergies in year three and the competition in year 5 during 2029. Integration between businesses will come at a cost, estimated to be 700 million euros, that will be spent during the first three years.

DEAL STRUCTURE

The agreement materialized approximately one month after Vodafone dismissed Iliad’s merger proposal, which would have entailed the creation of a joint venture.

Considering the synergies, the enterprise value of the transaction translates to multiples of 5.1x EBITDA after leases and 9.2x OpFCF. Before their realization, the multiples would be, respectively, 7.8x and 29.4x. This deal is expected to be neutral to Swisscom’s free cash flow (FCF) in the first-year post-closure and to enhance FCF from the second year onward, not accounting for integration costs. Fully debt-financed, the acquisition will increase Swisscom’s leverage to 2.6x (Net Debt/EBITDA) by the close of 2025, from a current value of the ratio of 1.5x.

Nevertheless, Swisscom anticipates that it will maintain an “A” corporate credit rating, one of the most elevated debt ratings in its sector, thanks to a transparent deleveraging trajectory.

Subject to approvals, the closing of the deal is expected to happen in the first quarter of 2025 and is expected to encounter fewer regulatory challenges compared to what would have happened in the potential merger with Iliad.

Authors: Marco Lodrini, Andrea Villa, Bryan Chua, Edoardo Simonetti, Giovanni Fusco, Luka Sulejic

Sources:

Reports on M&A published by both Vodafone and Swisscom on 15/3/24.

https://www.reuters.com/markets/deals/swisscom-buy-vodafone-italia-8-bln-euro-deal-2024-03-15/

https://apnews.com/article/vodafone-swisscom-telecoms-sale-italy-730a64e01f66a88084832d61f8567412

https://www.swisscom.ch/en/about/news/2024/03/15-vodafone-italia.html

https://www.pwc.com/gx/en/industries/tmt/telecom-outlook-perspectives.html

https://www.lexology.com/library/detail.aspx?g=b1877b9d-a036-475e-a573-f1eb0211cd8a

https://competition-policy.ec.europa.eu/sectors/electronic-communications/cases_en

https://think.ing.com/articles/european-telecom-sector-faces-additional-regulation/

https://www.swisscom.ch/en/about/company.html

https://www.swisscom.ch/en/about/investors/reports.html#acc-hJGe3g%5Bselected%5D%5B%5D=0

https://www.swisscom.ch/en/about/news/2024/02/08-results-2023.html

You must be logged in to post a comment.