INTRODUCTION

With a strategic asset acquisition valued at USD 9.9 billion, the largest Oil and Gas company in the UK Harbour Energy significantly expands into multiple regions such as Norway, Germany, Denmark, Argentina, Mexico, Egypt, Libya, and Algeria, by acquiring the upstream properties of Wintershall Dea, a German subsidiary of BASF and Letter One. This is the 6th biggest oil and gas deal globally in the last 6 months and one of the most significant in Europe, where the main objective of companies operating in this industry has been to consolidate their position in strategic extraction and sales areas and secure reserves, extraction, and drilling rights.

INDUSTRY OVERVIEW

At the European level, the Oil and Gas industry is undergoing a very particular two decades, mainly due to continental politics and regulations of production and consumption of substances that are harmful to the environment. Such legislative strategy has led to a progressive shift towards natural gas and renewables: the final consumption of oil and petroleum products declined from almost 400m TOE (tonnes of oil equivalent) in 2000 to less than 330m TOE in 2022, with natural gas helping to cover the gap in countries such as Italy or Germany, while the share of renewables has more than doubled, from an average per EU country of 9.6% in 2004 to 23% in 2022. At the same time at the intercontinental level oil consumption has remained unchanged (USA: ~5.8 billion TOE equivalent both in Y2000 and Y2022) or even increased (China: 2.3b TOE in Y2005 vs 4.8b in Y2022). This embraces the EU’s necessity to switch to less polluting resources, and it is precisely one of the reasons why this deal was born, except for the need to increase reserves and production capacity.

Although the economy is heavily dependent on oil and gas (it’s enough to look at the fluctuations in 2022-2023, where prices reached historically high levels), there has been an interesting evolution in the composition of demand, with a significant switch from Residential, Commercial, and Transportation levels towards the green sector, while industries whose production is centered on materials such as steel, cement, and glass, chemicals and plastics, the so-called petrochemicals and heavy industries, are still practically dependent on and forced to source from the oil and gas sector due to the higher temperatures caused by combustion.

Final consumption of oil and petroleum products in a 32-year range, m TOE

Source: Eurostat, 2024

Forecasts for the near future within the EU suggest an imminent surge in demand for Oil&Gas, as evidenced by the anticipation of approximately 430 investment projects by 2028. These ventures are expected to be spearheaded by industry titans such as Norway’s “Equinor Energy AS” and Italy’s “ENI”. This projected growth can be attributed primarily to the economic recovery and expansion of nations following a period of turbulence. Nevertheless, it is important to acknowledge the overarching EU policy objective to transition away from the consumption of resources that are detrimental to the ecosystem. As part of this trajectory, there is an anticipated decline of ~30% in demand for fossil gas and oil by 2030. Notably, countries like Norway, a frontrunner in the industry, are facing pressure to halt the exploration and development of new oil and gas extraction or export initiatives.

COMPANY OVERVIEWS

Harbour Energy

Harbour Energy dates back precisely one decade. It was founded in 2014 by the private equity firm EIG Global Energy Partners and Noble Group, the commodity trader. Harbour Energy was initially used as an investment vehicle to back Chrysaor Holdings Limited in acquiring oil and gas assets globally. In 2017 Harbour-backed Chrysaor acquired a bundle of oil and gas-producing assets valued at $3.8bn from Shell in the North Sea, averaging approximately 120,000 BOE per day at low operating costs. Subsequently, in 2019, Chrysaor purchased $2.7bn worth of producing assets from ConocoPhillips, adding 72,000 BOE per day to their portfolio. Then, in 2021, Chrysaor merged with Premier Holding in a reverse takeover, and the combined entity became Harbour Energy PLC, the largest independent London-listed oil and gas producer. It remains loyal to its business model of responsibly and sustainably supplying the world’s hydrocarbon demand with operations in the UK, Indonesia, Vietnam, Mexico, and Norway.

Harbour Energy highlights, 2023

Source: Harbour Energy investor presentation, 2023

According to its 2023 Annual Report and Accounts, Harbour Energy produced 186 thousand barrels of oil equivalent per day, down 11% from 2022, at operating costs of $16.4 per barrel equivalent, up nearly 18% from the year prior’s $13.9. One key drawback in their operations is a need for more geographical diversification, with over 90% of production coming from UK assets. However, no hub accounted for more than 20% of production or cash flow, meaning production is spread out through a series of assets. In addition, Harbour Energy is actively combatting this, reporting continuous investments in Mexico and Indonesia, which are adding to their international production. Harbour’s 2023 performance generated $1b of free cash flow and $2.7b of EBITDAX (EBITDA before exploration costs). The company has a very conservative capital stack with a leverage ratio of 0.1x, 50% down from 2022 and 89% down from 2021, demonstrating its commitment to debt repayment in times of heightened commodity prices. In summary, its ability to generate free cash flow and risk-averse capital management enables it to take advantage of M&A opportunities for inorganic growth.

Harbour Energy performance, 2022-2023

Source: Harbour Energy Investor Presentation, 2023

Harbour’s long-term strategy rests on four core pillars: responsibility, quality, diversification, and discipline. These pillars prioritize organic growth while ensuring strict safety and adherence to environmental regulations. They put emphasis on diversification and hedging to uphold robust financial stability across commodity cycles.

Wintershall Dea

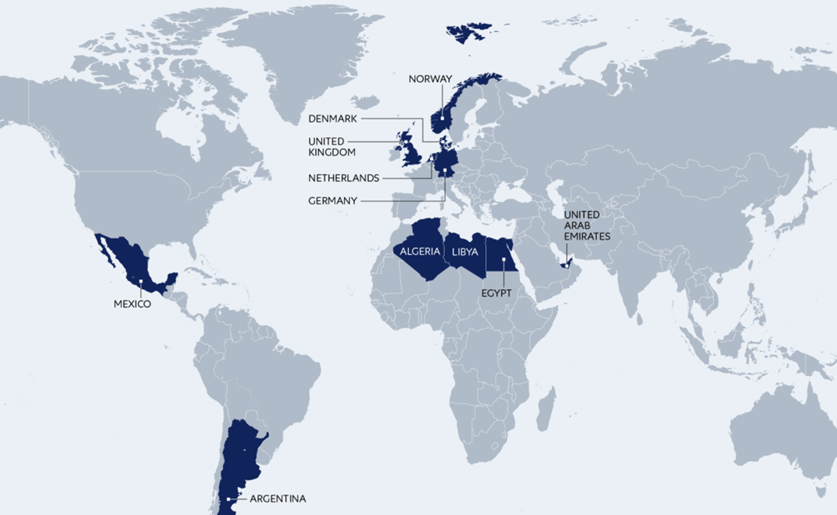

Wintershall Dea is a German independent oil and gas producer formed through the joint venture of Wintershall Holding and Dea DEA Deutsche Erdoel AG. The company’s strategy focuses on the energy transition, providing oil and gas while decarbonizing its value chain and employing carbon management methods. Also, the company draws immense priority to geographical diversification, consistently seeking to enhance its low-cost portfolio of assets present in 11 countries spread around the world. To grow, Wintershall Dea relies on inorganic methods such as M&A activity, investment in exploration, and organic methods, mainly by increasing operational efficiency to drive profits.

Wintershall Dea existing assets (pre-deal)

Source: Wintershall Dea website

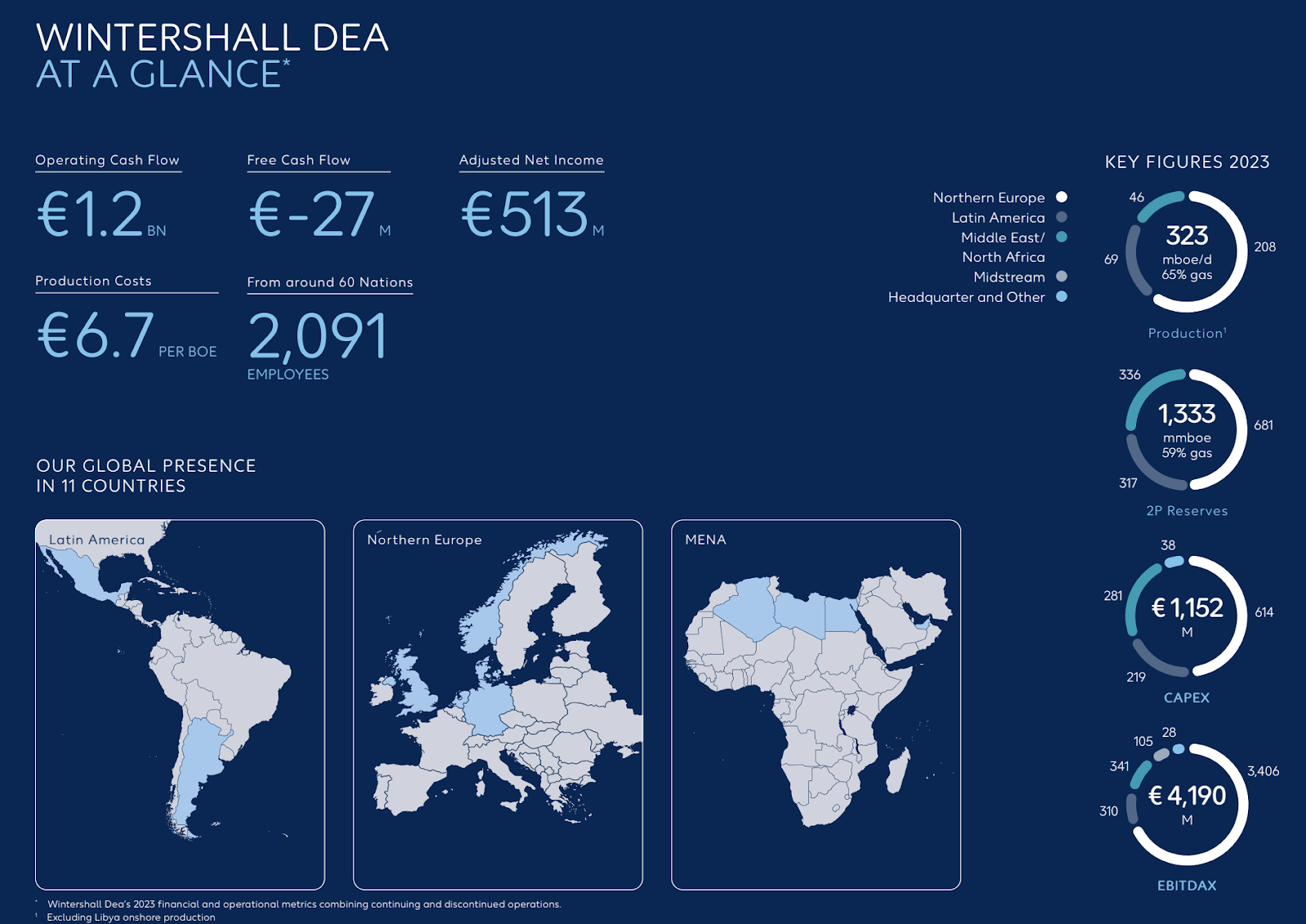

In FY 2023, Wintershall Dea reported solid operational performance but struggled financially with generating cash flow. They saw an increase in their debt capital and, consequently, leverage. Regarding output, Wintershall Dea has not grown since 2022: the production constituted 323 thousand barrels of oil equivalent per day in FY 2023 at a production cost of €6.1 per barrel of oil equivalent, 5.2% up from 2022. In terms of profitability, their 2023 EBITDAX figure saw a 29% plunge from 2022, while net income decreased by 45% to just €513m. Consequently, they didn’t manage to generate free cash flow, reporting -€27m in FY 2023, tripling their operating leverage to 0.6 in a scramble to cover operational costs. In 2024, Wintershall Dea expects their EBITDAX and free cash flow figures to be even lower

Wintershall Dea highlights, 2023

Source: Wintershall Dea Annual Report 2023

Wintershall Dea’s long-term strategy puts focus on M&A and exploration for moderate growth, while simultaneously improving carbon management and developing hydrogen operations to construct a decarbonized portfolio. The company owns upstream assets in Norway, Germany, Denmark, Argentina, Mexico, Egypt, Libya, and Algeria. These assets and their C02 Capture and Storage licenses in Europe comprise the “target portfolio” Harbour Energy seeks to acquire.

DEAL RATIONALE

The deal rationale fits well with both Harbour and BASF outlined strategies.

Harbour Energy

With the bidder being the UK’s largest oil and gas producer, Harbour pursues a strategic vision to evolve into a large, geographically diverse O&G company through disciplined M&A. The acquisition of assets from Wintershall Dea’s exploration and production business (excluding Russia-related activities) will significantly advance Harbour towards this objective. This acquisition focuses specifically on assets, not the entire business, reinforcing Harbour’s approach to targeted growth. The rationale for Harbour’s deal can be broken down into five enhanced dimensions.

Scale and Diversification

Both scale and diversification will increase, accounting for a combined production of over 500 kboepd and 2P reserves of 1.5 bnboe, with activities extending over 8 countries and concentrations in Norway, Argentina, Germany, and Egypt.

Reserve Life, Gas quota, and Margins

Acquired assets are poised to bolster Pro forma Harbour’s reserve life and margins, extending the 2P reserve life from 6 to approximately 8 years.

Post-acquisition, Harbour’s combined 2P reserves and 2C resources will total 3.0 billion barrels of oil equivalent (bnboe). The asset acquisition will also steer the company toward a more gas-centric portfolio, elevating its gas share from 42% to 55% by the end of FY22.

Additionally, the transaction will yield a favorable OPEX of approximately $11/boe, alongside exposure to Brent and TTF markets, enhancing profitability and strategic market positioning.

Sustainability

The deal supports Harbour’s sustainability objective and its 2035 Net Zero commitment. GHG emissions intensity will experience a 25% reduction to around 15 kgCO2e/boe. Sustainability enhancements also come from the European CCS projects(1) capable of storing over 10 mtpa of CO2.

Financials

Harbour will also strengthen its financials thanks to the porting of existing Wintershall Dea Bonds with $4.9 billion nominal value, a 1.8% weighted average coupon, and a weighted average maturity of 4.5 years. As a consequence, the firm’s financing model will become more flexible, unlocking lower costs of financing and Harbour’s access to diverse sources of capital. Harbour is expected to enhance its credit rating to IG(2), also driven by its significant increase in per-share free cash flow.

Shareholder returns

Lastly, the deal supports an enhanced shareholder returns framework, including an annual dividend increase from $200 million to around $455 million, with approximately $380 million allocated to holders of ordinary shares in Harbour. This reflects a 5% increase in dividend per ordinary share to 26.25 cents, supported by a high-quality portfolio, free cash flow accretion, and enhanced financial strength.

BASF

Moving to the seller perspective, BASF’s decision to finalize the deal is primarily driven by its strategic goal to exit the oil and gas business, allowing BASF to reallocate resources and focus on its core chemical and materials businesses. Despite BASF’s clear strategic rationale, the sale has encountered resistance from politicians and government officials in Germany: concerns have been raised about the potential implications of the deal on Germany’s energy security, as the sale could deepen Germany’s energy dependency. Under certain conditions outlined in the Foreign Trade and Payments Ordinance (AWV), the German government has the authority to prohibit takeovers of companies by non-EU entities if deemed necessary for national interests, posing a legislative risk to the deal finalization.

Overview of assets being acquired

Source: Harbour Energy investor presentation, 2023

(1). European CCS – Carbon Capture and Storage – projects involve capturing carbon dioxide (CO2) emissions produced from industrial processes or power generation, transporting them, and securely storing them underground to prevent their release into the atmosphere.

(2). Investment Grade grade signaling corporate bonds have a relatively low risk of default.

DEAL STRUCTURE

Harbour has finalized the acquisition of Wintershall Dea’s Exploration and Production (E&P) business for a total consideration of $11.2 billion. This comprehensive agreement encompasses various elements, including the porting of existing Wintershall Dea bonds valued at approximately $4.9 billion. Additionally, Harbour will issue approximately 921.2 million new shares to Wintershall Dea’s shareholders, amounting to $4.15 billion. To complete the consideration, a cash component of $2.15 billion will be provided, sourced from the cash flow generated by the Target Portfolio between the effective date of June 30, 2023, and the closing date, along with an underwritten bridge facility.

Following the acquisition’s completion, Harbour’s leadership structure will remain unchanged, with R. Blair Thomas continuing as Chairman, and Linda Z. Cook and Alexander Krane retaining their roles as CEO and CFO, respectively. All employees currently part of the Target Portfolio will transition to Harbour, with the inclusion of some personnel from Wintershall Dea’s corporate headquarters.

Ownership distribution in Harbour will reflect BASF’s majority position in Wintershall Dea, where BASF, holding 72.7% of Wintershall Dea, will have a 46.5% stake in Harbour’s listed Ordinary Shares. Meanwhile, LetterOne, with a 27.3% ownership in Wintershall Dea, will acquire 251.5 million non-voting, non-listed convertible ordinary shares in Harbour. Governance arrangements dictate that BASF will be entitled to nominate two Non-Executive Directors to Harbour’s Board, provided it holds at least 25% of the Ordinary Shares.

Furthermore, BASF’s Ordinary Shares and LetterOne’s Non-Voting Shares will be subject to a six-month lock-up period post-completion. LetterOne’s Non-Voting Shares hold conversion potential into Ordinary Shares, contingent on specific conditions being met. Additionally, the dividend payable on each Non-Voting Share will carry a 13% premium compared to any dividend payable on each Ordinary Share.

Notably, the acquisition excludes Wintershall Dea’s assets in Russia and its stake in WIGA Transport Beteiligungs-GmbH & Co. KG. The closing of the transaction is planned for the fourth quarter of 2024, subject to regulatory approvals. Financial insights indicate a pro-forma revenue of $5.1 billion and EBITDAX of $3.7 billion for the combined business in the first half of 2023, and $13.5 billion and $10.3 billion, respectively, for the full year of 2022.

Consideration structure

Source: Harbour Energy investor presentation

Authors: Olga Nasledysheva, Francesco Savelli, Letizia Iannincello, Francesco Casati, Greta Angelova

Sources: Mergermarket, Wintershall Dea, Statista, Eurostat, LSEG

You must be logged in to post a comment.