As the slowdown in global manufacturing driven by high inflation, supply chain disruptions, geopolitical tensions, and weakened demand continues to squeeze margins as many industrial firms are rethinking where they allocate capital. BASF, the Germany-based global chemical company, decided to sell its automative coatings and surface treatment units to Carlyle and the Qatar Investment Authority (QIA) for €7.7 billion reflecting that shift. The deal gives BASF fresh liquidity, while offering the buyers a stable platform in a market that still benefits from consolidation mainly driven by non-cyclical protective demand. This deal captures how large European industrial firms are reshaping their portfolios for a tougher environment.

Carlyle Overview

The Carlyle Group is a US-based global investment firm focused on private equity, global credit, and a custom investment opportunities tool called Carlyle AlpInvest. Since going public in 2012, The Carlyle Group has continuously expanded into real estate, infrastructure, and natural resources. They attract a vast clientele of pension funds, insurance companies, sovereign wealth funds, high net-worth individuals, and families. Their vast portfolio extends to consumer, financial services, aerospace, technology, and healthcare.

Source: BSMAC Research

Since its founding in 1987 and based in Washington DC, The Carlyle Group has become one of the world’s largest investment firms. The group’s most prominent recent deals include a 65-70% stake in Highway and Roop, an auto manufacturing platform in India, of around $400 million; a $1.3 billion strategic investment in insurance broker Trucordia; and a $2 billion investment in Diversified Energy Company to support oil and gas production in the US; all three in 2025 alone.

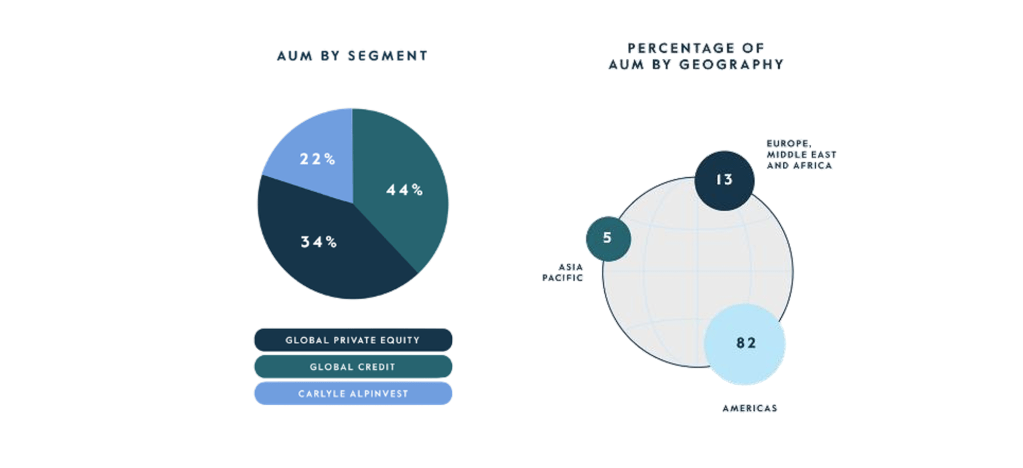

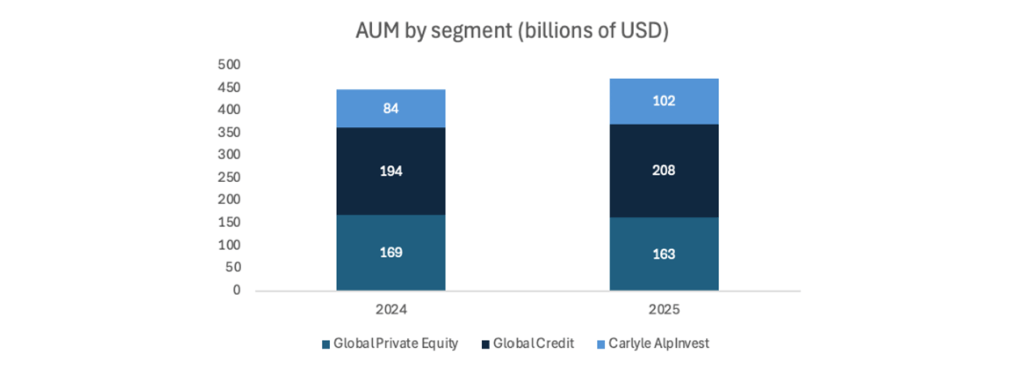

Their $474 billion in AUM, a 6% growth from last year, continues to be dominated by their Global Credit Segment while Global Private Equity trails second (The Carlyle Group, 2025)1. However, Carlyle AlpInvest, which focuses on secondaries and co-investments, continues to be a driver of scale and diversification despite its smaller size compared to the other divisions. It has allowed Carlyle to expand beyond just traditional buyouts and strengthen its competitive position. In 2024, Carlyle recorded fee-related earning of $1.1 billion, up 30% from 2023, with a margin of 46% and a total of $41 billion in revenues that accurately reflects its leading position in the market (The Carlyle Group, 2025).[1]

Source: BSMAC Research

In the industrial sector, The Carlyle Group boasts a diversity of investments. Their portfolio lists 26 industrial-related companies that have been acquired or invested in that have not been exited yet. While most of them involve private companies where no information on the stake or value was disclosed, the following official disclosures have been made by Carlyle:

BASF Company Overview

BASF SE is the largest chemical producer by revenue in the world with chemical sales of approximately $70.6 billion in 2024 (c&en)[2] and a major industrial actor in the global energy transition. The company was established in 1865 and its main office is located in Ludwigshafen, Germany. BASF, which is publicly traded on the Frankfurt Stock Exchange, operates as a Societas Europaea (a public company form under EU law that allows operations under a single legal framework) and is structured around six segments: Chemicals, Materials, Industrial Solutions, Surface Technologies, Nutrition & Care, and Agricultural Solutions.

Source: BASF Annual Report 2024

Since its founding, BASF has evolved from a local dye manufacturer into a global industrial powerhouse. The company expanded throughout the 20th century by developing the first large-scale ammonia synthesis process and integrating petrochemical production into its operations. Today, BASF’s portfolio spans over 50,000 products serving sectors such as automotive, agriculture, consumer goods, and construction, with R&D hubs all over the world advancing sustainable materials.

BASF’s strategic importance extends to the global energy transition and sustainability efforts. As an enabler of low-carbon technologies, BASF provides key materials for renewable energy systems, electric vehicles (such as battery cathode materials) and emissions reduction (through its catalysts business) (BASF Group 2023 at a glance)[3]. Crucially, BASF’s unique Verbund model of integrated production creates significant efficiency advantages: by-products of one process become feedstock for another, and energy is cascaded and reused across the network. This approach not only drives cost efficiency and high asset productivity but also lowers environmental impact. For instance, BASF’s combined heat-and-power systems and waste-heat integration at Verbund sites avoided an estimated 6.1 million metric tons of CO₂ emissions in 2024. (BASF Verbund)[4]

Europe is the group’s largest market, followed by North America and APAC. The group reported revenue of €65.3 billion (−5.3% YoY) in 2024 and an EBITDA before special items of €7.9 billion (margin 12%), as volume increases were largely offset by lower prices and weaker demand. Based on Mergermarket and FactSet (Nov 2025) data, BASF’s EV/EBITDA is close to 10.18x and its P/E (LTM) around 142x, indicating temporarily weak earnings as the denominator contracted while the share price remained relatively stable. Compared with peers such as Dow Inc. and Covestro, which typically trade at single-digit EV/EBITDA and lower P/E multiples, BASF appears more exposed to short-term profit compression and restructuring effects. The equity ratio was 45.9%, with moderate leverage and liquidity supported by €2.9 billion in cash. In the industrial chemicals sector, where margins are cyclical and capital intensity is high, these indicators help assess resilience, valuation risk and how quickly a company can recover profitability through the cycle.

BASF is undergoing a portfolio transformation to align with low-carbon and circular economy objectives. Under the “Winning Ways” strategy, the company is expanding its battery materials and recycling businesses, commissioning a new hexamethylenediamine plant in France and preparing a potential IPO of its Agricultural Solutions division by 2027. These initiatives reflect BASF’s shift toward sustainable and value-added segments while reducing exposure to cyclical petrochemical markets, a move driven by the need to stabilize earnings and align with demand trends. Recent divestitures, including the exit from Wintershall Dea, demonstrate a disciplined reallocation of capital toward growth fuelled by product development. Dr. Markus Kamieth (Chairman of the Board of Executive Directors, CEO of BASF SE) and Anup Kothari (Board Member responsible for BASF Coatings) view BASF as a resilient market leader whose integrated structure and global reach position it strongly for long-term competitiveness, making it a relevant strategic partner in the planned BASF x Carlyle transaction (BASF, 2024)[5].

Note: While expressed by executives directly involved in the transaction rather than independent analysts, their statements are authoritative reflections of BASF’s strategic positioning in this deal.

Market Overview

Over the past two decades, the global chemicals industry has undergone a significant structural transformation driven by shifts in energy economics, regional feedstock availability and evolving regulatory frameworks. In North America, the rise of shale gas fundamentally altered cost structures. Advances in horizontal drilling and hydraulic fracturing in the early 2000s made it economically viable to tap large shale formations such as the Marcellus, Permian, and Eagle Ford, unlocking substantial volumes of natural gas and associated natural-gas liquids (NGLs). This increase in supply reduced ethane prices, a key petrochemical feedstock, giving North American producers a durable cost advantage and stimulating investment in new ethylene crackers and downstream polymer capacity. The abundance of shale gas has helped the US chemical industry become one of the lowest-cost producers globally (Guertzgen, 2015).[6] Middle Eastern producers also benefited from access to low-priced, often state-subsidised natural gas and naphtha, which enabled companies such as SABIC, Borouge and QAPCO to develop large, export-oriented operations supported by favourable policy environments (“Rising forces: Future of the GCC chemical industry,” 2025).[7]

European chemical producers, long dependent on imported oil and natural gas, now face structural disadvantages. Since the 2022 energy-price shock driven partly by supply disruptions following the war in Ukraine and the reduced reliability of Russian gas flows energy costs in Europe have risen sharply, undermining the competitiveness of energy-intensive industries. As of 2024, the European Union still imports a sizeable share of its gas from Russia, though the EU has announced plans to reduce or phase out Russian fossil-fuel imports. At the same time, producers must comply with increasingly stringent environmental and chemical-safety regulations. Under the EU Chemicals Strategy for Sustainability, part of the broader European Green Deal, the EU is tightening restrictions on hazardous substances, phasing out high-risk chemicals, strengthening risk-assessment requirements (including “cocktail-effect” evaluation) and expanding controls on substances of very high concern (Beaumont & Bailey, 2025).[8] Together with more ambitious emissions rules and carbon-cost mechanisms, such regulatory pressure raises compliance and production costs for firms operating in Europe. Weak demand in downstream sectors, particularly construction and automotive manufacturing, has further reduced margins and utilisation rates, exacerbating competitive pressures.

Industry analysts project that growth in the global chemicals sector will moderate compared with the growth rates observed in previous decades (McKinsey & Company, 2024).[9] In response, many firms are shifting their business models away from feedstock-driven expansion toward innovation-led strategies, focusing on technological differentiation, product specialisation and positioning in high-value market segments. Technological differentiation may involve process intensification, advanced catalysis, or other production improvements; product specialisation means moving into engineered materials, specialty chemicals, or high-purity intermediates; high-value segments include applications with strong structural demand such as renewable energy, electronics, pharmaceuticals, and advanced manufacturing.

Within this context, the paints and coatings sector has demonstrated notable resilience. Its stability derives from steady maintenance and repaint demand across construction and industrial assets, pricing power supported by consolidation among leading firms, and a shift toward higher-value, sustainable technologies such as waterborne, powder and low-VOC formulations (“BASF to sell coatings business to Carlyle in EUR 7.7 billion deal,” 2025).[10] Major firms such as Sherwin-Williams, PPG Industries, AkzoNobel and Nippon Paint have used mergers and acquisitions to strengthen market positions, broaden their product portfolios and reduce exposure to volatile feedstock and energy costs (“BASF’s €7.7B divestment signals accelerating industry carve-outs,” 2025).[11]

Recent market data show substantial scale and growth potential in this segment. The global paints and coatings market was valued in the early 2020s at several hundreds of billions of US dollars. In light of stable demand drivers, many industry projections anticipate modest but steady growth over the medium term though the exact figures vary depending on region, end-market dynamics, and regulatory conditions. These baseline conditions stable demand, scale advantages, consolidation, and a shift toward higher-value, sustainable products support a cautiously optimistic outlook for coatings companies over the next decade.

Finally, regional asymmetries in cost structures, regulation and end-market demand continue to drive a divergence in competitiveness across geographies. North America and parts of the Middle East remain advantaged by low-cost feedstocks and supportive industrial policies, while European producers face structural headwinds due to higher energy and compliance costs and comparatively weaker demand recovery. This divergence highlights the challenges that European firms must overcome to maintain global competitiveness.

Deal Rationale

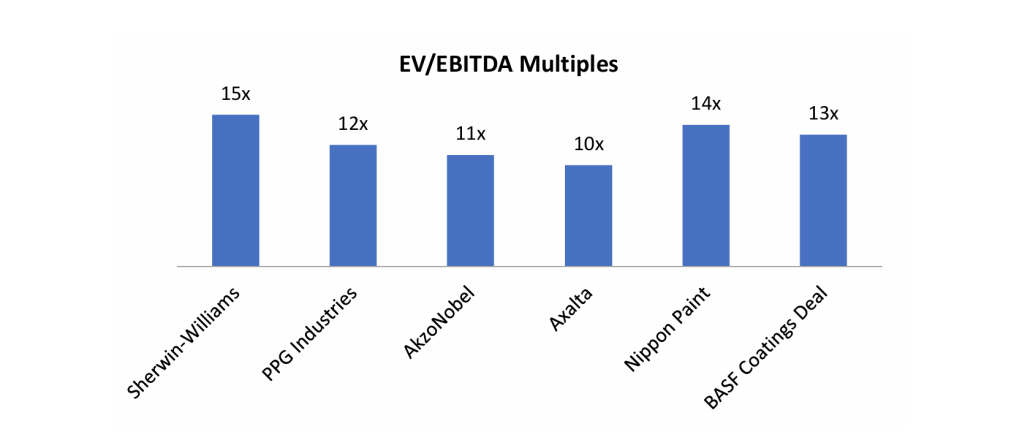

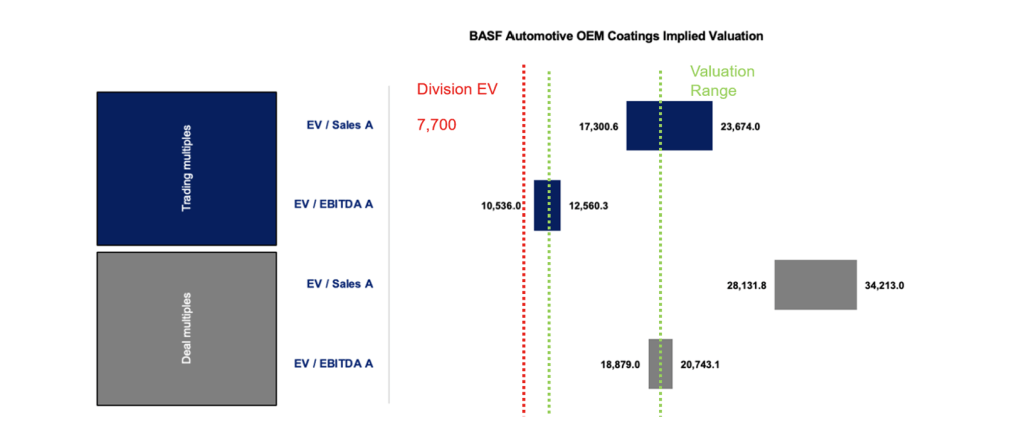

The €7.7 billion transaction in which BASF SE agreed to sell a majority stake in its Coatings division to The Carlyle Group LP and the Qatar Investment Authority (QIA) represents a significant strategic turning point for all parties involved. The transaction allows BASF to concentrate its portfolio on its core businesses in chemicals, agricultural solutions, and materials, while offering Carlyle and QIA the opportunity to acquire a leading global coatings platform with established market position. BASF will receive approximately €5.8 billion in pre-tax cash proceeds at closing and will retain a 40 percent equity interest in the new coatings entity. The deal’s implied valuation multiple of around 13 times EV/EBITDA reflects investor confidence in the division’s profitability and strategic relevance. AS shown in the chart, this valuation sits comfortably within the mid-teens range at which major global coatings producers such as Sherwin-Williams, PPG Industries, AkzoNobel, Axalta, and Nippon Paint, typically trade. The figure illustrates that the BASF Coatings transaction was priced boadly in line with sector benchmarks, consistent with the characteristics of established coatings businesses that exhibit resilient cash flows and defensible competitive positions.

From a strategic and financial perspective, value creation in the new entity is expected to arise from three broad areas: operational, commercial, and financial. Operational improvements are anticipated as the coatings business becomes an independent company with direct control over its production network, procurement activities, and logistics processes. BASF has noted that the carve-out will allow the business to operate without the structural constraints of the Verbund system, which integrates production across multiple chemical value chains (BASF, 2025)[12].While specific synergy figures have not been disclosed for this transaction, BASF and Carlyle have indicated that operational simplification and independent governance will be key elements of the future strategy.

Commercial synergies are expected through greater strategic focus on core application areas such as automotive OEM coatings, refinish coatings and surface-treatment technologies, which constitute the backbone of the business being sold (European Coatings, 2025)[13]. Public statements by BASF and Carlyle highlight planned investment in research and development capabilities, particularly in technologies aligned with sustainability requirements. The business has an established global presence, providing a basis for continued participation in long-term demand trends in transportation, industrial coatings, and mobility-related surface solutions.

Financial synergies relate primarily to BASF’s deleveraging and capital-allocation objectives. The €5.8 billion cash inflow will be used to strengthen BASF’s balance sheet, and the company has stated that the transaction will support its ability to invest in higher-margin areas within its portfolio. BASF will retain a 40 percent equity stake, enabling ongoing participation in the business’s future development while transferring operational responsibility to Carlyle and QIA.

The transaction timeline, as communicated by the parties, provides for closing in the second quarter of 2026, subject to regulatory approvals (Chemical Processing, 2025)[14]. Following the signing of the agreement in October 2025, the transition period will focus on establishing standalone structures for governance, information technology, procurement, and supply-chain management. The full operational separation is expected to take place over an extended period, consistent with the complexity of the business and its global footprint.

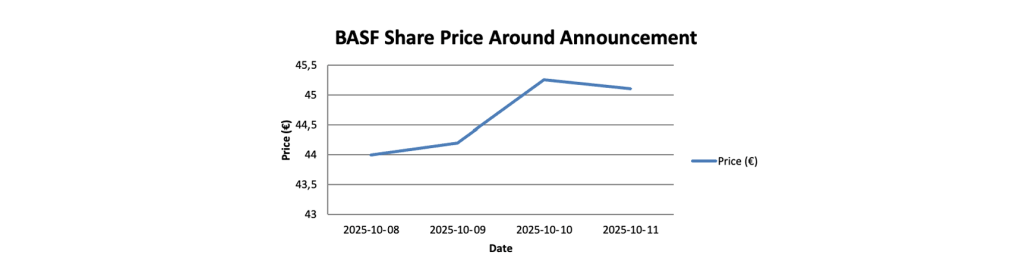

Market reaction to the announcement was broadly positive. News coverage of the sale highlighted that the deal was perceived as strengthening BASF’s balance sheet and simplifying its portfolio at a time of significant pressure on chemical companies operating under elevated energy and regulatory costs (Robotics and Automation News, 2025)[15].

Taken together, the BASF Carlyle QIA agreement reflects a structurally coherent transaction that balances BASF’s strategic shift toward a more focused and financially resilient business model with the buyers’ objective of acquiring a global coatings business with strong market positions. While the final outcomes will depend on execution, regulatory conditions and market dynamics, the deal aligns with established patterns in specialty-chemicals portfolio restructuring and represents one of the most significant European coatings-sector transactions of the mid-2020s.

The chart compares valuation multiples across major global coatings producers, including Sherwin-Williams, PPG Industries, AkzoNobel, Axalta, and Nippon Paint, alongside the implied multiple for the BASF Coatings transaction. The data show that the BASF deal was priced broadly in line with sector benchmarks, falling within the mid-teens range typical for established coatings businesses with resilient cash flows and strong market positions.

Deal Structure

BASF first announced it would be looking to sell its coating business in December 2023 to boost its earnings. By May 2025 it had sent out information to potential buyers of the division for an auction-style sale that was estimated to start at €6 billion. JP Morgan and Bank of America acted as financial advisors while Latham & Watkins provided advisory on the legal side. Carlyle ultimately outbid the unspecified offers from private equity investors AKPS Capital Partners, Lone Star Funds, and Platinum Equity as well as strategic investor Akzo Nobel. The official announcement of the acquisition deal came on October 10th, 2025, and stated their agreement to an enterprise value of €7.7 billion for the automotive OEM coatings, automotive refinish, and surface treatment businesses, which represented €4.3 billion out of BASF’s €69 billion total revenues. The remaining part of BASF’s coatings business, decorative paints, had been previously sold to Sherwin-Williams in a transaction that concluded in October, bringing the total enterprise value of the entire coatings division to €8.7 billion. BASF was able to quickly conclude the sale of the complete coatings division as part of their plan to gain value announced in 2024.

Post-transaction, BASF will retain a 40% equity stake in the coatings business, which had generated €4.3 billion in sales in 2024 throughout Europe, Asia Pacific, South America, and North America. For BASF, pre-tax cash proceeds are expected to be €5.8 billion. While information on the precise ownership breakdown between Carlyle and QIA is limited, together they will hold a 60% majority stake. The deal, however, remains subject to unspecified regulatory approvals, which is not expected until the second quarter of 2026. While Bank of America and Goldman Sachs are putting together a €4 billion debt financing package, more specific information is expected on the exact financing and structure terms in upcoming formal filings and regulatory disclosures (BASF SE, 2025).[16]

Indicative Valuation

Methodologies

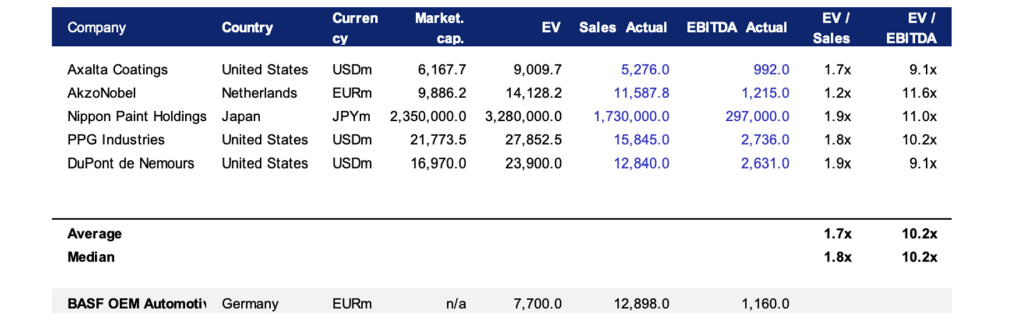

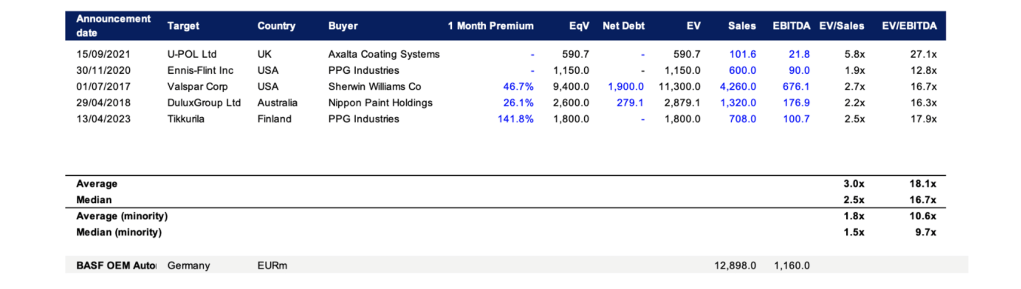

We employed comparable company analysis to value the BASF division sold off to Carlyle. We used comparable publicly listed companies and comparable precedent transactions, primarily focusing on companies that produce automotive coatings. BASF does not provide standalone financial statements for its coating business, and therefore an intrinsic cash flow-based valuation was not possible.

The images attached below summarize our findings.

We estimate the median multiples on EV/Sales as 1.8x, on EV/EBITDA as 10.2x for comparable listed companies.

Precedent transactions provide us with median multiples of 2.5x for EV/Sales and 16.7x for EV/EBITDA. The acquisition premium is estimated to be around 71%; it follows that the implied multiples for a non-controlling stake are 9.7x EV/EBITDA and 1.5 for EV/Sales, coming very close to the multiples for listed companies. These findings yield valuation ranges of 11,136-19,347 for the division’s implied enterprise value, which we summarize in the following football field:

Conclusion

Overall, our analysis shows that the valuation of the BASF coatings division remains consistent across methods, despite the absence of standalone financial statements. Public peers trade around 1.5x EV/Sales and about 9.7x EV/EBITDA. Precedent deals, once the estimated 71% control premium is removed, arrive at nearly identical multiples. This tight convergence strengthens the credibility of the implied EV and signals that investors view the division as a steady, established business rather than a fast-growth opportunity. For Carlyle, long-term value will need to come from operational gains, sharper commercial execution, and a more focused strategic direction.

Authorship Disclosure

Head of the Industrial Division: Emilio Cornejo

Industrial Division Analysts: Gioacchino la Rosa, Alberto Jimenez, Gianfranco Jr Sovernigo, Seungjae Kim, Lorenzo Agnello

Valuation & Modelling Analysts: Marcos Caiado, Gabriel Neumann

Bibliography:

- BASF SE. (2024). BASF Annual Report 2024.

- BASF SE. (2024). Combined management’s report: Fundamentals of the group — Economic environment Chemical industry. In BASF Report 2024.

- BASF SE. (2025, October 10). Joint news release: BASF and Carlyle reach binding transaction agreement on coatings business to create a leading standalone company. Retrieved from https://www.basf.com/global/en/media/news-releases/2025/10/p-25-203

- ChemXplore. (2025, October 10). BASF sells majority stake in Coatings unit to Carlyle for €7.7 bn.

- Financial Times. (2025, October 10). Carlyle nears €7 bn deal for BASF unit.

- Fortune Business Insights. (2024). Paints and coatings market size, share & industry analysis, by resin type (acrylic, alkyd, epoxy, polyurethane, polyester, and others), by technology (waterborne, solventborne, powder, and others), by application (architectural, automotive, wood, industrial, and others), and regional forecast, 2024–2032.

- Grand View Research. (2024). Paints and coatings market size, share & trends analysis report by technology (waterborne, solventborne, powder), by resin (acrylic, epoxy, alkyd, polyurethane), by application, by region, and segment forecasts, 2024–2030.

- Investing.com. (2025). BASF shares rise as investors applaud €7.7 bn coatings sale.

- McKinsey & Company. (2024). Petrochemicals 2030: Reinventing the way to win in a changing industry.

- Reuters. (2025, October 29). BASF’s Q3 operating profit beats consensus on better volumes.

- The Carlyle Group. (2018). AkzoNobel closes sale of Specialty Chemicals to The Carlyle Group and GIC [Press release].

- The Carlyle Group. (2024). Annual Report 2024. Retrieved from https://www.carlyle.com/investor-relations/annual-report-2024

- The Carlyle Group. (2025). The Carlyle Group Annual Report (referenced for AUM, performance data).

- The Wall Street Journal. (2025, October 10). BASF to sell majority stake in coatings unit to Carlyle for $6.7 billion.

[1] The Carlyle Group, Annual Report 2024 (2024), retrieved from https://www.carlyle.com/investor-relations/annual-report-2024

[2] Chemical & Engineering News. (2024). Global chemical sales rankings. c&en.

[3] BASF SE. (2024). BASF Annual Report 2024. BASF SE.

[4] BASF SE. (2024). The BASF Verbund system. BASF SE.

[5] BASF SE. (2025). Corporate website. Retrieved from https://www.basf.com

[6] Guertzgen, S. (2015, May 5). The impact of shale gas on the global chemical landscape. IndustryWeek. https://www.industryweek.com/supply-chain/article/21965092/the-impact-of-shale-gas-on-the-global-chemical-landscape

[7] “Rising forces: Future of the GCC chemical industry.” (2025, February 27). GPC-Chem. https://gpcachem.org/2025/02/27/the-chemicals-industry-in-the-next-decade-key-transformations-shaping-the-future/

[8] Beaumont & Bailey. (2025, January). Strategy & Outlook for the Global Chemicals Industry in 2025. https://www.beaumontbailey.com/wp-content/uploads/2025/01/Strategy-Outlook-for-the-Global-Chemicals-Industry-in-2025-FINAL.pdf

[9] McKinsey & Company. (2024, December 18). The state of the chemicals industry: Time for bold action and innovation. https://www.mckinsey.com/industries/chemicals/our-insights/the-state-of-the-chemicals-industry-time-for-bold-action-and-innovation

[10] “BASF to sell coatings business to Carlyle in EUR 7.7 billion deal.” (2025, October 10). European Coatings. https://www.european-coatings.com/news/markets-companies/basf-to-sell-coatings-business-to-carlyle-in-eur-7-7-billion-deal/

[11] “BASF’s €7.7B divestment signals accelerating industry carve-outs.” (2025, October). Breakthrough Marketing Technology. https://breakthroughgroup.com/market_watch/basf-sells-majority-coatings-business-carlyle-qatar-investment-authority-2025-10-10/

[12] BASF SE. (2025, October 10). BASF to sell coatings business to Carlyle and QIA in EUR 7.7 billion transaction. https://www.basf.com/global/en/media/news-releases/2025/10/p-25-203

[13] European Coatings. (2025, October 10). BASF to sell Coatings business to Carlyle in EUR 7.7 billion deal. https://www.european-coatings.com/news/markets-companies/basf-to-sell-coatings-business-to-carlyle-in-eur-7-7-billion-deal/

[14] Chemical Processing. (2025, October 13). BASF to sell majority stake in coatings unit to Carlyle, QIA. https://www.chemicalprocessing.com/industrynews/news/55323024/basf-to-sell-majority-stake-in-coatings-unit-to-carlyle-qia

[15] Robotics and Automation News. (2025, October 16). BASF and Carlyle to form €7.7 billion standalone coatings company with QIA investment https://www.roboticsandautomationnews.com/2025/10/16/basf-and-carlyle-to-form-e7-7-billion-standalone-coatings-company-with-qia-investment/95626/

[16] BASF SE, “Joint news release: BASF and Carlyle reach binding transaction agreement on coatings business to create a leading standalone company,” October 10, 2025, retrieved from https://www.basf.com/global/en/media/news-releases/2025/10/p-25-203

You must be logged in to post a comment.