The Deal

In September 2014, the Italian Government issued a decree regarding the privatization of the state owned company RAI Way S.p.A. (from now on, RWay). The decree came after the decision to list the company; indeed, due to the delicate role the tower sector plays in the country, the Government fixed some legal restrictions aimed at granting the company to serve the public interest even after the privatization process. One of these restrictions was that no more than 49% of RWay would have been sold by the Minister of Economic and Finance (the legal shareholder).

IPO

November the 18th, the IPO price was 2.95€ per share with a capitalisation of 802.4 millions euros; the day after, first trading day, it closed at 3.088€ per share, up 4.67%. During the IPO 30.51% of the shares has been listed, remaining majority and control to RAI S.p.A., unique shareholder pre – IPO.

Bid

2015, February the 25th, EI Towers announced its bid for RWay, 4.5€ per share valuing the company 1.225 billions euros (market cap at the time of bid announcement was 1B€). The bid came in a very complicated political scenario; other than that, the restriction imposed by the September dated decree on RWay privatization is still in place and, given the terms of the bid (at least a 66.67% stake), it forced the Italian Government to reject the bid on February the 27th, two days later. The same day, Citi published a report on the (media) tower sector in Italy, explaining that a consolidation would be extremely profitable and would generate more cash in a context where investments are capital intensive and the leverage already at high levels. In the same report, Citi increased the target price both for EI Towers and RWay at 55€ and 4.5€ per share respectively, rating buy, due to evident synergies that would benefit EI Towers. For institutional investors, RWay is considered as being a bond (cash cow status) with interesting M&A opportunities.

The Content

Despite favorable feedback from investors, the operation presents some issues of legislative, regulatory and political nature.

In fact, EI Towers launched its offer in order to get to own 100% of RWay- or at least 66.67%- and then delist it from the Milan stock exchange. However, the decree concerning RWay public listing states that the majority (51%) of the company must always remain State-owned.

In addition, Consob is opening a file with respect to the operation to ensure that competition won’t be compromised by the deal.

Last but not least, political pressures play a fundamental role in the game. Berlusconi family owns Mediaset and Berlusconi himself is the leader of the main right wing Italian party, which does not take part in the executive but can exercise a strong influence in the parliament.

As a result, different points of views exist on the matter, especially regarding competition issues. One school of thought argues that competition will be eliminated by the merger, whereas another one states that competition is actually worldwide and Italian companies have not enough capital to do well in this globalized context because of market fragmentation: concentration, in particular in telecom and media sector, should be welcomed.

Terms and structure

The offer values RWay’s shares €4.5, thus bringing 100% of equity value at €1.225bn through a cash and stock transaction. In fact, shareholders would receive per each share both a cash component of €3.13 (69%) and 0.03 new EI Towers issued shares (39%). JP Morgan would support Mediaset on the €851mln cash payment.

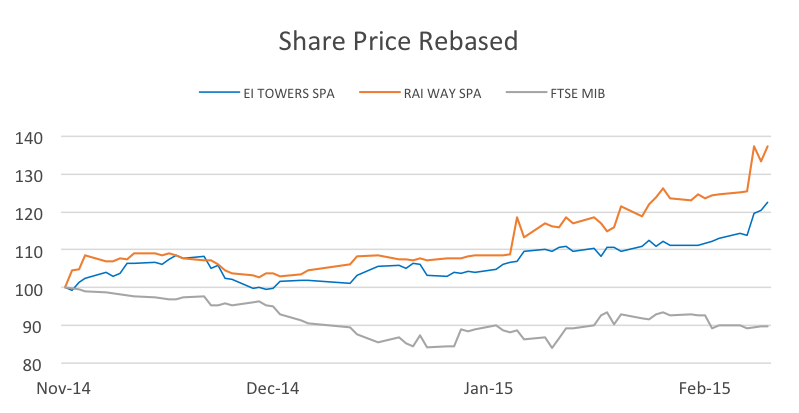

The market seem to approve and trust the deal as RWay closed the first day after the announcement gaining 9.46% on Milan stock exchange- the share price reached €4.05, not distant from the actual offer. Furthermore, stocks of neither the bidder nor the target stopped their rally after the issues raised by Italian government and antitrust.

The proposed price per share incorporates a premium of 22% with respect to prices registered before it was presented and of 52.7% if we consider the first trading day of the new listed company.

Through the merger, EI Towers intends to achieve synergies and overcome the actual market fragmentation. This will create a single big player and align the Italian market to the rest of Europe, where a single national operator is the standard.

Company Description

Mediaset S.p.A

Mediaset S.p.A is a multinational media group providing commercial television broadcasts mainly in Italy and Spain. In Italy, Mediaset S.p.A operates in mainly two areas: network infrastructure services and management, and integrated television operations.

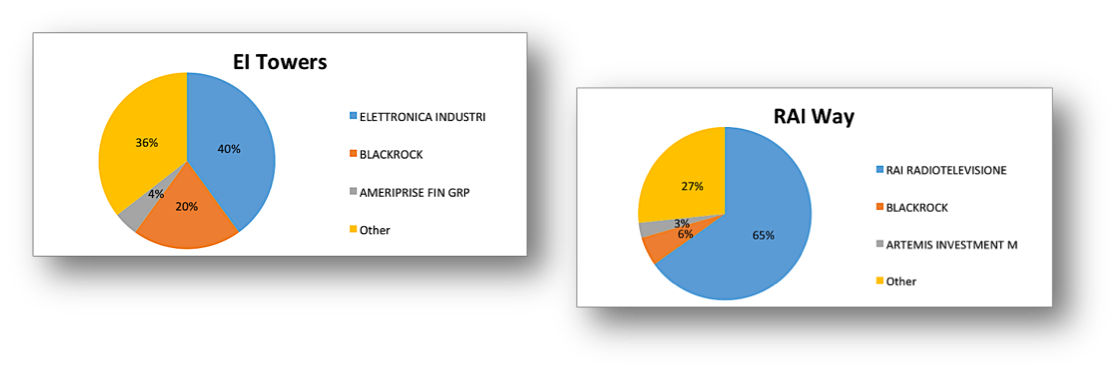

Mediaset’s network infrastructure services and management operations comes from its 65% holding in EI Towers. Ei Towers is an independent tower operating in Italy and it engages in network infrastructure management and provides electronic communications services for mobile transmissions and television and radio broadcasting. Furthermore, it manages broadcast contribution links for Mediaset Group through its own operations centres and network infrastructures.

The company’s integrated television operations offer variety of free TV channels to air and pay TV channels on football, cinema, documentaries and children’s channels.

In addition, Mediaset S.p.A is the main shareholder in Mediaset Espana, which is the Spanish commercial television operator with two main general interest channels, including Telecinco and Cuatro.

Radiotelevisione italiana S.p.A

RAI (Radiotelevisione italiana S.p.A) is Italy’s national public broadcasting company, owned by the Ministry of Economy and Finance. RAI provides many television channels, radio stations. It is the biggest broadcaster in Italy and it competes with Mediaset, Skyitalia and Telecome Italia Media.

Scenarios

The context in which the bid came is complicated under many sights, political, industrial and legal.

- Political because, as explained before, RAI Way S.p.A. is a state owned company, part of a delicate sector (media towers) and because EI Towers is owned by Mediaset, the principal competitor for RAI S.p.A. (owner of RWay); furthermore, Mediaset is property of Berlusconi family, politically involved.

- Industrial because the media towers’ sector is an hot topic, it has to be reformed and consolidation is probably the best choice under an economical point. But EI Towers and RWay are not alone: Telecom is the other giant player. Telecom is considering the split of its division owning the towers for its listing, following EI Towers (2004) and RWay (2014) ones.

- Legal because, as a state owned company, RWay is protected and partially regulated by special laws, one of which is the previously named 2014 September decree on its privatization.

Analysing the possible scenarios in this tremendously complicated context is not an easy task; many interests are in place, economic and political. The followings are few scenarios that we can prospect at the day of writing (February the 27th):

- The deal will take place in its today terms: although this could be done from an industrial point, legal restrictions and political interests make this scenario not probable.

- RAI and Mediaset will equally split the RAIWay ownership: this scenario is more probable from a legal and political point but in industrial and strategic terms, it is unlikely that EI Towers and Mediaset will commit so much capital in an acquisition that substantially does not give them full control over the company.

- The deal is a fake: it is unlikely that the board of EI Towers has not considered the legal restrictions on the acquisition and the political situation. Following this idea, and recalling that EI Towers is part of the Fininvest universe, it could be that this deal is a fake; Fininvest already knew that it could never work and it’s using it just as a currency (in political terms) to finally get the acquisition of RCS Libri by Mondadori; indeed, a “no” over this deal would strengthen the bargaining power of Fininvest, increasing the likelihood of a “yes” in the deal over RCS Libri.

- NewCo among RAI, EI Towers and Telecom: given the necessity for a consolidation in the sector, it could be that all the towers will be put in a NewCo serving in a more efficient and functional way all the three players. This is the best scenario from an economical and industrial standpoint, but the fact that one of the three participants would be a state owned one would probably turn away private investors over the fear of an increasing bureaucracy and decreasing efficiency.

As this article is being written, the situation is evolving; stay tuned for further information.

Sources: © 2015 Bloomberg L.P.

To contact the authors:

Sangwook Park theo.park@hotmail.com

Davide Petrangeli petrangelidavide@gmail.com

Oskar Kwasny oskar.kwasny@studbocconi.it

Ilias Sberveglieri ilias.sberveglieri@studbocconi.it

To contact the editor responsible for this article:

Ilias Sberveglieri ilias.sberveglieri@studbocconi.it