Competitiveness

The TMT industry (in a broad sense) is becoming more and more complex:

- From the demand side, emerging markets are asking for new services to be provided and developed countries are asking faster and better services (overall in data quantity). This translates in more quantity (emerging markets) and more quality (developed country).

- From the supply side, this huge demand pushes more and more businesses to expand to telecom services, including, just to mention a few, Google and Liquid Telecom (fibre network in Africa).

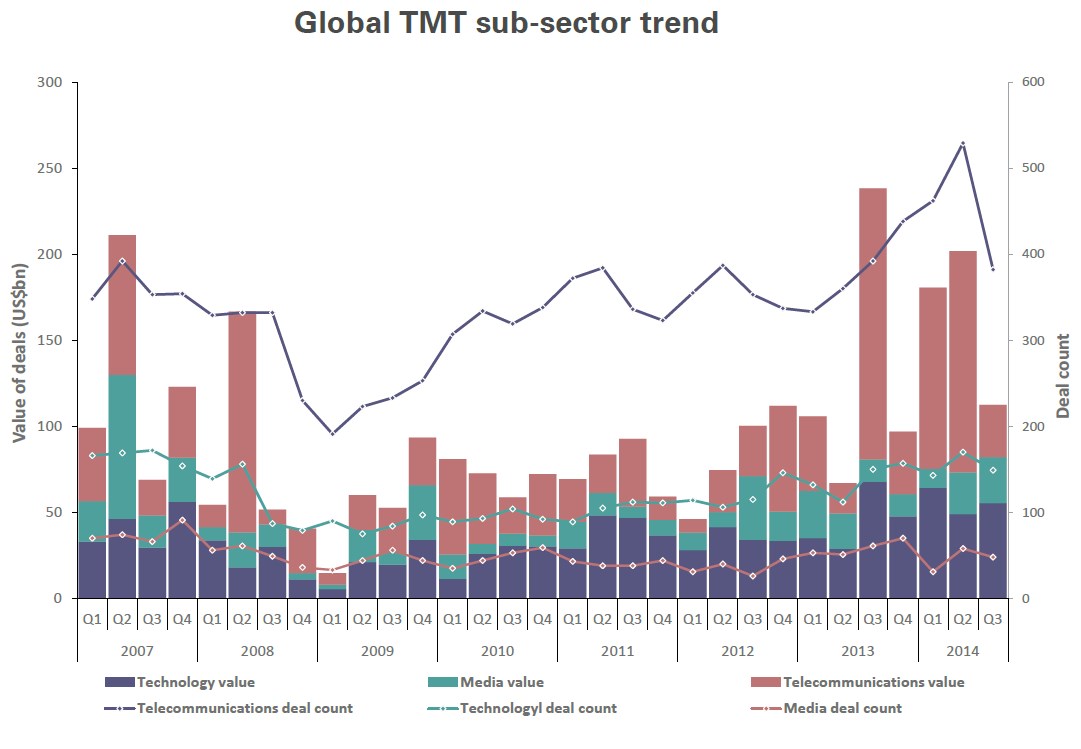

To recap: more demand pushes more supply. More supply translates into more competitiveness, with all the consequences it implies: lower prices to customers, better services, better customer care et cetera. This translates inevitably in lower returns on capital. Investors don’t want this (who would?) and push their managers to increase the power and competitiveness of the firms they are running. Furthermore, with lower return on capital, fewer capitals are available for net CAPEX (new investments) and, in one of the most capital-intensive industries, this translates in fewer innovations (fewer new infrastructures) that don’t match the demand of “more and better” coming from the customers (that, by the way, are willing to pay for the services). What the investors want from their managers is, thus, more competitive and remunerative firms: in other words, they want to invest in successful and innovative businesses, that is, conglomerates. This, indeed, is the consolidation trend in the TMT industry: to create conglomerates with larger customer bases, higher returns, more efficient and more innovative. This is the main reason why TMT related M&A set a new record in deals during 2014; and the trend is likely to be just at the beginning.

TMT M&A Forum 2015

The trend characterising the TMT industry is the main focus of the TMT M&A Forum 2015 that will be held in London, March 19th, organised by ©tmtfinance.com and sponsored by some of the leading financial institutions worldwide. The Forum will cover a set of hot topics, some of which are of our interest:

- Telecoms M&A: covering the consolidation wave driven, as just explained, by the increased competitiveness and investments needs;

- Infrastructure ownership: the ownership of the infrastructures is crucial in this context; the companies owning the infrastructures will face the challenges arising from ever – faster pace of infrastructure renewals; regarding this topic we’ve covered the case EI Towers on Rai Way last week;

- Convergence and Media: as long as there is consolidation, someone will profit from the convergence; another key question to address is how this consolidation process will change the way customers benefit TMT industry products; likely, new big conglomerates will have huge capitals to be invested, to increase efficiency and set new innovations;

- Financing: deals, and in particular big deals, need services from financial institutions, starting from advisory to financing. The way investment banks and other key financial institutions will approach the industry trend is likely to be a key driver of how the industry will look in its future.

Other main topics will be discussed, like the role regulation will have in characterising TMT future. The consolidation trend makes TMT probably the hottest industry for investment banks and other financial institutions (like M&A boutiques) and consulting firms at the moment.

NXP to Buy Freescale

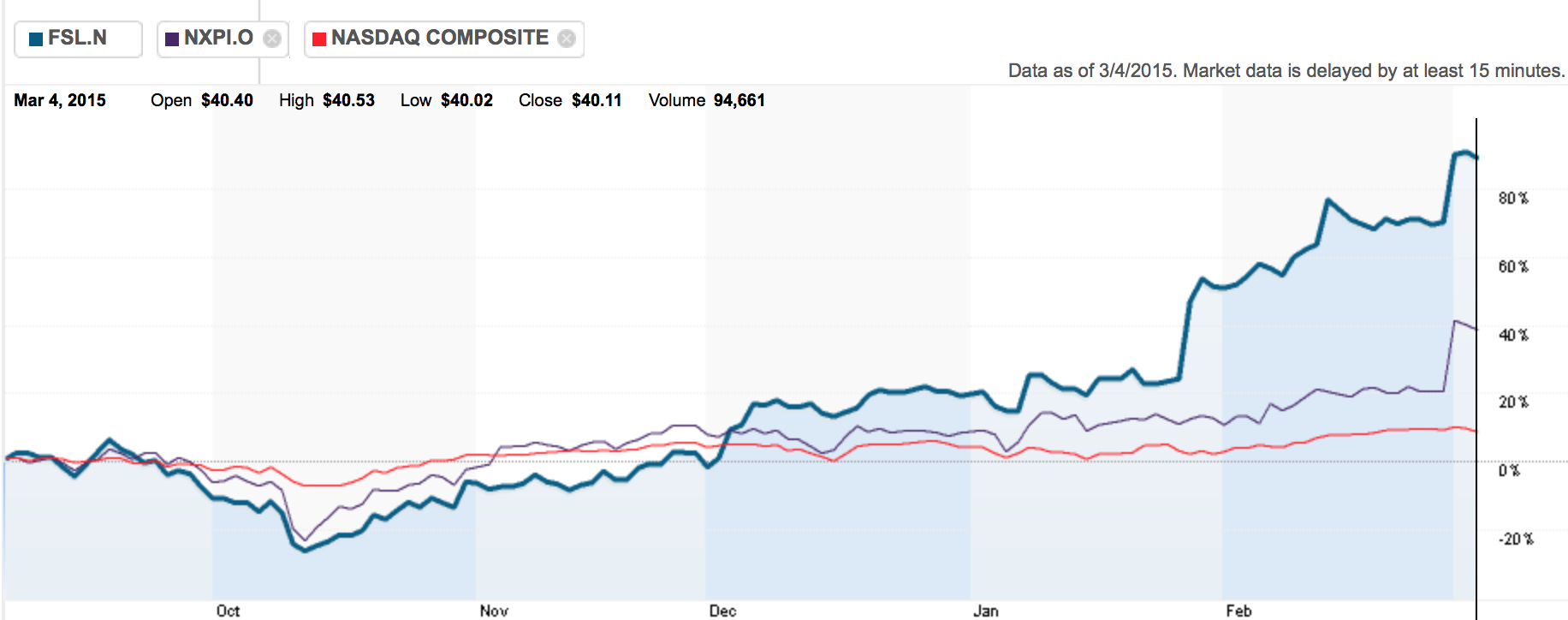

Confirming the consolidation trend in the industry, NXP Semiconductors is on the point of buying Freescale, thus creating a company with a combined enterprise value of $40bn.

NXP- once part of Philips- is a Dutch Nasdaq-listed company that produces credit and debit cards’ chips and has a market capitalization of $21.4bn.

On the other side, US rival Freescale was once a division of Motorola and now makes chips for automotive, consumer, industrial and networking markets.

Through the offer Freescale is valued $11.8bn and shareholders will receive on a single share basis $6.25 in cash and 0.3521 NXP shares- thus getting to own a third of the new company.

NXP will finance the transaction issuing $1bn new debt and 115mm new shares as well as using $1bn cash.

Shares of both companies have risen by more than 50% during the past year as Internet of things has pushed demand for chips. In addition to this, NXP already provides Apple with NFCs for the iPhone 6 and now stands to benefit from a deeper collaboration with the company founded by Steve Jobs.

Credit Suisse, Simpson Thacher & Bartlett and De Brauw Blackstone Westbroek advised NXP, while Morgan Stanley and Skadden advised Freescale.

NXP is not alone

NXP on Freescale would not be the first transaction in the chip-making field. Last year, Qualcomm bought UK-chipmaker CSR in a £1.56bn deal, while German chipmaker Infineon Technologies acquired the US group International Rectifier for about $3bn.

If we consider instead the entire TMT sector, even much bigger transactions happened during 2014.

The Comcast offer for TimeWarner ($68.5bn), the acquisition of Directv by AT&T ($65.5bn) and that of WhatsApp by Facebook ($16bn) are only three of the most significant examples.

Sources: ©2015 Bloomberg L.P. – ©2015 Valuewalk.com

To contact the authors:

Davide Petrangeli petrangelidavide@gmail.com

Ilias Sberveglieri ilias.sberveglieri@studbocconi.it

To contact the editor responsible for this story:

Ilias Sberveglieri ilias.sberveglieri@studbocconi.i