CHAPTER 1

On April 15, 2015 Nokia announced a €15.6bn offer for Alcatel-Lucent that will create a huge Finnish-French rival to Ericsson and Huawei in the telecoms equipment industry, with a market capitalization of about €40bn and sales of about €27bn, matching those of Ericsson.

Industry Overview

Nokia, the world’s dominant maker of handsets in the pre-smartphone era, lost its leadership after missing smartphone revolution. Nevertheless, it has recovered since selling the mobile handset division to Microsoft in September 2013 which helped return the company to profitability last year. In addition to this, Nokia is also thinking of selling its mapping software, Here.

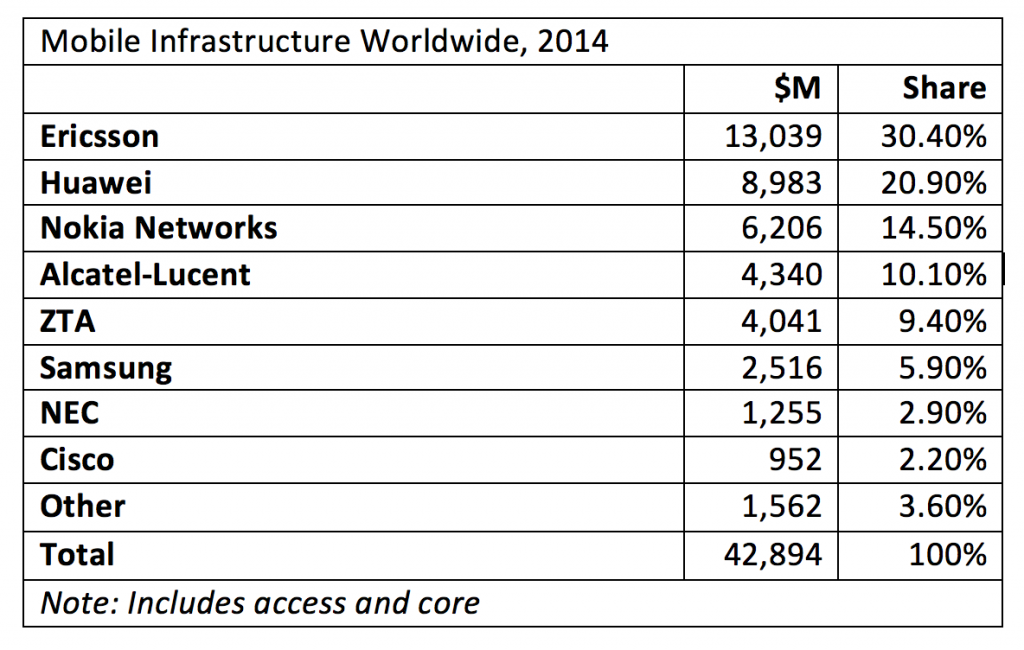

That is because by the end of 2013 Nokia had decided to place its bets for the future entirely on the telecom-equipment business, buying out Siemens from the joint venture in July. That business will be further strengthened by the Alcatel-Lucent deal, placing Nokia on an much better footing in terms of revenues with Sweden’s Ericsson, the market leader, and China’s up-and-comers Huawei and ZTE.

Despite the new challenge of global migration to wireless technology, both companies seem to have put the worst behind them after painful restructurings: Nokia’s shares have tripled in the last two years, while Alcatel-Lucent’s have quadrupled, as the two have started to diversify business away from mobile carriers.

Transaction Drivers

Through the merger the two companies are expected to achieve €900m of cost synergies by 2019 and €200m in reduced interest expenses by 2017.

As part of the deal, Nokia also committed to spend €100m on setting up an investment fund to back French start-ups.

The combined company would have had revenues of €25.9bn last year, making it slightly bigger than Sweden’s Ericsson and China’s Huawei, which lead the telecoms equipment industry.

Nokia said the joint company would have had underlying operating profit of €2.3bn, reported operating profit of €300m and net cash of €7.4bn assuming the conversion of both groups’ convertible bonds.

As a result, the merger would enable the two companies to share the high costs of research and development as well as the capital expenditure. On the other side Nokia will exploit Alcatel‘s relatively strong position in North America, a region in which Nokia has only begun to make headway again following a deal with Sprint.

Terms & Structure

In this all stock-financed transaction, 0.55 of a newly issued ordinary share of Nokia would be offered in exchange for each share of Alcatel-Lucent. Nokia’s shares rebounded on Wednesday 15 April, rising 4.7% to €7.84 after falling 3.6% on Tuesday. Alcatel’s suffered the reverse phenomenon, falling 9% to €4.06 after a 16% jump on Tuesday.

Based on Nokia’s share price on Wednesday 15 morning, its offer is worth €4.31 per Alcatel share compared with a value of €4.12 at Tuesday’s closing prices. We speak of roughly 28% premium over the French group’s average stock price over the past three months.

Alcatel-Lucent shareholders would own 33.5% of the fully diluted share capital of the combined company, and Nokia shareholders would own 66.5%, assuming full acceptance of the public exchange offer. While the combined business will remain headquartered just outside Helsinki, France will continue to be important as “a major center for innovation”, creating several hundreds of new positions in research and development in the country targeting new graduates.

According to Rajeev Suri, CEO of Nokia, the deal will be completed during the first half of 2016 “at the earliest”.

In addition, from a regulatory standpoint Nokia and Alcatel will need to convince authorities in nine countries including the US and China that their proposed tie-up will not impair competition in an already heavily consolidated telecoms equipment market.

Advisors

J.P. Morgan served as financial advisor to Nokia and delivered a fairness opinion to the Board of Directors of Nokia in connection with the transaction. Skadden, Arps, Slate, Meagher & Flom LLP and Roschier, Attorneys Ltd served as legal advisors.

Zaoui & Co is acting as lead M&A advisor to Alcatel-Lucent and delivered a fairness opinion to the Board of Directors of Alcatel-Lucent in connection with the transaction. Sullivan & Cromwell LLP served as legal advisor.

Meanwhile, Nokia first quarter results have been published… read more on our update of this story next to come.

To contact the author of this story:

Davide Petrangeli davide.petrangeli@studbocconi.it

To contact the editor responsible for this story:

Ilias Sberveglieri ilias.sberveglieri@studbocconi.it

You must be logged in to post a comment.