A new Pharma Mega-Deal making Botox and Viagra join forces.

On November 23, 2015, Pfizer announced its $160bn tie-up with Allergan to form the world’s biggest pharmaceutical company by sales.

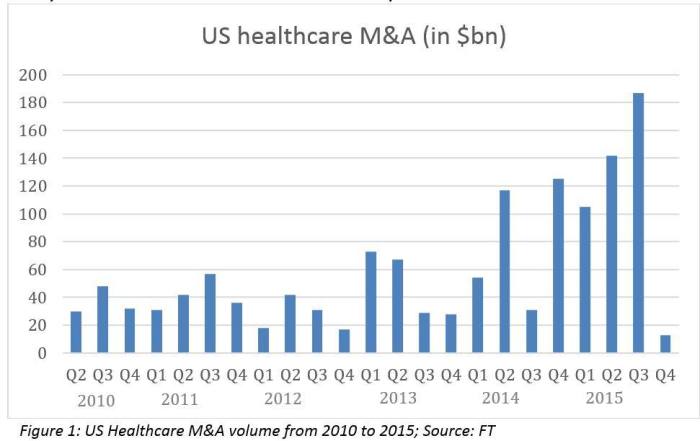

Industry Overview

Even though recent M&A activity has started to slow down in the healthcare sector, the announced merger shows that the M&A frenzy is not over yet.

Pharma M&A activity has been soaring to new heights this year with no other industry even coming close. Furthermore, the pharma deal volume has been record-breaking for several reasons. Not only has it overtaken last year in terms of both deal value ($448.2bn compared to last year’s $326.5bn) and number of deals (448 to 326 deals last year), but also left the second largest industry – technology – far behind. Including Pfizer’s deal in the graph below, this year’s value would even exceed the years 2012, 2013 and 2014 combined.

The US has been the main driver for M&A activity, accounting for nearly half of the total global M&A volume and several policies have helped the M&A rush. First of all, many US-based companies bought foreign companies in order to evade corporate taxes. In fact, the US corporate tax is the highest corporate tax rate in the developed world with 39.1% compared to the OECD average of 24.8%. However, both the current Obama administration as well as the front-runners for the presidential election Hillary Clinton and Donald Trump have questioned such practices and stated that they would do everything to prevent companies from evading taxes. Second, the Affordable Care Act has disrupted the American healthcare landscape and lead in return to consolidations of healthcare providers who are trying to increase their bargaining power. Third, an analysis by KPMG shows that this year alone pharmaceutical companies could lose up to $44bn in sales due to patent expirations. In order to offset decreases in revenues many firms have turned to buying competitors to strengthen their drug portfolio.

Pfizer Inc. is one of largest multinational pharmaceutical corporations located in the US and offers solutions for a wide range of medical disciplines including immunology, oncology, cardiology, diabetology and neurology. Pfizer’s revenues have been declining for the last three years and are currently at $49.6bn (2014). The company has always been quite busy with its M&A activity and according to Thomson Reuters, it was involved in 6 out of the 20 biggest pharma deals. It should also be noted that the Allergan deal would supersede Pfizer’s Warner-Lambert deal in 1999 to be the largest deal in the healthcare industry.

Allergan plc (formerly known as Actavis plc) is a pharmaceutical company based in Ireland. It has already been involved in several acquisitions this year including the sale of its generic drug business Actavis to Teva. The most notable brands in its drug portfolio include Botox, Namenda and Latisse.

Timeline

On Thursday, October 22, 2015, Pfizer announced its intention to buy Allergan in a deal, which would be the biggest in the healthcare industry and the biggest tax inversion in history. The “preliminary friendly discussions” of details of the transaction followed in the days ahead. On Sunday, November 22, 2015, Pfizer Inc. and Allergan plc announced that their boards of directors had unanimously approved the deal terms, and hence the companies had entered into a definitive merger agreement.

Deal Terms

Dublin-based Allergan (NYSE: AGN) will merge with New York-based Pfizer (NYSE: PFE) in order to allow the American drugmaker to benefit from the tax inversion advantages that will reduce its current tax rate. The newly created company will be in fact based in Ireland.

The deal values Allergan shares at $363.63, which corresponds to a premium of around 30% based on the closing price registered on October 28, 2015. It can therefore be inferred that the total value of the deal will be around $160bn. Allergan shareholders will receive 11.3 shares of the new company for each of their old Allergan shares, while the conversion ratio for Pfizer shareholders will be 1:1. This is because the price of the new shares has been set at $32.80, corresponding exactly to Pfizer’s closing price on November 20, 2015 (the last trading day prior to the official announcement).

Allergan shares did not move noticeably following the official announcement made on November 23, 2015 and they closed on November 27, 2015 at a price of $319.76, more than 10% below the value set for the merger. Pfizer shares fell by around 2.6% following the announcement just to recover and close at $32.79, almost perfectly in line with the share price of the new company.

Looking at the long-term graphs, Pfizer’s stock price has been quite volatile over the last months, and it has fallen by around 7.5% starting from October 28, 2015. Allergan’s price per share has suffered from the same volatility of the American company over the same period but, as mentioned before, it surged by around 30% from October 28, 2015.

Goldman Sachs, Guggenheim Partners, Centerview Partners and Moelis & Company are advising Pfizer, whereas Allergan is advised by JPMorgan and Morgan Stanley.

Deal drivers

Following the unsuccessful bid to buy AstraZeneca last September, Pfizer Inc. found the perfect target to slash corporate taxes by concluding the largest M&A deal in the pharmaceutical industry through the $160bn acquisition of the Dublin-based Allergan plc.

The main driver for this acquisition is certainly tax inversions. In 2014, Allergan only paid 4.8% in corporate fees as opposed to 25.5% for Pfizer. Through this controversial technique, large firms whose revenues come significantly from foreign markets are able to re-incorporate in another country with a lower corporate tax rate, Ireland in this case.

In fact, Pfizer will reduce its tax burden to 17-18% when the deal will be concluded. This transaction has been seriously condemned by the U.S. Treasury Department and by politicians, including President Barack Obama, who defined the transaction as “unpatriotic”. However, as Pfizer’s CEO Ian Read told the Financial Times, this deal should be considered as “a great deal for the US, given that it frees up [our] ability to invest in the American science”. In addition to the one-off tax saving of $21bn generated by the merger, Pfizer will be able to repatriate to the US $30bn in cash trapped overseas at a reasonable cost.

The merger is not expected to create value for stockholders in the immediate future, as the P/E ratio of Allergan is significantly higher than the one of Pfizer − respectively 40.6 and 24.5 − resulting in a dilutive EPS process. However, Pfizer’s EPS are expected to be neutral in 2017, accretive starting from 2018 and more than 10% accretive in 2019.

Another important reason that had a strong impact in negotiations was the market share Pfizer would gain after the merger. With more than $63.5bn in revenues and with a market capitalization in excess of $320bn, Pfizer would become the largest pharmaceutical firm worldwide preceding the current leader Johnson & Johnson. The company would have an excess of cash in hand valued around $70bn, arising from the sale of Allergan’s generic business to the Israel-based Teva for $40bn last July and from the cash Pfizer accumulated overseas.

Moreover, the merger would allow Pfizer to move a step forward towards its will to split itself into two separate entities. As some people familiar with the matter reported to The Wall Street Journal, the firm will now have the possibility to focus on two main areas, as they are large enough to stand on their own. The first one will focus on innovative patent-protected products, such as Pfizer’s breast-cancer drug Ibrance and Allergan’s blockbuster Botox, whereas the second one will focus on established products with expired patents drugs. The split, which is likely to take place in 2018, will boost profitability as in-patents drugs command higher prices and have a higher expected sales growth.

Another aspect that would bring benefits to the Irish company will be a sole 6.25% tax on patents developed in Ireland; this coincides with Pfizer’s policy of cost reduction over the next few years, which will free up more cash to be invested in R&D.

Dealing with corporate leadership, Ian Read (CEO of Pfizer) will continue to serve the company as CEO, personally gaining $186m from this operation. Brenton L. Saunders, actual Allergan’s CEO, will assume the position of Chief Operating Officer (COO).

Sources and References: Seeking Alpha, Fortune, Financial Times, Reuters, Pfizer website/annual report, Heritage.org, Allergan website, KPMG

To contact the authors:

Federico Campanini federico.campanini@studbocconi.it

Giorgia Caruso giorgia.caruso@studbocconi.it

Federico Cattani federico.cattani@studbocconi.it

Lukas Klemend lukas.klemend@studbocconi.it

Basile Zurcher basile.zurcher@studbocconi.it

To contact the editor responsible for this article:

Alexandra Heidemann alexandra.heidemann@studbocconi.it

You must be logged in to post a comment.