On September 14th, 2016, Bayer has reached a deal, currently pending regulatory approval, to acquire Monsanto in an all cash transaction for $128-a-share ($56bn Equity Value, $66bn EV)

COMPANY OVERVIEW – BAYER

Bayer AG (ETR:BAYN , Market Cap: €77.57bn, Share Price: €93.90 as of 11/11/2016) is a German multinational chemical and pharmaceutical company traded on the Frankfurt Stock Exchange.

Bayer’s core business activities include human and veterinary pharmaceuticals, consumer healthcare products, agricultural chemicals, biotechnology products and high value polymers.

Bayer’s strong innovation culture has played a substantial role in making 2015 another record year for the company. Analysing its financial performance, Bayer’s EBITDA has grown steadily over the last five years, rising from €6.9bn in 2011 to €9.6bn in 2015 (CAGR of 6.8%), while revenues have moved from €36.5bn up to €46,3bn in the same time period (CAGR of 4.9%). Bayer has been also able to defend and marginally improve its strong EBITDA margin of around 20%, considering that pure pharma companies have an average value of 22%, but Bayer is also involved in the Agritech business, where margins are much more compressed (usually significantly below 10%).

The share price (see graph in the last paragraph) has been following a comparably positive trend over the 2011-2015 period, but starting from April 2015, when it hit the record price of €146.20, the trend has surprisingly reversed, with shares dropping to lows of just above €85 in May 2016. Considering that the S&P Pharma Index also peaked between April and July 2015, it is possible to suggest that systematic factors, namely the price gouging controversy that sparked general outrage and subsequent promises by presidential candidate Clinton to enforce regulations and price limits had she been elected, have dented Bayer’s performance too. Following Mr. Trump election last week, the price has jumped from around €88 to €94 (+6.8%), possibly heralding an increase in confidence in the sector and in its earning potential.

To strengthen its position as one of the largest companies in the pharmaceutical sector (6th in terms of earnings in 2016), Bayer strategy for the future will remain focused on a strong R&D program. Between 2011 and 2015, Bayer increased its annual research and development spending from €2.9bn to €4.3bn. Management has also recently announced plans to invest in the division a further €4.5 billion in 2016 only, which is more than ever before. Another potential growth source, especially in terms of increased efficiency and leaner processes, will be represented by the new Bayer Life Science Center, created to further develop and implement innovative technologies developed by startups and universities.

COMPANY OVERVIEW-MONSANTO

Monsanto Company (NYSE: MON , Market Cap: $42.90bn, Share Price: $97.90 as of 11/11/2016), headquartered in St Louis (Missouri, USA), is a multinational agriculture corporation traded on the New York Stock Exchange. It pioneered the application of biotechnologies to agriculture, promoting the introduction of transgenic plants and conducting field trials of genetically modified crops.

Monsanto produces seed brands both in large and small-acre crops, develops in-the-seed trait technologies (from pest to disease to drought resistance) and it also manufactures a vast array of herbicides, including the world famous and controversial Roundup. Monsanto’s business is divided into two main segments: Seeds and Genomics, which comprises its seeds and traits divisions, and Agricultural Productivity, including crop protection and herbicides. The company considers the former the main driver of its future growth, whereas the latter provides with its products a substantial capacity to supply the market, granting to the company the capacity to maintain pressure on margins.

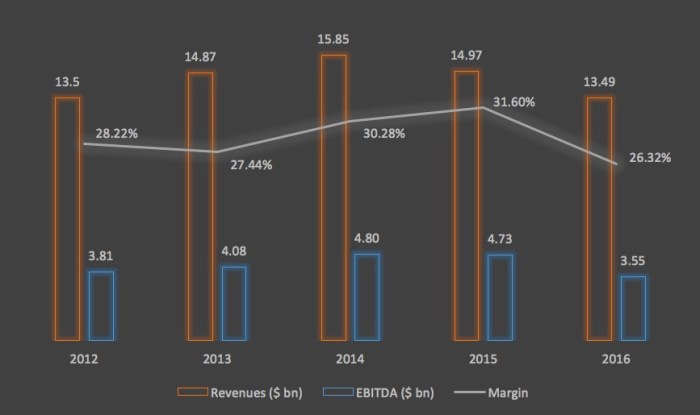

In terms of historic financial performance, Monsanto sales provide a mixed picture, as they increased from $13.5bn in 2012 to $15.85bn in 2014 for then to decline to $13.49bn in 2016 (CAGR: -0.02% Note: Monsanto’s fiscal year ends in August). EBITDA has been following a similar path, from $3.81bn in 2012 to $4.8bn in 2014 and then down to $3.55bn in 2016 (CAGR: -1.72%). Also thanks to its dominant position and unique product range, Monsanto has been able to maintain a remarkable EBITDA margin level over the last years, but this ratio has experienced in 2016 the same kind of sharp decline that has impacted revenues, highlighting the difficulties companies have in managing fixed costs in presence of significant and sudden drops in the top line.

The stock (see graph in the last paragraph) has risen mimicking the strong performance posted in the 2012-2015 period, raising from just above $80 to over $120, for then to experience a rapid contraction that brought the shares’ value back to around $84. Only after the rumor of a potential acquisition from Bayer started to spread, the price broke even the $110 level in a moment of probably excessive enthusiasm among its shareholders and has since then partially “retreated” to levels close but below the $100 mark.

As the numbers suggest, things have started going south for the Company starting in 2015, and specifically in March of that year, when the WHO declared glyphosate, the world’s most commonly used weed-killer, a “probable human carcinogen.” This ingredient is the back-bone of Monsanto’s Roundup and many of its seeds are specifically designed to resist this herbicide. Moreover, there is an ongoing effort made by many countries to regulate and limit the use of toxic chemicals in the products used in agriculture, and this could potentially spell doom for the company. Another macro-element that has significantly contributed to Monsanto’s lagging performance has been represented by commodity prices, on a constant slide since their peaks of 2013/2014, and this has led farmers to cut back on spending. Finally, the strong dollar paired with price cuts on certain products determined by the intense competition have played a major role as well.

Monsanto has recently started to roll out plans to cut over 2500 employees to partially counter these headwinds and to return to deliver growth to its shareholders as soon as possible. Monsanto’s strategy for the future will necessarily remain focused on R&D, where the company has spent over the last four years $1.5bn in each year on average trying to develop, among others, new biotech traits, to advance the genomic research and to envisage improved formulations of the crucial Roundup herbicide. Monsanto appears uniquely positioned to deliver integrated solutions for its customers and will try to focus on leveraging this advantage to stimulate its long-term growth.

INDUSTRY OVERVIEW

The agricultural industry has been consolidating at a steady pace for decades. The M&A wave of the 1990s concentrated more than half of the agricultural biotech patents of the decade in the hands of just 10 players, down from the over 600 independent seed companies that were active in 1996 and that have since been bought out. Today, 63% of the global seeds market is in control of the big six – Monsanto, Syngenta, Bayer, DuPont, Dow Chemical and BASF. In the 2008 report “Who owns nature?” published by ETC (a group working to address socioeconomic and ecological matters), several issues  that are common also to the most recent consolidation spur in the sector were analyzed. At that date, the top 10 seed companies accounted for 67% of the global market (with Monsanto alone reaping one quarter of global sales) and with the top 10 agrochemical players controlling an astounding 89% of the broader global market. The group concerns were focused in particular on product overlapping rather than on market shares per-se: “the world’s six largest agrochemical manufacturers are also seed industry giants”, read the ETC report.

that are common also to the most recent consolidation spur in the sector were analyzed. At that date, the top 10 seed companies accounted for 67% of the global market (with Monsanto alone reaping one quarter of global sales) and with the top 10 agrochemical players controlling an astounding 89% of the broader global market. The group concerns were focused in particular on product overlapping rather than on market shares per-se: “the world’s six largest agrochemical manufacturers are also seed industry giants”, read the ETC report.

Sector consolidation can on one side be a sensible thing: with in-house R&D of agrochemical capabilities, it is possible to engineer seeds and crop sprays that optimize production when bought in bundle. On the other hand, in the words of BASF head of crop protection Markus Heldt, “farmers want the freedom to choose, they want choice and alternatives-They don’t just want to be dependent on 3 to 4 [suppliers] on a global scale”. There is then one more factor that comes into play: the increased barriers to entry. The big vertical players can engineer integrated products that require farmers to purchase the full package, effectively locking out small competitors.

Sector consolidation can on one side be a sensible thing: with in-house R&D of agrochemical capabilities, it is possible to engineer seeds and crop sprays that optimize production when bought in bundle. On the other hand, in the words of BASF head of crop protection Markus Heldt, “farmers want the freedom to choose, they want choice and alternatives-They don’t just want to be dependent on 3 to 4 [suppliers] on a global scale”. There is then one more factor that comes into play: the increased barriers to entry. The big vertical players can engineer integrated products that require farmers to purchase the full package, effectively locking out small competitors.

Moreover, innovation in the agricultural industry business is and will remain crucial in order to address some of the biggest “upcoming” world problems. With the global population forecasted to soar past 9 billion by 2050, crop yields will need to rise by 60% for sufficient food to be grown on existing farmland, and the benefits of advanced seeds, indeed, include stronger pest resistance, streamlined weed control and more efficient harvest around the world.

DEAL DRIVERS

Mr Baumann and Mr Grant (CEOs of Bayer and Monsanto respectively) claim that there is no significant overlap in the businesses of the two giants, which is partly true considering that Bayer’s strength is in the chemicals products that protect crops while Monsanto specializes in seeds and genetic traits. Moreover, Monsanto has a much bigger presence in the US and Latin America while Bayer has its “strongholds” in Europe and the Asia-Pacific region. It is however highly likely that Bayer will have to sell out its cotton seeds business to avoid creating a behemoth controlling 70% of the whole US market supply. The same faith will probably be faced by either Roundup (Monstanto) or Liberty Link (Bayer). Indeed, they not only belong to identical product lines (consisting of glyphosate weed-killer and glyphosate-resistant seeds), but they have been also used by farmers as complementary products when crops start developing resistance to either one of the sprays.

Considering the deal is pending regulatory approval, it is worth noting that the merger plan will be filed in over 30 different jurisdictions. In the US, the justice department usually takes an “holistic” approach and looks at the overall consequences for the market. A similar method is adopted in China, while in Europe the regulator adopts a “first come, first served” principle, where the company planning a merger needs to commence the pre-notification procedures with the commission before the announcement, and to ensure that it can announce the transaction and notify on the same day. However, it is plausible that no extreme hurdles in selling overlapping units will be faced during the process, considering that BASF refusal to take part in the recent M&A frenzy will almost certainly compel the company to buy the assets sold off in the Bayer-Monsanto, Dow-DuPont and ChemChina-Syngenta tie-ups to try to remain competitive.

From a synergistic point of view, the idea of creating a global “one-stop shop” selling seeds, crop sprays and advice to farmers has significant potential. The main criticism, timewise, has been however that there will be only four global seeds players left by next year, down from the current six. This consolidation wave comes at a very delicate time for farmers: commodity prices have fallen so low that some producers struggle to just breakeven. The net cash farm income is expected to decrease for the third year in a row in 2016: while crop yields have been going up over time, the prices of biotech-engineered seeds have increased even faster, a problem that has been correlated with lack of competition.

Among the possible obstacles to the completion of the deal, the tarnished reputation of Monsanto, mainly due to its genomic research, has brought about a wave of protests and petitions to stop this “marriage”. Despite years of research having provided no evidence that genetically engineered crops pose risks to human wellbeing, with the National Academies of Sciences experts panel concluding that there is no “substantial evidence” of health or environmental damages, the general opinion is quite the opposite, to the point where genetically modified crops are subject to prohibitions in 19 EU countries.

The general shift in focus from increasing the global food supply to enhancing the quality of food, coupled with falling crop prices, has led to a decrease in demand for crop protection chemicals. The high costs and long timeline of R&D innovation make it a necessity to streamline processes, either by downsizing or by consolidating. Moreover, the just-started digitalization of the agricultural industry means that bigger firms will be able to invest more and have more capabilities to increase crop yields and “farm better, farm smarter”. Under this point of view, the impact of mega-mergers on innovation presents both significant pros and cons: it could be positive (the elimination of overlapping initiatives could free up funds to pay for other researches) but also negative (with lower competition the quest to develop new products would be reduced). Some experts argue that, in a worst-case scenario, innovation will continue outside the R&D laboratories of the big players, probably in the context of academia or thanks to smaller firms, which would suggest more M&A activity is to be expected down the road.

DEAL STRUCTURE

On September 14th 2016, Bayer has finally announced to have clinched the acquisition of Monsanto for $128-a-share in an all-cash transaction. The agreement was reached after over 4 months of talks and after the German drug and chemical maker upped for 3 times its original $122-a-share offer ($125 in July and $127.50 in early September). Bayer will in the end pay a 44% premium over Monsanto’s share price on May 9th 2016, the day before Bayer’s first written proposal. Bayer has also agreed to pay Monsanto a break-up fee of $2bn should the deal be rejected by antitrust regulators, and this represents a significant increase compared to the $1.5bn fee offered in July. Upon approval by regulators, the new company will become the largest agribusiness of the planet, selling 29% of the world’s seeds and 24% of its pesticides.

The transaction values the equity of Monsanto at about $56bn, for a total Enterprise Value of $66bn, implying an EV/EBITDA (LTM before unusual items) of 17.6x, significantly above the 9.0x multiple usually seen in comparable transactions. This clearly indicates how far Bayer has been ready to go in order to close the deal and how strongly it believes in the potential of this acquisition.

After the final announcement (red line in the graph above), Monsanto’s shares have risen by just 0.6% to $106.70. This low increase in price, still more than 20% below Bayer’s proposed acquisition price, reflects investors’ concerns about regulatory approval for a deal that would dramatically reshape the industry as a whole. Putting things into perspective, since this potential deal has become public in May 2016, Monsanto’s shares have however risen significantly from just above $89 (+19.9%), signalling a generally positive sentiment among investors regarding the new and improved perspectives for the company following the acquisition.

On a different note, Bayer investors’ reaction has been clearly negative since the company first disclosed it had entered into talks with the St Louis-based firm. Price dropped from €99.95 on May 9th to as low as €84.42 in the days following the announcement (It has since slightly recovered as detailed above, but is still trading below the price registered on May 9th), which represents a loss exceeding 15%. There is a number of reasons for such a reaction, and among those one of the main sources of concern appears to be related to the debt funding, that would leave the combined companies with a significantly increased debt burden. The acquisition will in fact lead to a sharp increase in Bayer’s leverage ratio. Moody’s estimates its total Debt/EBITDA to be around 4.0x by the end of 2017, compared with 2.2x on June 30th, 2016. To partially outweigh this, substantial free cash flow from Monsanto is expected to allow Bayer to reduce the ratio to close to 3.0x by the end of 2019.

Another cause for uncertainty is represented by the benefits Bayer will reap from this acquisition. Bayer’s brand has been historically associated with well know and widely used medicines and other treatments for humans, but would now be almost equally strongly linked to the agricultural business and in particular to seeds production (and among them to the genetically modified ones, that have contributed to the negative reputation Monsanto “enjoys” especially in the USA). Moreover, Bayer has recently reported strong third-quarter profits powered by its pharmaceutical division, while its crop science arm was basically flat. This has further enhanced some pre-existing concerns from shareholders, who have been questioning the rationale behind the possible decision to shift the management’s attention from the profitable pharma business to try and revamp the agrochemical division. Under this perspective, this acquisition might be the only solution for this area to remain viable in the medium-to-long term.

Regarding the structure of the deal, Bayer will fund the transaction with a combination of debt and equity. The equity component (of about $19bn) will be raised with the issuance of convertible bonds and a rights offer. In the meantime, Bank of America Corp., Credit Suisse Group AG, Goldman Sachs Group Inc., HSBC Holdings Plc and JP Morgan Chase & Co. have agreed to provide bridge financing of $57 billion.

The deal is expected to be concluded by the end of 2017. Morgan Stanley and Ducera Partners LLC are advising Monsanto, while Bank of America, Credit Suisse and Rothschild & Co. are on Bayer’s side. The total estimated fee pool (including the bridge financing) is estimated to be just shy of $700mn.

Sources and References: Nasdaq, Bloomberg, Reuters, Zephyr, Financial Times, Companies’ annual reports and websites, Wall Street Journal, Marketwatch, Standard and Poor’s

To contact the authors:

Federico Cattani federico.cattani@studbocconi.it

Marco Monaco marco.monaco@studbocconi.it

Elisa Forghieri elisa.forghieri@studbocconi.it

Adele Bertolino adele.bertolino@studbocconi.it

Umberto Armani armani.umberto@studbocconi.it

You must be logged in to post a comment.