General Electric and Baker Hughes reached a deal for the combination of their oil services business units. General electric will contribute its oil-and-gas business and pay $7.4 billion through a special dividend of $17.50 for each Baker Hughes share.

The new company will be 62.5% owned by GE and 37.5% owned by Baker Hughes shareholders.

Companies Overview

General Electric

General Electric Company (GE) is one of the largest American conglomerate corporations, specifically the eleventh biggest company in the U.S., as well as a component of the S&P500 and the DJIA. Its divisions comprise sectors which include: Engineering, Software Development, Medial Devices, Life Sciences, Pharmaceutical and Automotive. It is incorporated in New York and headquartered in Boston.

GE Oil and Gas, the division implicated in the merger, supplies equipment for the oil and gas industry across the entire value chain, including drilling, subsea, LNG, distributed gas, pipeline and storage, refinery and petrochemical. It has revenues of $16.5 billion, out of GE’s total revenues of $140 billion.

GE is listed on the NYSE with a total market capitalization of $275.2 billion at the time this article was published.

Baker Hughes Inc

Baker Hughes Inc. is the fourth biggest global provider of oilfield services at $27.6 billion, headquartered in Houston, Texas. It offers reservoir consulting and products for drilling, formation, evaluation, completion and production.

With 40,000 employees spanning across 90 countries, Baker Hughes is comprised out of numerous companies whose history can be traced back to the beginning of the 20th century. The company has large contracts with all Middle Eastern NOCs such as Saudi Aramco, Qatar Petroleum and ADNOC.

Baker Hughes is listed on the NYSE (BHI) with a current market capitalization of $24.5 billion.

Industry Overview

Oilfield Services companies play a crucial role in the oil industry and their tasks involve the phases of valuation and drilling of oil fields and the completion and production of oil rigs. Oilfield services industry is tightly linked with the oil industry, thus it is exposed to some of the same risks. Particularly, the profits of this industry are significantly influenced by the oil price. Moreover, the environmental concerns as well as the threats represented by renewable energies and the other issues afflicting the oil industry (e.g. geopolitical instability and uncertain energy policies) are relevant also for this specific sector.

Oilfield services companies have evolved from producers of components to broader and more complex providers of services. Nowadays, oilfield services firms have become main contractors which in turns subcontract some activities and tasks to other firms specialized in specifics areas. More generally, two kinds of contracts are mainly diffused in this industry. The first one is based on the payment of a certain sum to a general contractor, which is bound to complete its job (whether it is exploration, drilling, completion or production) for that amount. Hence, in this case, any eventual expense above the cap established by the parts is upon the contractor. Another possibility is that the oilfield services company provides a list including costs for fees, hours of work, components and tools. Once the task will be completed by the firm, the total cost will be based on the pre-specified prices. The latter is the most diffused contract, and it is less risky for the oilfield services companies.

The Oilfield Services industry is characterized by the presence of few companies accounting for a large share of the market revenues. More specifically, Schlumberger, Halliburton and Baker Hughes, the three biggest operators, represent almost 50% of total revenues.

This sector is also characterized by high capital requirements. Moreover, the workforce is highly specialized and the knowledge intensity is high, since the companies have to possess all the skills necessary to supervise complex phases. The government does not pose direct limits to competition, however some government policies that oblige companies to use only technologies and methods authorized by the laws indirectly raise the barriers to overcome. The return on invested capital (ROIC) of the oilfield services industry has been significantly higher than the one registered by the market as a whole. More specifically, the ROIC of the total market has averaged around 7% in the last three years, while the one of the oilfield services industry has gone from 19.64% in 2013 to 16.90% in 2015.

Structure of the Deal

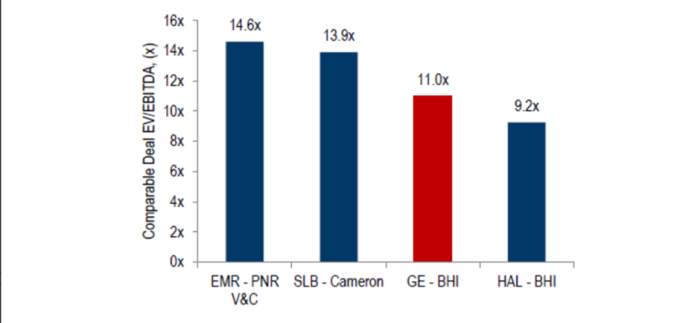

Coinciding with a recovery in oil prices, the structure of the deal, however complicated, is in favour of General Electric. GE is acquiring the oil and gas unit of Baker Hughes through a special dividend and a 62.5% stake in the new company. The special dividend is worth a total of $ 17.50 per share. GE was very strategic in this acquisition, as buying out all of Baker Hughes would have cost 3.5 times more: instead, GE only payed Baker Hughes shareholders a total of 7.4 billion which is debt-funded. However, instead of getting a loan through the debt market, GE has reached into its subsidiary, GE Capital, to get a 0% interest loan till 2019. Interestingly, GE’s stock price has varied quite little since the deal was realized, as this reflects the concerns of some investors that GE is paying too much for the deal.

Drivers of the Deal

Starting with synergies, a $1.6 billion synergy is predicted and being pitched to investors under the assumption that oil will recover to 60 dollars a barrel. In fact, synergies have been modelled at $ 0.5, 1.3, and 2.0 billion from 2018 to 2020 respectively together with segment margins, including synergies, increasing to 20.1% by 2020. However, the deal does hurt GE’s EPS in the short run, a projected decrease of 0.2 cents. This is mainly due to management selling off none-core assets which will reduce short-term sales. The long-term outlook by management will be instead profitable for GE and its shareholders who will be part of the second largest oil company. Again, for EPS the long-term outlook is in fact a 7% increase over the next three years and that will help move GE’s dividends up to a more attractive level.

This deal is excellent in the short term for Baker-Hughes investors who see a high premium for their shares and will own shares in a GE company which will become the second largest oil service provider in the world. Baker-Hughes has had seven straight quarters of negative earnings and will benefit tremendously from the synergies provided by the deal. For GE, the deal will provide long-term benefits to margins, EBITA, and EPS, as well as a much needed increase for GE’s dividend in the future. GE’s current route is to become a leaner company, with a very long-term focus. Even though these benefits will come to fruition at an arduous pace, GE will set to be a dominant company in the industrial sector for years to come.

Advisors

Financial advisors for General Electric were Centerview Partners and Morgan Stanley, while Shearman & Sterling provided legal advice. Goldman Sachs Group Inc. advised Baker Hughes on financial matters and Davis Polk was the company’s legal adviser.

Sources and References: Bloomberg, Companies’ websites, Financial Times, The Wall Street Journal, workboat.com

To contact the authors:

Matei Apolzan apolzan.matei@yahoo.com

Adrian Galer adi117ro@gmail.com

Marta Naidenova marta.naidenova@gmail.com

Stefano Rovelli stefanorovelli@hotmail.it

Malte B. Schmitter malte.schmitter@cass.city.ac.uk

To contact the editor responsible for this story:

Stefano Rovelli stefanorovelli@hotmail.it

You must be logged in to post a comment.