Rockwell Collins has officially announced the acquisition of B/E Aerospace. The transaction is expected to be completed in 6 months in the spring of 2017. The boards of both companies have approved the deal.

Rockwell Collins is expected to pay $34.10 per share in cash, representing a 22.5% premium with respect to the closing price prior to the day of the announcement. Overall, Rockwell Collins is expected to spend a total amount of $8.3bn for B/E Aerospace. The increased size will lead to a more established company in the market and better financing abilities due to the reduced business volatility by the enlarged product portfolio of the two companies.

Companies Overview

Rockwell Collins

Rockwell Collins, Inc. (NYSE: COL) is an American multinational company active in the Aerospace and Defense Industry listed on the NYSE. It has a market capitalization of $11.92bn as of end of September 2016.

Rockwell Collins was born in the post war years as the aerospace technology division of the Collins Radio Company after the parent company incurred some major financial difficulties. It was spun off in 2001 becoming one of the major avionics and information technology systems provider in the world. Based in Cedar Rapids, Iowa, the company employs about 30,000 people worldwide of which around 85% work in American facilities, 10% in EMEA and the remaining 5% in Asia.

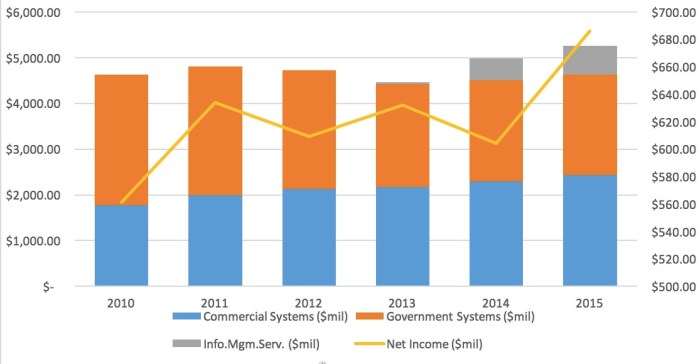

In 2015 the corporation registered sales for $5.244bn, an increase of 5.3% from 2014 and 15.7% from 2012. Rockwell Collins’ activities can be divided into 3 main divisions: Commercial systems, Government systems and Information Management Services. The Commercial systems division has as its main clients commercial and business airlines, airports and railways; it generated $2.434bn in 2015 with a 9% increase from the previous year confirming a longstanding positive trend. On the other hand, the Government systems division, which provides products for the military of all major Western nations, faced a slight decrease in sales to $2.187bn in 2015. This was mainly due to a sharp decrease in orders of Communication products and Surface solutions whereas the Avionics sales resisted. The Information Management Services division proved to be the main reason of the steady increase of sales in the past 4 years being a relatively new market for the company which managed to create $632m in 2015. The company invests continuously in R&D and recently increased these expenses getting to almost $1bn in 2015.

B/E Aerospace

B/E Aerospace, Inc. (NASDAQ: BEAV) is an American multinational company active in the Aerospace manufacturing industry. As of the end of September, B/E Aerospace’s market capitalization is 6.07bn. It is a world leader in manufacturing aircraft passenger cabin interior products both for the commercial and business aircraft market.

B/E Aerospace was founded in 1987 in Wellington Florida, where its headquarter currently is. The company’s history is marked by many acquisitions: in 1989 it acquired its major competitor EECO, in 1992 after a successful IPO on NASDAQ, it took over PTC Aerospace (seating products) and Aircraft Products Company (galley structures and inserts) and many others, such as Honeywell’s Consumable Solutions in 2008, in the following two decades.

The company has a workforce of about 10,000 people: 66% in manufacturing/distribution operations, 22% in R&D, 5% in sales/marketing and 7% in finance, H&R, IT, legal, general administration.

In 2015 the company registered sales of $2.73bn, an increase of 5% from the previous year and 75% since 2011, whereas net income was $285m in line with past results. Revenues were produced for 35% in North America, 24% in Europe and 41% in Asia, Pacific rim and Middle East, confirming the company’s leading position in emerging markets.

The activities of the company are divided into two segments: The Commercial Aircraft segment which is involved in the production of seating products (world leader); Equipment for food, beverages, preparation and storage; oxygen delivery systems; interior structures; and the Business Jet segment which provide interior cabin products for business jets, executive VIP seats and head of states aircraft. Even though the Business Jet segment increased double digits for many years whereas the commercial one increased in line with the industry, the Commercial Aircraft segment still represents the largest source of revenues (78%).

In 2015 the company kept its high percentage of expenses (10%) in R&D over the revenues, spending about $280m.

Industry Overview

Global Aerospace and Defense deal activity recovered slightly from the second quarter of 2016, with transaction volumes ticking up and an aggregate deal value holding steady. Areas of interest currently include identity, security services and additive manufacturing, addressing increasing opportunities and threats related to the industry’s technological advances. During the past four quarters, we have seen a 38% decline in M&A volume overall. Indeed, the global deal value YTD 2016 accounts for almost $18bn. The financial share of M&A activity has been on an upward trend. This quarter financial investors contributed 57% of deal value and 27% of deal volume, showing increasing outside interest in the sector. Uncertainty around the US election, Brexit, government spending and the global economy are holding the activity in check.

While we apparently expect volumes to recover, deal making for the remainder of 2016 may be more opportunistic in nature.

A&D companies are actively splitting public sector and commercial units and divesting lower margin businesses, such as IT services. The main players (i.e. Lockheed Martin) are consolidating or broadening leading positions in segments, allowing for focus on platforms. Restructuring, divestitures, and spin-offs also remain popular among A&D companies and diversified industrials. Companies are optimizing portfolios to simplify operating models, align with core capabilities, or to enter faster-growing markets. Commercial market exposure and specialty technology are among the two highest priority themes driving deal activity among defense contractors.

High-growth markets, including cyber security, electronic warfare, and UAVs continue to see strong deal activity. The market is still dominated by the two aerospace giants, Airbus, and Boeing, but the ability to get into space and to reduce costs is opening new scenarios to the companies that are actively researching the sector. Know how from little corporations and big capital from big firms interested in having access to space are reshaping the industry scenario.

Structure of the Deal

Under the terms of the agreement, B/E Aerospace shareholders will receive a total consideration of $62 per share. The consideration is broken down by $34.10 per share in cash, and $27.90 per share in Rockwell’s common stock, representing a 22.5% premium on the closing price prior to the day of the announcement. Further, the common stock portion is subject to a protective option strategy (collar) of 7.5% in the expectation of substantial long-position gains. Furthermore, the acquisition includes consideration conditions. In fact, if the volume weighted average price of Rockwell Collins common stock during the 20-day ex-post period exceeds $89.97, the stock portion of the consideration will be fixed at 0.3101 shares of Rockwell Collins common stock for each share of B/E Aerospace. Conversely, if it falls below $77.41 per share for the period, the stock portion of the consideration will be fixed at 0.3604 shares of Rockwell Collins common stock for each share of the target. Overall B/E Aerospace shareowners are expected to own 20% of the new entity. Rockwell Collins will be spending the equivalent of $6.4bn for B/E Aerospace plus the assumption of $1.9bn of B/E’s debt. The cash portion of the transaction is said to be financed with new debt, $1.5bn of which Rockwell Collins expects to pay down by the end of the fiscal year of 2019. Rockwell Collins values B/E at an EV/EBITDA multiple of 12.4x, which is above the average of 10.9x multiple for Aerospace M&A for the current year where an increasing role has been played by financial buyers, rather than strategic ones.

The transaction has been approved unanimously by the boards of both companies and it is expected to be completed by the spring of 2017. As financial advisers for the deal, Rockwell Collins hired J.P. Morgan, whilst B/E Aerospace has been advised by Citigroup and Goldman Sachs. Kadden, Arps, Slate, Meagher & Flom, Shearman and Sterling LLP served as legal counsels for the transaction.

Drivers of the Deal

External Deal Drivers

The slowing commercial aerospace market and pricing pressure from aircraft manufacturers Boeing and Airbus have made acquisitions attractive for larger suppliers. One factor for this development is the relatively flat US military demand and the softening in the commercial aerospace business after the boom in recent years. At this point it is reasonable for Rockwell Collins to fill out their portfolio and combine it with other strong franchises.

Internal Deal Drivers

Synergies

In the classical case of acquisitions by mature companies, revenue and especially cost synergies are the major driver of M&A transactions.

In short, Rockwell expects to generate significant run-rate cost synergies and over $6bn in free cash flow over the next five years with expected free cash flow conversion of greater than 100 percent. In addition, by leveraging the respective airline and OEM relationships, as well as Rockwell Collins’ business jet dealer network and military aircraft positions, the company firmly believes there are revenue synergies that create meaningful upside to their business case.

In detail, the run-rate pre-tax cost synergies are approximately $160m, of which 90 percent captured in the first full year of the acquisition. The cost savings come from eliminating public company administration at B/E Aerospace, greater buying power with suppliers, consolidating information technology system and using low-cost factory labor across the combined company. In combination with certain conforming purchase accounting adjustments it will result in improved pre-tax earnings of approximately $60m to $90m per year for the first six years after the acquisition.

Rockwell Collins Chief Executive Kelly Ortberg said in an interview that the combination offered substantial cost synergies and the ability to cross-sell electronics and plane fittings, and positions the enlarged company to lead the development of “smart” aircraft. Such advanced product offering will lead to classical up-selling effects and thereby to increased revenues.

Product Offering and Customer Benefits

The transaction combines Rockwell Collins’ capabilities in flight deck avionics, cabin electronics, mission communications, simulation and training, and information management systems with B/E Aerospace’s range of cabin interior products, which include seating, food and beverage preparation and storage equipment, lighting and oxygen systems, and modular galley and lavatory systems for commercial airliners and business jets. Thereby, the acquisition significantly increases Rockwell Collins’ scale and diversifies its product portfolio, customer mix and geographic presence.

This transformational acquisition is consistent with Rockwell Collins’ strategy to accelerate growth and build value through market-leading positions in cockpit and cabin solutions. The acquisition will enable the company to better serve commercial aviation, business jet and military customers through broader offerings.

Both CEOs feel confident that this combination delivers significant long-term benefits neither company could realize on its own.

Sources and References:

Company presentations, Bloomberg, Reuters, The Wall Street Journal, Financial Times, CNBC pressroom, Companies’ websites and New York Times.

To contact the authors:

Niels Carl niels.carl@studbocconi.it

Joerg Heilmair joerg.heilmair@studbocconi.it

Davide Martellozzo davide.martellozzo@studbocconi.it

Giuseppe Scavolo giuseppe.scavolo@studbocconi.it

Dima Pisaniuc dimitru.pisaniuc@studbocconi.it

To contact the editor responsible for this story:

Davide Magni davide.magni@studbocconi.it

You must be logged in to post a comment.