On the 15th of December the independent committee of Sky has approved to sell to 21st Century Fox 60.4% of its equity ownership at £10.75 per share. The agreement comes after two rejections by the committee in the previous days, and it represents the latest attempt of the Murdoch Brothers to acquire full ownership of the company after 2011 hacking scandal which involved the at-the-time 21CF’s parent company, News Corp.

Company descriptions

21st Century Fox

21st Century Fox [NASDAQ:FOXA; Share Price: $30.35 as of 27/02/17] is a leading premier portfolio of cable, broadcast, film, pay TV and satellite assets operating global across the six continents with more than 1.8bn subscribers. The top 5 institutional holdings include Capital Research Global investors, Dodge & Cox, Capital World Investors, Vanguard Group Inc. and State Street Corp. On July 1, 2015, Lachlan Murdoch was elevated to Co-Executive Chairman with Rupert Murdoch while James Murdoch replaced Rupert as a CEO. 21st Century Fox has been formed as a result of a split of entertainment and media properties from News Corporation in 2013. These include FOX, FX, FXX, FXM, FS1, Fox News Channel, Fox Business Network, FOX Sports, Fox Sports Network, National Geographic, STAR India, 28 local television stations in the U.S. and more than 350 international channels; film studio Twentieth Century Fox Film; and television production studios Twentieth Century Fox Television and a 50% ownership interest in Endemol Shine Group. At the same time, 21st Century Fox holds 39.1% ownership interest in Sky.

On July 25, 2014 they have announced the sale of Sky Italia and Sky Deutschland to BskyB for $9bn, subject to regulatory and shareholder approval in order to bid for Time Warner, for which they have also received $25bn from Goldman Sachs. In 2015, the new company National Geographic Partners have been formed from an announced for-profit joint venture with the National Geographic Society where the 21st Century Fox holds 73% of its stake.

Sky Plc

Sky Plc [LSE:SKY; Share Price: £996.00p as of 27/02/17] is a Europe’s leading entertainment company and largest pay-tv broadcaster with 21m subscribers and 30k employees as of 2015. They specialize in satellite broadcasting, on-demand internet streaming media, broadband and telephone services. James Murdoch, a CEO of 21st Century Fox is a chairman of the company, while the CEO have been replaced by Jeremy Darroch. The top 5 institutional holdings include Twenty-First Century Fox, Inc., Franklin Templeton Investments Corp., Invesco Advisers, Inc., BlackRock Investment Management Ltd. Legal & General Investment Management Ltd. Sky Plc has been created as a result of merger of Sky television and British Satellite Broadcasting in 1990. In July 2007, BSkyB announced a takeover of Amstrad for £125m with a 23.7% premium on its market capitalization. In 2014, they have additionally acquired Sky Italia and Sky Deutschland which allowed them to expand their operations across the Europe. Its other subsidiaries include Sky UK, Sky Ireland, Amstrad, The Cloud, Now TV (UK). On 4 June 2010, BSkyB and Virgin Media have reached an agreement for the acquisition by BSkyB of Virgin Media Television.

Sky’s strength relies in its profitability growth and its ability to convert most of its profits into cash within the fiscal year. A disciplined cost management in the past 6 years made sky’s revenue growth outpace its cost growth by 4% p.a. This successful formula has been achieved by paying attention to technological synergies and by successful investments in the OTT distribution market, which made sky the leading pay-tv platform covering live and video-on-demand. Additionally, this highly efficient financial model resulted in an average 100% conversion of profits into cash, which has led to decreasing net debt/EBITDA from 3.3x to 2.4x in past 2 years.

Industry

The golden years of pay-tv services might be approaching a step downhill. However, in the past decades, subscription based television services had grown very large and they entertained millions and millions of households in many countries around the entire globe. Nonetheless, as of today, a drop of Pay-Tv customers in most developed countries is expected to take place in the upcoming years. On the other hand, countries that are still growing their wireless infrastructures, are expected to see an increase in Pay-Tv subscribers. That is because with efficient data streaming tools, other competitors are conquering the market (e.g. on-demand services). Furthermore, cord-cutting, a pattern of viewers cancelling their pay TV subscriptions, is decreasing the number of customers as well.

Additionally, Pay-Tv penetration is Western Europe, where Sky has a strong presence, have constantly growing over the decade, and will peak around 60% in 2020. That shows the strong potential that Pay-Tv still carries and it explains why there is interest towards this area.

Comcast Co. is the leading Pay-Tv provider in the United with about 22.4 percent of the Pay-Tv market share in the U.S. Right after Comcast, DirecTV follows with an estimate of 20.3 percent of the market share, followed by Dish Network. For what concerns Europe, Liberty Global and Sky are the major players. In the Pay-Tv business, it is not rare to have single individuals who hold great power, such as Rupert Murdoch and John C. Malone.

Companies in this business earn their revenues through advertisement on the platforms and licensing of rights to broadcast specialty programs. The struggle in competing with alternative on-demand services has sparkled many M&A talks in the industry, such as French Vivendi’s hostile approach towards Mediaset or the recent talks between Time Warner and AT&T, which shows us how the sector is moving towards consolidating producers of contents and those who deliver them.

Strategic rationale

There are three different strategic drivers of the deal, namely synergies, technological know-how and geographical diversification.

Synergies

The dominant driving force of the deal are cost synergies. Analysts believe these to amount to quickly realizable $100m pre-tax.

The main factor of these synergies can be traced to the strategic relationship between Fox and Sky. Since its inception in 2013, 21st Century Fox owns 39% of Sky and has had a strategic relationship ever since. As a part of this relationship, the companies shared a lot their consumer content and brands. Both 21st Century and Sky own exclusive sport rights and production studios (see exhibit 1), which are hard to replace and thus are marketed at a premium. Hence, the internalization of these cost drivers, would allow the combined company to steeply increase margins.

Technological Know-How

Another driver is the ability of 21st Century Fox to acquire some of Sky’s technological know-how around its direct-to-consumer Sky-Go streaming platform. Fox poached some of Sky’s senior management that worked on Sky Go in recent years to position itself against new up-and-coming competitor Netflix. By buying Sky completely it can tap into the full extent of its direct-to-consumer technology and implement a serious alternative to Netflix in its home market.

Geographical Diversification

Lastly, the acquisition of Sky gives Fox further exposure to the European market by increasing Europe’s revenue share from 12% to 44%. Moreover, Fox can hope to leverage on its expertise to capture growth in some of the less developed European markets, such as Germany, Italy and Austria.

Terms & Structure

On the 15th of December, the independent committee of Sky accepted 21CF’s proposal to acquire the 60.9% equity ownership it doesn’t already own at £10.75 per share in an all-cash transaction. 21CF’s has added a break-up fee of £200m in case regulatory authorities don’t approve the transaction.

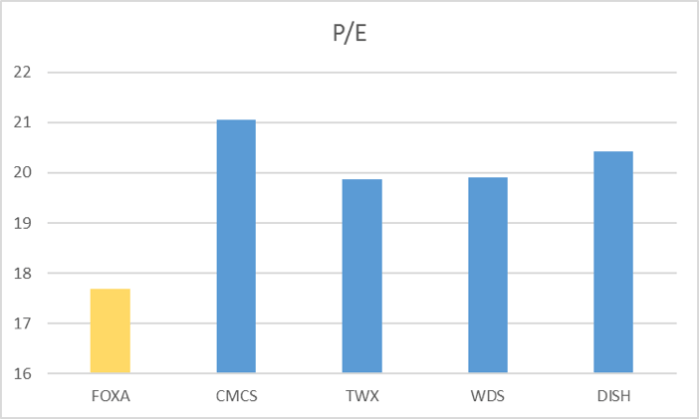

FOXA’s P/E has historically been around 17.4x throughout 2016, lower than the industry average as graph 1 shows, making FOXA’s stock a weak acquisition currency and explaining the choice of paying cash for this acquisition.

Deal gives Sky an Equity value of £19.2bn, at a 36% premium considering the closing share price on the announcement day and an implied enterprise value of £25bn, 11.4x its FY16 EBITDA, in line with the EV/EBITDA of many of its competitors like Walt Disney, Dish, CBS or 21st Century Fox which have an average metric of 11.4x. It is undervalued only if compared with Mediaset, undergoing an hostile takeover that has substantially increased its share price, which is showing an EV/EBITDA of 18.24x.

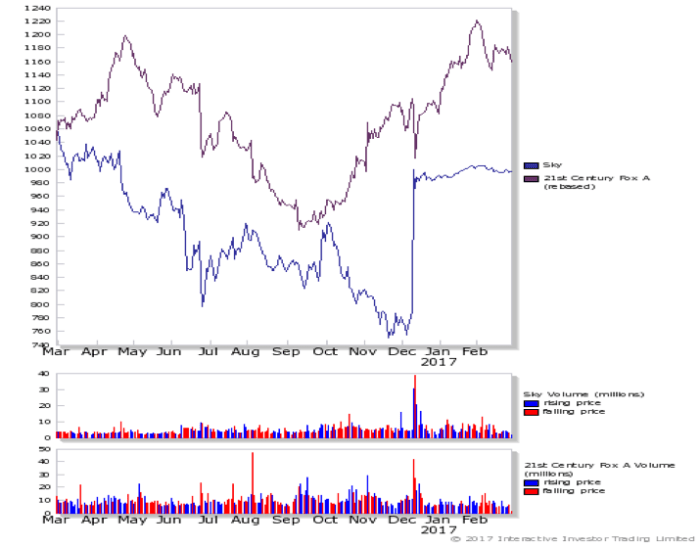

On the day of the agreement Sky’s share price rose 26.6% from £789.5p to £1000p. After a couple of days, investors have expressed disappointment about the effort of Sky’s board to the price negotiated, blaming it could have been higher. Indeed, demand for a successful company as Sky, who is showing leadership in the OTT distribution of its contents, should be high and should represents a big point in negotiations against an acquirer. Still, it is necessary to consider that the same 21st Century already owns 39% and that the eventual acquirer should co-exist with the current owner, which can be difficult to motivate as a possible successful proposal to current shareholder and therefore leads us to the conclusion that this represent a fair deal for Sky’s exiting shareholders.

FOXA fell 1.5% on announcement reflecting concerns about the effective necessity of an increase in Sky’s stake and doubts about regulatory approval, which has already derailed, back in 2011, Murdoch’s previous attempt to acquire BSkyB in the UK.

Transaction to be financed through a mix of cash and long-term debt, to be issued in GBP and that is going to replace the bridge credit facility agreed that is now ensuring capital will be available at the time of the closing of the transaction. Deutsche Bank, J.P. Morgan and Goldman Sachs have arranged a facility made up of two tranches for an amount equal to £12.2bn and have committed capital in an equal share. They are also lead financial advisers to 21st Century Fox America, and, therefore, will presumably arrange the bond issuance.

The interest charged for the advances of the facility amounts to the LIBOR plus an Applicable margin which will varies accordingly with public debt ratings (BBB+ according to last Fitch rating) and duration starting from the closing date as table shows. To give a sense, the applicable margin assuming a stable credit outlook to BBB+ would be in the range between 112.5bps and 187.5bps in the case the funds are borrowed for more than 270days, which represents a 3% spread with the average interest rate charged on 21CF’s latest bond issuances.

Deutsche Bank, Goldman Sachs, Centerview Partners and J.P. Morgan have acted as financial advisor to 21st century fox for this deal, while Morgan Stanley, PJT Partners and Barclays have advised Sky’s independent committee.

Sources and References: Bloomberg, Wall Street Journal, Financial Times, Companies’ websites and annual reports

To contact the authors:

Michele Di Paola michele.dipaola@studbocconi.it

Niklas Müller niklas.muller@studbocconi.it

Johnathan Riad johnathan.riad@studbocconi.it

Monica Chrost monicha.chrost@studbocconi.it

You must be logged in to post a comment.