Companies Overview

Consolidation is likely to remain the main answer to a series of concerns in the auto industry, from increasing production costs to high competition and more stringent environmental regulations. The merger between PSA and Opel reduces industry capital requirements by eliminating competition and combining two manufacturing and design footprints into one. This acquisition could pave the way for a series of mega-mergers like the one desired by Sergio Marchionne between FCA and GM.

PSA Group

Founded in 1976, PSA Group is a French automotive company that is the result from the merger between Citroën SA and Peugeot SA. It owns three car brands in its portfolio: Peugeot, Citroën and DS. Moreover, it offers a wide array of mobility services under its Free2Move brand, a product line aimed to meet the growing needs of automobile users. With 3.15 million sold vehicles in 2016 PSA is one of the major players in the industry.

Under the current CEO, Carlos Tavares, PSA has undergone a great strategic overhaul which led to a significant turnaround for the company after the French government bailout in 2012. Mr. Tavares managed to lead the company from net losses to profits in just 3 years and 2017 will be the first year in which PSA will be paying dividends after 6 years.

In 2016, the Group has increased nominal sales for the third consecutive year (5.8% YoY growth) and to more than 3 million vehicles worldwide. The Group also reported €54.03bn in revenues, relatively flat year on year. The operating income reported was €2.61bn (32% YoY growth) and the net income amounted to €2.15bn (78% YoY growth), which shows an improvement in efficiency compared to past years.

Opel AG

Opel was founded in 1862 in Rüsselsheim, Germany, by Adam Opel. It was purchased by GM in the 1930s and it is now one of Europe’s largest automakers with a 5.73% market share. The company designs, manufactures and distributes passenger vehicles, light commercial vehicles and vehicle components for distribution. Opel offers German engineering expertise available at affordable prices combined with innovative premium-class features.

In 2016, the company sold approximately 1.2 million vehicles, which is an increase of 4% YoY and highest sales volume since 2011. From 2016 to 2020, the brand plans to bring 29 new models to the market, 7 of which are expected to be introduced in 2017.

Vauxhall Motors (GM UK Ltd) is one of the oldest car manufacturers and distribution companies in the UK, which traces its history back to more than 100 years and that has engineered and produced some of the UK’s most popular vehicles. It was acquired in 1925 by GM for $2.5bn and acted as main GM’s UK distributor. The cares offered by Vauxhall have the same platform as the cares offered by Opel and are most of the time just rebranded to ensure the recognition of the established brand Vauxhall. Together with Opel, Vauxhall Motors employs over 38,000 people in Europe and is currently present in over 50 countries around the globe. Together, the two car manufacturing companies generated €17.7bn in revenues in 2016.

In the end, it is of note that the mayor problem of Opel (and Vauxhall) is the lack of profitability in the last 20 years. In summary, they are caused by one of the most expensive locations for production costs (Germany and UK) and functional overlaps with the administration of GM.

Industry Overview

The global auto industry is more challenged than it can be expected, although performance seems to be strong on the surface. Worldwide sales reached a record 88 million autos in 2016, up 4.8% from the previous year and profit margins for suppliers and auto makers (also known as original equipment manufacturers, or OEMs) are at a 10-year high. Nonetheless, viewed through the lens of two critical performance indicators, the industry seems to be in serious troubles.

First, the average automaker TSR (Total shareholder return) was about 5.5% whereas the S&P500 and the Dow Jones in the same period guaranteed returns of 14.8% and 10.1%, respectively. Second, in 2016 the returns of the top OEMs were about half the industry cost of capital and major suppliers have enjoyed slightly positive returns after years in the red. These numbers paint a picture of an industry that is a less attractive place to invest than other sectors.

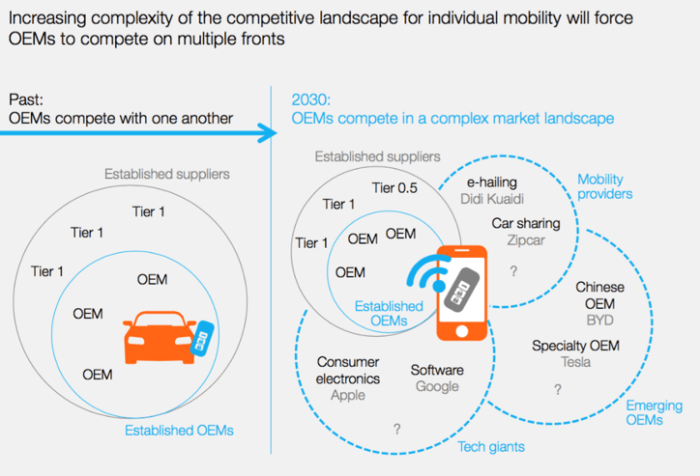

Besides, the situation is becoming direr as the cost of capital is unlikely to come down and new capital outlays are rising for advances in connected cars and autonomous driving technology. Innovative software developments may make tomorrow’s vehicles exceptionally expensive: OEMs and suppliers must earmark resources for acquiring modern technology and recruiting experienced technical talent. It is forecasted that in the next 2 years the vehicle electronics will account for about 20% of the car value, up from only 13%. As a result, some of the recent mergers and acquisitions in the automobile sector were undertaken to augment GM’s in-house technical knowledge and capabilities. Decisions about investments and industry alliances that are being made now will determine the dominant positions of tomorrow.

The rising cost of safety and environmental regulations is also a concern for the industry. Apart from the US and Europe where strict standards have already been implemented, other parts of the world, including China, are catching up to the regulations of the developed countries.

From a macroeconomic perspective, there is no market promising a substantive growth in the short to medium run: the US market seems to have reached last year his sales record and is expected to keep sales flat. Sales have improved in the European Union since the financial downturn, but the European auto industry is held hostage by local economies that are teetering on the edge of recession. Moreover, emerging countries, on which the world counted for future growth, are underperforming. In the end, given this global picture it seems that expansion in specific areas doesn’t provide a solution to the crisis of the industry.

Structure of the Deal

The deal is divided in two transactions: first, PSA Group acquires Opel and its sister brand Vauxhall, effectively cutting GM’s marque in Europe. Secondly, PSA Group and the French bank BNP Paribas jointly acquire GM Financials’ functions in Europe.

Under the agreement, the acquisition of Opel/Vauxhall involves a consideration consisting of €670m paid in cash and €650m in PSA share warrants, for a total contract value of €1.3bn. In anticipation of proactive integration of the Opel brand following the acquisition, the warrants have a maturity of nine years and are exercisable after five years with a strike of €1. As of the announcement, PSA referenced the shares at €17.4, pricing the option warrants at €7.16, corresponding to 39.7m PSA shares (4.2% of diluted share capital). Furthermore, GM has agreed to sell the PSA shares obtained on the warrant exercise within 35 days, and will not enjoy governance or voting rights throughout the holding period.

Secondarily, PSA and BNP Paribas will pay €900m for GM Financials’ operations in Europe, booking GM a projected loss between $4 and 5bn from the deal. The value of the combined transactions amounts to €2.2bn. Of these €2.2bn, PSA will cover €1.8bn, the rest by BNP Paribas

The deal is expected to close before the end of 2017, subjected to a plethora of conditions, including regulatory approval and reorganizational plans. The transaction includes all of Opel/Vauxhall’s automotive operations, comprising Opel and Vauxhall brands, six assembly and five component-manufacturing facilities, one engineering center (Rüsselsheim) and approximately 40,000 employees. GM will retain the engineering center in Torino, Italy. Opel/Vauxhall will also continue to benefit from intellectual property licenses from GM until its vehicles progressively convert to PSA platforms over the coming years.

Drivers of the Deal

In an industry characterized by thinning margins and threatened by regulatory complexities and advancements in technology, becoming bigger is one of the keys for survival. The acquisition would allow PSA Group to surpass Renault and become the second largest player in Europe in the automotive industry with an estimated market share of 17%. Moreover, it is expected that the group would be able to increase its sales in other key regions such as Asia, where consumers seem to trust more German manufacturers such as Opel.

According to the representatives of the both sides, the combination would create realizable annual synergies of €1.7bn by 2026. A significant amount of synergies is expected to be delivered in the first 3 years post the closing date of the transaction. The savings are to be achieved through spreading the enormous costs for R&D, manufacturing and a stronger bargaining power with the suppliers. PSA Group’s CEO, Mr. Carlos Tavares has guided his company through a successful recovery in the last 2 years, after the company has been consistently ending their fiscal years in negative territory. After the acquisition, it is expected that Opel would undergo through a turnaround and achieve a positive operational free cash flow by 2020 and to steadily increase its operating margin, reaching 6% by 2026.

The rationale of GM to divest the brands of Opel/Vauxhall is to decrease their exposure in the “old continent”, and to focus on their core market, the US, where they have consistently achieved better results than in Europe. The proceeds from the transaction, would allow GM to work on more lucrative opportunities in their core automotive business and to invest in new disruptive technologies. Additionally, the proceeds would allow the American giant to speed up its buyback program of $14bn.

Sources and References:

Company presentations, Bloomberg, Reuters, The Wall Street Journal, Financial Times, CNBC pressroom, Companies’ websites and New York Times.

To contact the authors:

Niels Carl niels.carl@studbocconi.it

Joerg Heilmair joerg.heilmair@studbocconi.it

Davide Martellozzo davide.martellozzo@studbocconi.it

Giorgio Passerini giorgio.passerini@studbocconi.it

Dima Pisaniuc dimitru.pisaniuc@studbocconi.it

To contact the editor responsible for this story:

Davide Magni davide.magni@studbocconi.it

You must be logged in to post a comment.