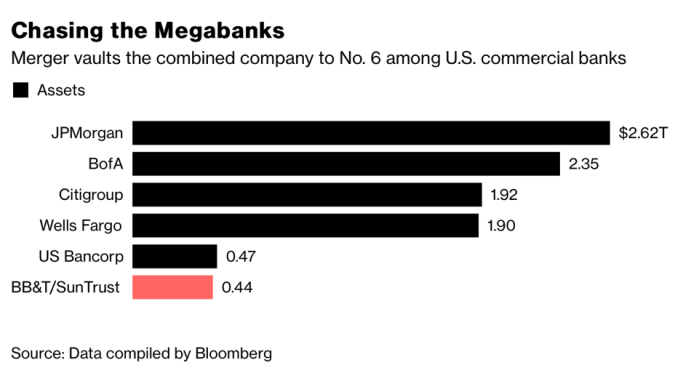

On February 7th, 2019 BB&T Corp. announced a deal to buy Suntrust Banks Inc. for $28.2bn, creating the sixth-largest US commercial bank. This is the largest US bank merger since the great consolidation of the 2008 financial crisis and it may pave the way to a new merger wave in the US Banking sector.

Companies Overview

BB&T

BB&T Corporation (NYSE: BBT, $48.53 stock price, $37.04bn market cap as of February 6th, 2019) is one of the largest US financial services companies with $225.7bn in assets as of December 2018.

Founded in 1872 in Wilson county, Eastern North Carolina, under name Branch and Hadley (after the two founders), BB&T grew to the status of North Carolina’s “big bank” during WWI. After surviving the Great Depression and enjoying unprecedented growth through the 60s, 70s and 80s in North and South Carolina, BB&T started to grow rapidly outside of its stronghold through consolidation during the 90s and the first decade of the 21st century. In 2019, BB&T operates more than 1,800 financial centers in 15 states (mainly east coast and Texas) and Washington D.C. and employs more than 36,000 people across the USA.

In 2017 the company had:

- Revenues: $11.3bn (4.8% increase YoY; a 19% increase since 2012)

- Net income: $2.41bn (1.1% decrease YoY; a 19.1% increase since 2012)

- Total deposits: $164.63bn (increased by 20% since 2012)

- Loans and leases: $144bn

- Profit margin: 29.41%

- Book value per common share: $34.01

- ROE: 8.25%

- CET 1: 10.2%

SunTrust Banks

SunTrust Banks, Inc. (NYSE: STI, $58.74 stock price, $26.25bn market cap as of February 6th ,2019) with 1,268 full-service branches, $206bn of total assets and 24,324 employees, is one of the largest and strongest financial service company of the southeastern states of the USA.

Founded in 1891 in Atlanta, where the current headquarters of the company are, under the name Georgia General Assembly, the company developed and consolidated in the southeast through a series of merger and acquisition deals in the 80s, 90s and the beginning of the 21st century, the last of which is the merge with Memphis-based National Commerce Financial Corporation.

The business of the bank is organized in 2 segments: Consumer (Consumer Banking, Consumer Lending, Private Wealth Management and Mortgage) and Wholesale (CIB, Commercial and Business Banking, Commercial Real Estate, and Treasury) which respectively accounted for 38% and 62% of the 2017 $2.3bn net income.

In 2017 the company had:

- Revenues: $9.1bn (4.1% increase YoY; a 13% decrease since 2012)

- Net income: $2.28bn (21% increase YoY; a 15% increase since 2012)

- Total deposits: $166.5bn (increased by 21% since 2012)

- Loans and leases: $143bn

- Profit Margin: 30.77%

- Book value per common share: $47.94

- ROE: 9.72%

- CET1: 9.74%

For comparison, in 2017 the 4 largest commercial banks in the US had:

- Revenues: (JPMorgan $100bn ; BofA $87bn ; Citi $73bn ; WF $89bn )

- Net income: (JPMorgan $24.5bn ; BofA $18.3bn; Citi $15.8bn ; WF $22.4bn )

- Total deposits: (JPMorgan $1,707bn ; BofA $1,595bn ; Citi $1,208bn ; WF $1,408bn )

- Loans and leases: (JPMorgan $931bn ; BofA $937bn ; Citi $675bn ; WF $968bn )

- Profit Margin:(JPMorgan 36% ; BofA 33% ; Citi 31%; WF 31% )

- Book value per share: (JPMorgan $67.04; BofA $23.80; Citi $70.62 ; WF $35.18 )

- ROE: (JPMorgan 10%; BofA 9.5%; Citi 7% ; WF 11.5% )

- CET 1: (JPMorgan 12.1% ; BofA 13.1% ; Citi 12.4%; WF 11.13% )

Industry overview

The US banking industry appears to be enjoying favorable economic and political conditions recently.

With the election of President Trump, the expectations of low regulatory pressures have been not only preserved but also arguably bolstered.

On the other hand, the prevailing low economic growth rates for more than 10 years already have been one of the major concerns for US banks as organic growth has become harder to achieve. The most powerful tool that big US banks have currently is their ability to scale through digitalization. To compete in the digital arena, banks have to significantly adjust some of their pre-existing business practices and employ new ones. This means shifting the focus from branch expansion to developing and marketing digital solutions for their customers by increased investments in R&D and substantial expansion of the technology divisions. At this point, the five largest US banks have more that 40% of the market share of US deposits, which is double the share they had 20 years ago. A good part of the expansion in dominance can be explained by the realized economies of scale through digitalization, which smaller or medium banks have not benefited from due to high barriers, such as capital, vast amounts of data and human talent.

Nevertheless, digitalization is the characterizing aspect of many fintech companies which are currently entering the financial services industry and are hoping to gain competitive advantage by being fully digital and thus more cost efficient. Even though there are new firms entering the market each day, most of them either have a very insignificant market share or end up being acquired by the major US banks. In 2018, the top 10 US banks have participated in a record number of more than 10 acquisitions of fintech companies.

Along with digitalization, the new CECL accounting standard which will be adopted in 2020 is another major threat for the industry and especially smaller banks. Under the new standard, banks will be required to build their allowance for loan losses on the date of formation of the loan, while currently losses are recorded when it becomes probable that the loan will be impaired. According to S&P Global Market Intelligence’s scenario, the level of reserves required under CECL from 2020 on will increase by 50%. Even though most banks currently have ample capital to successfully adopt the new accounting standards, some banks with thinner capital rations, especially smaller ones, will need to either raise more capital, increase rates, introduce more stringent loan requirements or consolidate with other banks.

In the current landscape of digitalization and the upcoming CECL standards, consolidation appears to be one of the few viable options for smaller and medium US banks.

Deal Rationale

The deal, worth $66 billion, represents the largest merger in the banking industry since the financial crisis and aims at creating the sixth largest bank for assets and deposits in the US. The upcoming institution will have $442 billion in assets, $301 billion in loans and $324 billion in deposits with 10 million of US households as customers.

The main reason behind this operation is the need, for both the institutions, to increase their scale as “it is clear that the combined company can do more than we can alone” SunTrust Chairman and CEO William Rogers Jr said. The upcoming scale will enable the new entity to invest in technology and innovation as “We’re finding the consumer is demanding real-time satisfaction, they want what they want, where they want it, exactly when they want it” BB&T CEO and Chairman Kelly King told The Atlanta Journal-Constitution.

The increasing number of ATM and branches will benefit the final customers, both the companies sustain. However, about 25% of the two banks branches are within two miles each other and this could lead to branch closures in the future. This strategy follows the branch consolidation plan already implemented by BB&T, which has seen a 7% reduction of its total branches both in 2017 and 2018.

The potential cost synergies are expected to deliver approximately $1.6 billion in annual net cost savings by 2022 (around 10% of total expenses), Suntrust reported. The primary sources of cost savings are expected to be in facilities, information technology/systems, shared services, retail banking and third-party vendors.

The new company will also create an Innovation and Technology Center, putting emphasis on the new digital strategy of the bank.

Despite operating in the same geographical area, the two businesses are considered as complementary. BB&T’s Community Banking will guarantee revenues from its insurance operations while SunTrust’s mid-market CIB business and digital lending platform will enhance the core business of the new entity.

Overall, the new group would be able to challenge the market leaders which in the recent past have invested larger resources in technology and innovation.

Deal Structure

The all-stock deal will allow BB&T to buy SunTrust Bank at a price of $28 billion, in what is usually described as a “merger of equals”. SunTrust shareholders will exchange their shares with BB&T’s ones at 1:1.295 rate, with a 7% premium to SunTrust shares. BB&T shareholders will hold the 57% of the new entity, while SunTrust the 43%.

Markets reacted to the announcement positively: SunTrust shares rose up to 10% ($64.60) while BB&T up to 5% ($51.20).

The two banks expect the new company having 60,000 employees, $440 billion in assets and a 22% RoATCE (Return on Average Tangible Common Equity), higher than the majority of the large banks in US.

The transaction is planned to be closed by the end of 2019, with Kelly King (current BB&T CEO) as the CEO of the new group until September 2021, after which W. Rogers Junior (current SunTrust CEO) will take place.

The name of the new company has not been disclosed yet, but the new headquarter will be based in Charlotte (NC).

BB&T chose RBC as advisor, while SunTrust has been advised by Goldman Sachs. The transaction is subject to regulatory approval and to the approval of the shareholders of the two banks.

Sources and References: Bloomberg, Companies’ websites, Financial Times, Reuters, Wall Street Journal, CNBC, AT Kearney, McKinsey, S&P Global

To contact the authors:

Davide Martellozzo davide.martelozzo@studbocconi.it

Francesco Di Carlo francesco.dicarlo@studbocconi.it

Abel Poghosyan abel.poghosyan@studbocconi.it

You must be logged in to post a comment.