On February 6th, Spotify acquired Gimlet and Anchor, two key players in the Podcast Industry, establishing the beginning of a process of expansion and diversification to ultimately create the largest distributor of audio products, not only music, as Daniel Ek, CEO and Founder stated.

This article aims at analyzing the two recent and biggest strategic acquisitions of Spotify. It analyzes the companies involved in the deals and the Music and Podcast Industries to better understand the ultimate reasons of the move.

Spotify

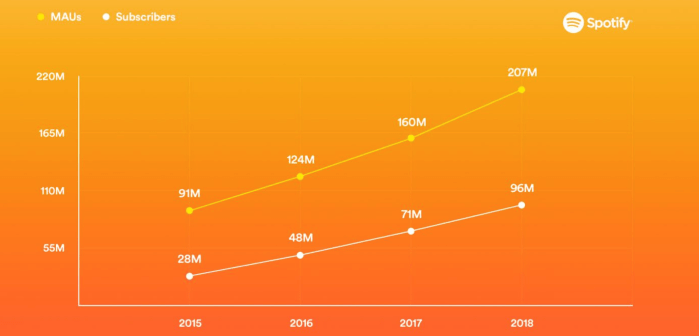

Spotify Technology S.A. (NYSE: SPOT, $148.52 stock price, $26.861 bn market cap as of February 15th, 2019), launched in Sweden in 2008, is a well-known platform for music streaming service with a community of 207 million users, among whom, 96 million are counted as subscribers.

The platform benefits from a library of over 40 million songs and besides offering subscription packages through its Spotify Premium, which gives access to offline mode, higher sound quality, ad-free listening and its Spotify Connect service, it also allows users to interact for free with some limitations rotating around the already mentioned advantages a normal subscriber would get.The company has been the largest driver of revenues to the music business, generating €10 bn of royalties paid to music publishers.

As of Q4 2018, Spotify counts its presence in 78 markets around the world and has seen a constant growth in number of users and subscribers (as Graph 1 shows), with 9 million added from Q3 and a 30% increase in revenues year-on-year, going to €1.5 bn (meeting projections), these ones generated from subscriptions and ads.

The company has announced future sacrifices of margins in a trade-off for growth as it is preparing itself to invest from $400 M to $500 M in strategic acquisitions for 2019. For this reason, gross margins are expected to decrease to 22-25% from 26.7% in 2018.

Graph 1: Time series of Subscribers and Monthly Active Users

Gimlet and Anchor

Gimlet Media, founded in 2014 by two former radio journalists, is one of the largest podcast producers, next to ESPN Radio, Audioboom, Authentic, benefitting from a wide network of high-quality, narrative podcasts, with hit shows such as “Homecoming” and “Reply All”, the former being licensed to Amazon to create a TV series.

As of 2019, Gimlet counts important shareholders obtained through 6 funding rounds, raising a total of $28.5 M. The biggest ones are WPP, Graham Holdings and Stripes Group, which have respectively invested $5M, $6M and $15M.

Anchor FM Inc develops specific software tools that enable anyone to record or upload high-quality audio, host and distribute content. It has grown into the most popular tool developer among many podcast creators.

As of 2019, it has raised $14.4M in 4 funding rounds with GV investing $10M, Accel investing $2.8M and Eniac Ventures and SV Angel investing $1.6M.

Music Industry

After two decades of systematic disruption, starting with the destructive impact on overall profitability due to the piracy problem, the Music Industry is experiencing an outstanding revival thanks to the increasing popularity of streaming platforms such as Spotify, Apple Music, Deezer, Amazon Prime Music and Pandora. According to Goldman Sachs, revenues will double by 2030 to $131 bn.

Revenues are distributed among three different categories:

-

- Live Music Revenues, with $26bn as of 2017

- Recorded Music Revenues, with $30bn as of 2017

- Publishing Music Revenues, with $6bn as of 2017

The distribution is set to change by 2030 with a huge surge in revenues coming from Recorded music and a 108% increase in revenues coming from Publishing music.

Music is inevitably linked to the spread in popularity of Streaming services. In addition, more and more Millennials and members of the Generation Z are increasing their spending in this kind of service which is also boosted by the increase in the use of smartphones in both Developed Markets and Emerging Markets.

This is inevitably good news for Spotify and its growth targets, even though it does not solve one of the main problems of the company: its operating costs (pointed as “Cost of Revenue”) that are presented in the form of royalties paid to big music labels and music publishers represent a significant portion of its operating revenues, determining lower gross and operating margins (as shown in Exhibit 1).

This is one of the main reasons why Spotify is betting big on Podcasting, as the industry may offer new opportunities to escape from the sticky costs of the company.

Exhibit 1: Portion of the Annual Income Statement of Spotify Technology S.A.

Podcast Industry

According to a recent joint research of IAB and PwC Research, the Podcast Industry has reached $314 M of revenues in 2017, representing an 86% growth Y-o-Y and is expected to double to $659 M by 2020, which has been described as outstanding for a niche industry based on a medium that is quite difficult to monetize.

Among the different companies surveyed and data collected, top podcast producers recorded a 94% revenue growth from Q4 2016 to Q4 2017 with a 18% compound quarterly growth rate.

More than half of those revenues has been generated by ads put on Podcasts focused on Arts and Entertainment, Technology, News and Politics and Business, becoming the biggest fields and establishing a tangible possibility to become strong platforms for advertisement, even though the results are absolutely small if compared to the tens of billions of dollars spent by advertisers on video content.

Deal Rationale

The acquisitions of Spotify clearly show the company’s intentions to dig deeper inside Podcast territory.

Despite its late entrance, as podcasts started appearing since 2000, with Apple being an important contributor to the overall growth with its iTunes 4.9, Spotify aims at taking part and benefiting from a long-term and still developing strategy of monetization of podcasts through subscriptions, ads and possible licenses of shows, just like Gimlet is doing with ABC and Amazon.

The new move would ultimately engage users in new ways, by bringing radio experience to the platform, as people spend on average two hours a day listening to radio.

It would also create a new channel to enhance consumption of core business and overall time spent on the platform.

It goes without saying that the diversification process that Spotify is starting has also a financial purpose as the company is trying to find new ways to generate additional revenues that could be considered free from the sticky royalties paid to music publishers, to ultimately increase its operating margins.

Deal Structure

Despite the uncertain numbers published by different sources, Spotify is expected to buy Gimlet and Anchor for, respectively, $230 M and $140 M, paying in cash, investing a relatively important amount and even similar to the amount of revenues generated by the industry in 2017.

The announcement of the acquisitions came as Spotify reported fourth-quarter results. Shares fell 5% in pre-market trading as investors negatively reacted to the company’s forecast of lower future margins due to the planned investments in acquisitions aiming at growth in the long-term.

Investors are also asking themselves whether the investment will generate an adequate future return as Spotify enters a relatively small field if compared in ads revenues generated by other kinds of medium.

Sources and References: TechCrunch, Financial Times, CrunchBase, Goldman Sachs, IAB, PwC Research, Spotify, Bloomberg, Barron’s

To contact the authors:

Denis Cascino denis.cascino@studbocconi.it

Theodore Tassin de Charsonville tdecharsonville@hotmail.com

You must be logged in to post a comment.