On February 11th, 2019 Morgan Stanley acquired Solium Capital, a large equity plan administrator, for $900m, a 40% premium over the recent trading price. This is the biggest acquisition in a decade for the Wall Street giant and likely the first of many more deals to enlarge its wealth management business in the next decade.

Companies Overview

Solium Capital

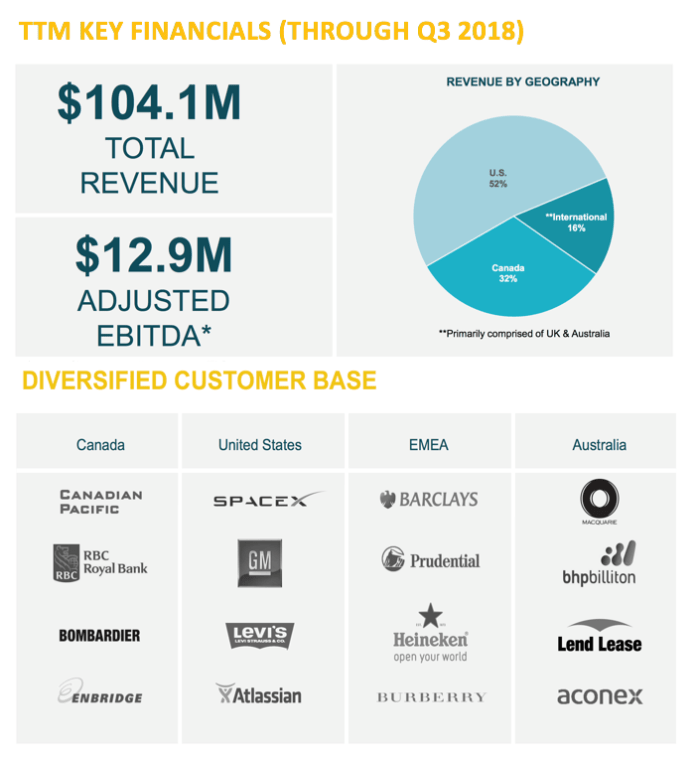

Solium Capital (TSX:SUM, CAD 13.36 stock price, CAD 758 mn as of February 8th) with revenues of $104.2mn TTM and clients in more than 100 countries, is a Canadian SaaS company global leader in equity plan management.

Founded in 1999 in Calgary (AL), where is currently headquartered, the company is well renowned for Shareworks, its single global SaaS platform which, transacting on 15 global exchanges in real time, enables public and private firms to manage stock option plans and cap tables (spreadsheet or table that shows capitalization, or ownership stakes, in a company).

The firm supports money transfers for billions of dollars ($8.5bn money movement in 2017) through a 24/7 call center and 4 global operating centers (Calgary, Tempe, London, Sydney).

The company uses different channels to sell its cloud-enabled services:

- a direct sales force

- white label partners

- third party partners (law firms, wealth managers, and others)

Over the course of the past few years Solium expanded both organically and through acquisitions such as:

- GlobalSharePlans, a leading online provider of regulatory and tax advice for companies with global equity incentive plans, in December 2013

- Capshare, a high-growth cloud platform for cap table management, in October 2017

- Advanced-HR, leading provider of compensation data and compensation planning software for private and venture backed companies, in February 2018

According to the company 2018 investor presentation:

- 66% of revenues come from fixed-recurring subscription, 30% from participant and plan based based–reoccurring activity (brokerage, transaction & fund movement fees; foreign exchange spread), and 4% from implementation fees and special projects

- the biggest market for the company is the US (52% of revenues), followed by Canada (32%) and the rest of the world (primarily UK & AUS) (16%)

- the company’s management is determined to expand in the UK and Europe (primarily Germany), continue building brand awareness in Australia and Canada, and establish significant partnerships with Wealth Management firms

Morgan Stanley

Morgan Stanley (NYSE:MS, $40.815 stock price, $70.2bn market cap as of February 8th), with revenues of $40.1bn (2018, a 6% increase YoY), pre-tax profits of $11.2bn (2018), a $8.7bn net income (2018), and 57,000 employees in more than 41 countries, it is one of the most important global investment banks in the world and a Fortune 500 company.

It was founded in New York, where its world headquarters are at 1585 Broadway Av., in 1935 as a result of the 1932 Glass-Steagall Act (the two founders left J.P. Morgan & Co when it closed down the IB business).

The business is divided into three main segments:

- Institutional Securities: made up by the IB and the S&T divisions and produced revenues for $20.6bn and a pre-tax income of $6.3bn (a staggering 12.5% increase YoY) in 2018

- Wealth Management: produced revenues for $17.2bn, which are divided into Transactional, Asset management, Net Interest and Others, and a pre-tax income of $4.5bn in 2018

- Investment Management: produced revenues for $2.7bn, which are divided into Investments and Asset management, and a pre-tax income of $464mn in 2018

Since joining Morgan Stanley from Merril Lynch in 2006, James Gorman, the current CEO of the bank, has invested a lot in the Wealth Management division of the Wall Street giant and the investment seems to have paid off well. The bank consistently increased client assets in the WM business since the acquisition of 51% of Smith Barney in 2009 bringing them from $1.6 to $2.3 trillion.

Source: Morgan Stanley Strategic Update 17th January- 2019

Industry Overview

A big driver for M&A in the financial services sector over the last few years has been technology. Indeed, financial institutions have been pursuing acquisitions either to keep pace with innovation, winning market share in attractive market segments such as payments and specialty finance, or to build more scale in order to go through a heavy digitalization process that requires significant investments.

A lot of banks around the world are shifting resources from traditional investment banking and trading activities to their wealth management divisions as we are late in the cycle and the global volume of net investable assets of high-net-worth individuals (HNWI+) is expected to increase by around 25% to almost US$70 trillion by 2021. This extraordinary increase in private wealth is mainly driven by higher returns on asset classes compared to the average GDP growth in the post crisis period.

Source: EY wealth management outlook – 2018

The wealth management industry is faced with challenges such as intense competition, fee compression, stricter regulations, and evolving customer needs.

As technology continues to change rapidly, firms must be agile to enhance the overall experience of their customers. Infrastructure and technology-driven capabilities will be fundamental to a wealth manager’s activity in the future.

On top of that, the industry’s advisory model has also been transforming, increasing focus on the traditionally underserved segments. Among these segments, the mass affluent segment (US$1million-US$5million) comprises 90% of global HNWIs by population and 43.0% of total wealth. Goldman Sachs has been focusing on the mass market through its Ayco business, which provides financial coaching to employees through corporate partnerships. Another example in support of this claim is the move made by Pilatus Bank, which now offers services to the mass-affluent market that were earlier available only to HNWIs.

An additional area of vital importance for wealth managers is represented by the women segment, given that the global wealth of women is expected to grow from US $13 trillion to US $ 21 trillion by 2021, about 1.6% faster year-on-year than that controlled by men, a trend exploited by UBS, which has prioritized attracting more female clients with focused advisory service.

Furthermore, personalized solutions catering to niche segments can be a client acquisition tool to attract younger, less-affluent customers, who might potentially require private banking services in the future. Increasing competition and client demand for transparency is forcing firms to relook at their strategies to acquire and retain clients. For instance, looking for different distribution channels in order to create cross selling opportunities has been a very successful move for Etrade, which converted equity plan clients into brokerage clients.

Deal Rationale

The deal has several key drivers, ranging from business synergies in Solium’s core business, i.e. stock plan management, to gaining access to new technology, from expanding Morgan Stanley’s wealth management division to catch cross-selling opportunities in other bank’s businesses.

First of all, the operation is aimed to create a global market leader in equity administration, offering a complete set of solution encompassing equity plans and stock management for corporates around the world. Morgan Stanley, that entered into a partnership with Solium in 2016 to administer equity-compensation plans for its corporate clients and employees, already operates in the stock-plan business, with more than 330 corporate clients (including Microsoft and Ford Motor) and covers 1.5 million employees. However, its business merely focused on top executives stock plans for Fortune 500 companies. The combination with Solium Capital will broaden the equity management business horizon, since the Canadian company will add over 3000 corporate clients with 1 million employees, including start-ups as the fintech payment firm Stripe Inc., the e-commerce group Shopify, the delivery service Instacart Inc., whose workers belong to a very young demographic and usually do not have strong and frequent relationships with banks.

Secondly, the deal will give Morgan Stanley access to technology that Solium has developed through years. Merging with technology firms has become quite popular for banks in the past few years, as financial firms are trying to keep pace with digital transformation and technological progress. Goldman Sachs, for example, snapped up the fintech start-up Clarity Money last year, while JP Morgan acquired WePay in 2017, a leading integrated payment provider.

Source: Forbes

The fact that Morgan Stanley will gain access to Solium Capital’s millennial employees represent an opportunity for client acquisition in the Wealth Management arm as well, since these young clients may become millionaires overnight as soon as their companies go public or may accumulate wealth over time in a more steady and predictable way. In both cases, Morgan Stanley will be able to offer these young customers robo-advisory services until their wealth and fortunes are considered high enough to deserve a transition to human advisory service. As a matter of fact, both passive and active asset management services constitute the backbone of what has become the world’s third largest wealth manager in terms of asset under management.

Focusing on the young age population, especially as regards wealth management activities, becomes a crucial factor since, as a CB Insights Research states, by 2030 millennials are expected to control as much as 20 trillion dollars of assets globally and their parents are expected to pass down another 30 billion dollars by 2050 in North America alone.

If the first target is enhancing the wealth management division, cross-selling opportunities cannot be ignored. Indeed, Solium clients include successful start-ups that Morgan Stanley’s investment bankers can strategically advise and take public, since relationships built by the wealth management division might turn into IPO mandates for Morgan Stanley’s investment bank division. Winning public offering mandates is a crucial point for Morgan Stanley, that in that field is competing with rival Goldman Sachs as some of the largest privately held tech companies are ready to go public. Moreover, the Sales and Trading department may benefit as well, since when customers-employees want to sell their shares, they will do so turning to Morgan Stanley’s trading desks.

Finally, it cannot be excluded that this is the first of many future deals aimed at adding scale to Morgan Stanley asset and wealth management division and at developing the retail banking business fundamental to gain customer loyalty and where, at the moment, Morgan Stanley is lacking.

Deal Structure

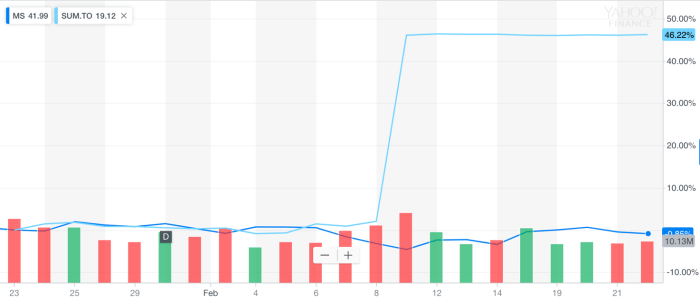

Morgan Stanley will acquire all of the issued and outstanding common shares of Solium for CAD 19.5 per share in cash, representing a 43% premium over the previous closing price, CAD 13.36, and a total valuation for the Canadian stock plan administrator of CAD 1.1bn ($0.9bn). The transaction is subject to the approval of Solium shareholders and regulatory approval.

On the day of the announcement of the deal, the stock price of Solium soared by 46% matching the offering price while Morgan Stanley’s stock declined by 4.6% and later recovered during the week.

The transaction is expected to close in the second quarter of 2019.

CIBC World Markets Inc. is the financial advisor to the Solium’s Special Committee in charge of reviewing, evaluating and negotiating the Arrangement on behalf of the company. Norton Rose Fulbright is acting as Solium’s legal advisor.

Davis Polk & Wardwell and Osler, Hoskin & Harcourt are providing legal advice to Morgan Stanley in connection with the transaction.

Sources and References: Wall Street Journal, Financial Times, Bloomberg, CBinsights, Solium investor relations, Morgan Stanley press releases, Capgemini, Forbes, Deloitte WM outlook 2018, EY WM outlook 2018

To contact the authors:

Davide Martellozzo davide.martellozzo@studbocconi.it

Luca Ranzani luca.ranzani@studbocconi.it

Simone Bertani simone.bertani@studbocconi.it

You must be logged in to post a comment.