Introduction:

The $90bn merger between United Technologies Corp. and Raytheon Co. constitutes the largest ever merger in the Aerospace and Defense sector, resulting in a creation of among the largest company of its industry. The merger has resulted in a very diversified group, operating in both the commercial aerospace and the Defense industry. Due to the diversification, the deal was heavily criticized. On the other hand, the combined group will use the core competencies of Raytheon and United Technologies to develop new solutions consistent with the most recent technology trends in the sector.

Companies overview:

Raytheon Company

Raytheon Company was a major U.S. defense contractor with core manufacturing concentrations in weapons, military and commercial electronics. It supplied mainly the U.S. government with military and missile equipment. Founded in 1922 and headquartered in Waltham, Massachusetts, the company was incorporated in the state of Delaware and adopted its name in 1959. In March 2014, Thomas Kennedy was named CEO succeeding William Swanson.

The company operated in five business segments: Integrated Defense Systems; Intelligence, Information and Services; Missile Systems; Space and Airborne Systems; and Forcepoint. Its electronics and defense-systems units produce air-, sea-, and land-launched missiles, aircraft radar systems, weapons sights and targeting systems, communication and battle-management systems, and satellite components. Before the merger, Raytheon generated more than $27 billion in net sales and had a market capitalization of $55 billion.

United Technologies Corporation

United Technologies Corporation (UTC) was an American multinational conglomerate. It provided high technology products and services to the building systems and aerospace industries worldwide. Headquartered in Farmington, Connecticut, UTC is divided into four segments which are still operating:

- Otis manufactures a wide range of passenger and freight elevators, as well as escalators and moving walkways.

- Carrier is a leading global provider of heating, ventilating, air conditioning, refrigeration and security solutions.

- Pratt & Whitney develops large engines for wide- and narrow-body and large regional aircraft in the commercial market and for transport aircraft in the military market.

- Collins Aerospace Systems provides advanced aerospace products, including customers of Boeing and Airbus.

Before the merger, UTC had a market cap of $11 billion and generated $44.7 billion in sales.

Industry overview:

In the Aerospace and Defense industry (A&D) the two major manufacturing areas are civil aerospace and military equipment. A minor part of the production comes from space and security systems. Civil aerospace accounts for the majority of the manufacturing in A&D. In 2019, it experienced a decline in deliveries due to some problems related to the production of certain aircraft models. Nevertheless, the long-term demand is strong, and the commercial aerospace sector is expected to grow over the next two decades.

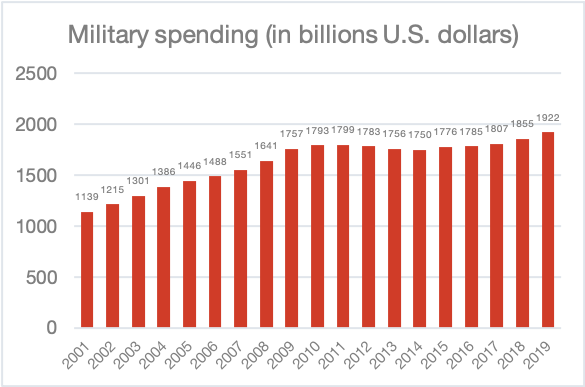

Concerning the defense sector, since the beginning of the Trump administration, defense budgets in the US have been increasing. Similarly, NATO countries, as well as other nations including India, China and Japan, have been growing their defense spending in order to counter potential security threats. Growth in the defense sector has been, in the last years, strongly driven by the demand for military equipment in response to the intensification of geopolitical tensions. Increasing global defense spending will continue to create opportunities for defense contractors and their supply chains.

The defense industry has always relied on the most advanced technologies. Until now, the defense industry has been able to develop these technologies internally. However, the future defense sector will be characterized more and more by a system architecture approach, which takes advantage of new emerging technologies such as 5G, artificial intelligence, quantum computing, biotechnology, human augmentation and novel materials. Although the defense industry will not be at the forefront of developments in these technologies, it is indispensable to adapt and translate them into military systems that meet the requirements of armed forces. Nowadays, we see that these investments in emerging technologies are mainly driven by innovation clusters and tech start-ups. For instance, the US Department of Defense (DoD) has launched the Defense Innovation Unit (DIU), which supports the development of, among others, autonomous systems and biological warfare through investments in tech firms. Therefore, we expect that, over the foreseeable future, competition from nontraditional players will increase. As newcomers gain a share in an industry normally monopolized by major players, R&D efforts will increase. Defense companies will have to adapt their strategies to incorporate these new technologies into the products they develop even if innovation attempts had, in the last years, been lagging. M&A can be an alternative to internal development as in the case of Raytheon and United technology.

On the other hand, it should still be taken into account that the ability of existing dominant players to deal with complex systems, from nuclear weapons to fight aircraft, would be difficult to match. Therefore, it is unlikely that the control of large military platforms will shift away from traditional defense companies towards tech newcomers.

In the global landscape, changes in trade agreements may also play a crucial role on the future of A&D. In Europe, for instance, Brexit might lead to the disruption in the supply chain of one of the most strategic and politically important industries of the UK, especially through its impact on small- to mid-size suppliers. Furthermore, if not lifted, the steel and aluminum tariffs introduced during President Trump’s mandate will continue to raise costs throughout the industry.

In this environment of significant uncertainty, there has been a growing focus of A&D companies on the management of relationships across the supply chain, as well as on the objective of pursuing stable partnerships in the industrial sector. Since 2015, M&A activity has remained strong and is expected to expand further improve, especially in the sub-sectors of Command, Control, Commercial Aerospace and Hypersonics, to name a few. The increasing pressure on suppliers to cut costs and expand production to achieve greater scale effectiveness has driven consolidation. In particular, greater consolidation is expected both among smaller companies, as they face challenges to meet financial and investment requirements, as well by parts families, such as components and electronics, in the search of economies of scale. On one hand, deal volume is supported by megadeals aimed at the vertical integration of the industry’s largest companies, on the other hand, prime contractors are looking to acquire new technologies and expand to new markets through the purchase of small- and mid-sized companies.

Despite the successful outlook of previous years, COVID-19 has caused a drop in M&A activity. In H1 2020, total deal value has been 34% lower than the ten-year average figures in the industry and, even more strikingly, there was a drop of 78% since H1 2019, when total value was driven primarily by the UTC/Raytheon transaction.

Besides the M&A trends, as the COVID-19 pandemic continues to spread globally, the supply and demand dynamics of most A&D companies continue to be affected. In commercial aviation, companies are being faced with a slowdown in demand and disruption in production, while the delivery of new aircraft is being delayed. Given the capital-intensive nature of aircraft manufacturing, cash flows and liquidity are being challenged. On the defense side, COVID-19 is expected to have a milder impact on the short-term demand, given the early budget timing and the cruciality to national security that characterize these projects.

Deal structure:

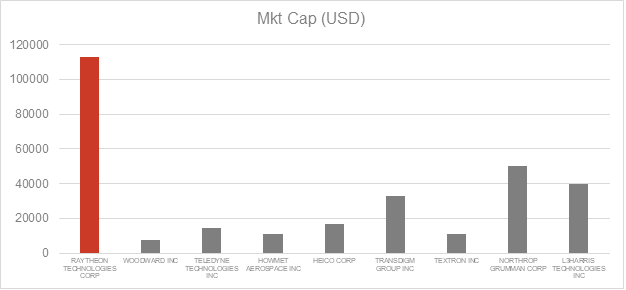

On April 3, 2020, United Technologies Corp. bought Raytheon Co. in an all-stock merger of equals transaction valued at $90bn. The merger created an aerospace and defense conglomerate named Raytheon Technologies Corporation (NYSE: RTX) with a market cap of around $113bn (as of 9th December 2020).

The merger was preceded by the spin-off of two United Technologies Corp. divisions: Otis and carrier which are now listed as a separate entity at NYSE.

United Technologies shareholders continued to hold their shares of United Technologies common stock, which since then constituted shares of common stock of Raytheon Technologies Corporation.

Raytheon Company shares (previous NYSE ticker symbol RTN) ceased trading before the market opening on April 3, 2020. With the merger, each share of Raytheon’s common stock was granted the right to receive 2.3348 shares of United Technologies’ common stock (previous NYSE ticker symbol UTX).

Although the deal is labelled a “merger of equals transaction”, UTC shareholders control 57 percent of the new group, and Raytheon shareholders the remainder. UTC shareholders control 8 of the 15 board seats, and Raytheon’s the rest. The companies state that the newly created entity is expected to return between $18bn to $20bn to shareholders in the first three years after completion of the deal. Moreover, it will assume around $26 billion in net debt over the same period. The deal constitutes the largest ever merger in its sector and the resulting company is among the largest of its industry with approximately $77bn in 2019 pro forma net sales and a global team of 243,200 employees.

United Technologies’ financial advisors were Morgan Stanley, Evercore, and Goldman Sachs while its legal advisor was WLRK. Raytheon’s financial advisor was Citigroup, its legal advisor Shearman & Sterling LLP, and a fairness opinion was provided by RBC Capital Markets LLC.

Deal Rationale:

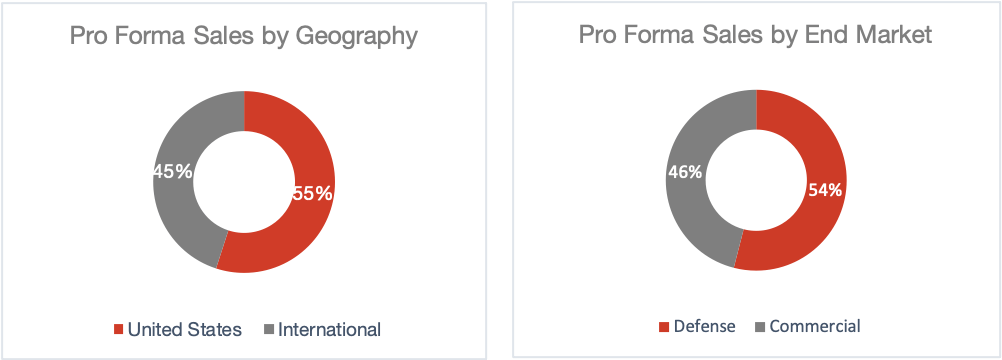

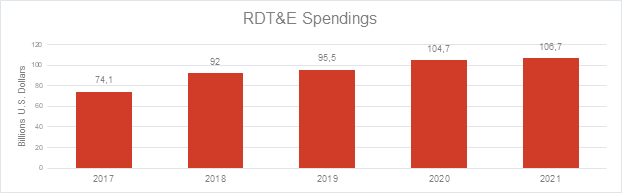

Raytheon and United Technologies did not share many clients and their activities showed few overlaps. The merger has resulted in a very diversified group, operating both in the Aerospace and Defense industries. It also achieved diversification through geographical sales, with 45% of revenues generated in international markets. With diversification, comes reduced dependence on a single platform, program or geographical location making the group more resilient to business cycles. In the past few years, the U.S.’s DoD spending in technologies, budgeted under the caption Research, Development, Test & Evaluation (RDT&E) has been constantly increasing.

The CEOs of both entities expected the investments of the DoD on technology to increase as a result of the strategic confrontation with China and the advancements in new areas like artificial intelligence. The new group with consolidated R&D activities will respond more readily to the new requirements of the DoD, thus translating public spending to additional revenues for Raytheon Technologies. The combined group will use the core competencies of Raytheon and United Technologies to develop new solutions for its military customers. Priority areas are:

- High speed and hypersonic missiles

- Directed energy weapons (These are ranged weapons aiming to damage a target through focused energy such as laser or microwaves. Such technologies are currently considered a priority by the DoD)

- Intelligence, surveillance, target acquisition and reconnaissance (ISTAR), in other words, the acquisition and transmission of battlefield information.

When it comes to commercial activities, 2 of the main clients are Boeing and Airbus. These plane makers are increasingly relying on outsourcing, even in core technology. The competencies combination of Raytheon and United Technologies aims to respond to this opportunity. In that context, the group will focus on the following areas:

- Aircraft connectivity

- Advanced analytics to optimize manufacturing and maintenance of commercial aircraft

Another important activity in the commercial segment is airspace management. United Technologies has been a leader in this activity. The use of Raytheon’s expertise in areas such as radars and military air traffic control aims to help improve customer solutions with improved capacity, efficiency, and safety. In summary, while revenue synergies will not be immediate, they are expected to materialize in the future by the development of new technologies. These technologies are aimed at spurring the growth of existing revenue-generating units and creating new ones.

The cost synergies have been announced to amount to “at least” $1bn per year from Year 4, with half of it creating shareholders’ value while the other half will benefit the US government through cost reduction on contracts. During the merging announcement, the yearly cost synergies have been estimated as follow:

- Supply chain and procurement: $350m

- Corporate and segment consolidation: $325m

- Facilities consolidation: $175m

- IT and other SG&A: $150m

The deal was heavily criticized by 2 high-profile hedge-fund managers, both shareholders of United Technologies prior to the merger announcement.

Dan Loeb, CEO of Third Point, voted against the deal. In a letter to UTC’s board, he declared: “Since there is no strategic or financial rationale for this transaction, we can only conclude that the merger was motivated by empire building and Mr. Hayes’ desire to extend his already long overdue tenure as head of a Fortune 100 company.” About the synergies, he said that “Raytheon brings very little applicable technology to UTC’s aerospace offerings.” The deal was also opposed by Bill Ackman, CEO and founder of Pershing Square Capital Management. In an e-mail to UTC’s CEO, he said: “such a transaction will significantly lower the business quality of pro-forma United Technologies’ aerospace business, and, to make matters worse, will be accomplished through the highly dilutive issuance of large amounts of United Technologies stock.” In hindsight, the COVID-19 pandemic that developed in 2020 was probably less painful for a shareholder of the combined group than it would have been for a shareholder of United Technologies as a standalone company, the commercial aviation sector having been severely impacted.

References: Raytheon Technology’s web site, PWC, Deloitte, Financial Times, Bloomberg, Reuters, Yahoo Finance

To contact the authors:

Yuting Yan

You must be logged in to post a comment.