Introduction:

BBVA has reached an agreement for the sale to PNC Financial Services Group of 100% of the capital stock of its subsidiary BBVA USA Bancshares. The transaction is considered the largest US banking acquisition since the 2008 financial crisis and will allow PNC to become America’s largest regional bank. The deal (approved by both companies’ board of directors) is expected to be closed in mid-2021, subject to regulatory approvals, with a fixed purchase price of $11.6bn (€9.7bn), fully paid in cash.

The deal is expected to bring many advantages to PNC, since the acquisition of BBVA’s 637 unit branches will accelerate their national scale influence, making the bank a coast-to-coast national franchise. This is the target they want to achieve with this deal since PNC’s CEO underlined the importance of spreading their presence in the US to compete effectively with their largest competitors.

Companies’ Overview:

PNC Financial Corp

PNC Financial Corp was created by the merger of Pittsburgh National and Provident National banks in 1983. The deal, which represented the largest bank merger in U.S. history at the time, gave birth to the largest bank in Pennsylvania.

Since its foundation, the Institution pulled off a series of mergers and acquisitions that enabled the bank to amplify the number of services offered and grow across the U.S. until becoming the fifth largest U.S. bank by assets. With the acquisition of BBVA USA, PNC will have a presence in 29 of the nation’s top 30 markets

PNC serves a wide range of customers, that range from individuals and small businesses to corporations and government entities. PNC operates in three main areas:

- Retail Banking

- Asset management

- Corporate & Institutional Banking

PNC is an industry leader in many markets with its client list that includes more than 2/3 of Fortune 500 companies. Additionally, PNC reported a net income of $1,532 bn in 3Q of 2020, an increase of 10% from the third quarter of 2019.

BBVA

Banco Bilbao Vizcaya Argentaria SA (BBVA) was established in Spain in 1988, as a result of the merger between Banco de Bilbao, SA and Banco de Vizcaya, SA. The present name was adopted in 2000, after the merger with Argentaria, Caja Postal y Banco Hipotecario, S.A. With a customer-focused retail business model, BBVA offers clients comprehensive products and services and is engaged in retail banking, asset management, private banking and wholesale banking. As a leading international bank, BBVA is the second-largest financial institution in Spain and the largest in Mexico, with an extensive network in Turkey, South America, Asia, the rest of Europe, and the US.

The firm’s international expansion began in 1902, when the Banco de Bilbao opened a branch in Paris, thus becoming the first Spanish bank with a presence abroad. In 2004, BBVA began expanding into the US, with acquisitions of entities in the south of the country, taking advantage of the strength of its Mexican subsidiary BBVA Bancomer. In 2007, BBVA reorganized its entire portfolio of brands under the name “BBVA Compass” to strengthen its franchise and unifiy its corporate image in the US. As of June 2020, BBVA Compass is the 39th largest bank in the United States by total assets.

BBVA recorded revenues for €23,24 billion and earnings for €3,51 billion in 2019, with an increase of 4,6% and a decline of -35% year on year respectively.

Industry Overview:

Since the 2008 and 2011 financial crises, both European and American banks have been facing deep structural issues with uninspiring revenue growth. However, since the economic consequences of Covid-19 are not as acute as those of the Global Financial Crisis of 2008, the duration of the pandemic will certainly exacerbate the issues. Even before the advent of coronavirus, global GDP growth was slowing down, but the pandemic has aggravated the decline.

With the onset of Covid-19, banks are caught in a devastating limbo of restructuring and staying afloat as the demand for loans skyrockets around the world. The pandemic is realizing a reshaping action to the global banking industry under the aspect of dimensions, introducing in a new landscape, suppressing growth in some traditional product areas, prompting innovation and strongly stimulating digitalization in a great part of banking and capital markets areas.

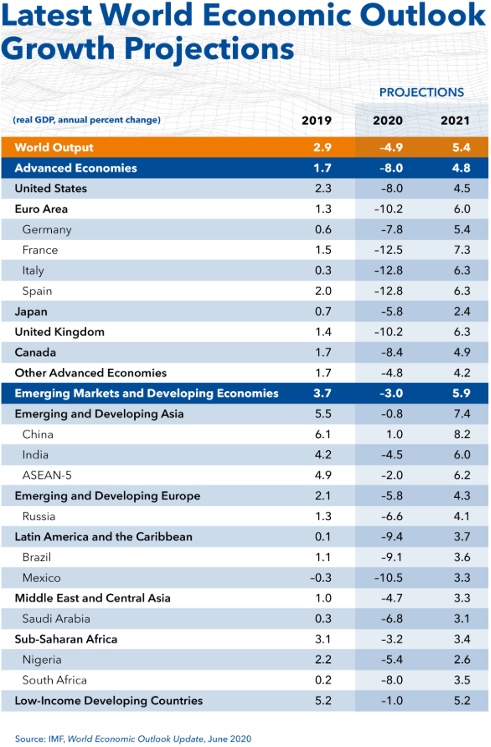

For the banking industry, The International Monetary Fund (IMF) expects global real GDP to decrease by 4.9%, or almost US$6.2 trillion in 2020, with the first half of 2020 incurring a more negative impact than anticipated. Global real GDP growth for 2021 is projected at 5.4%, leaving the global GDP 6.5 percentage points lower than previous projections.

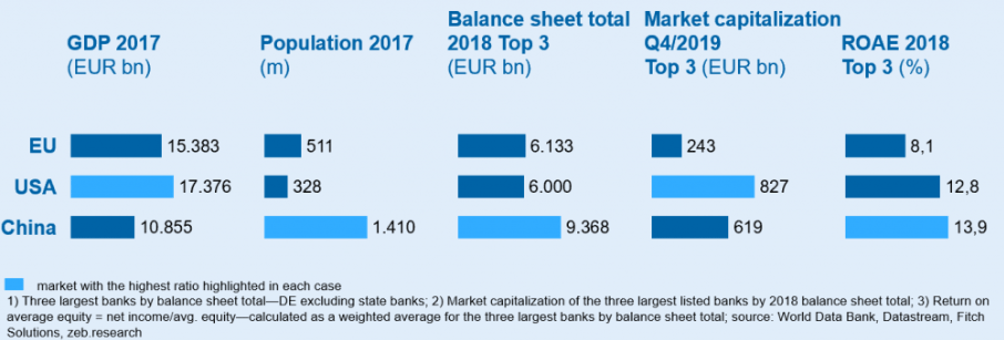

Consolidation processes within Europe have been increasing steadily to survive the fallout of the 2008 Global Financial Crisis and recuperate from its effects. These mergers are backed with positive effects deriving from the economies of scale and diversification in order to survive and return to pre-crisis performances. The number of banks in Europe saw a large reduction from 6,127 to 4,600 in the years between 2007 and 2018. However, European banks did not fully recover before the Covid-19 pandemic struck and were left desperately searching for funds to sustain themselves.

European banks are currently facing the issue of becoming less imperative due to continued weak earnings, outdated IT infrastructures and weaker levels of economies of scale in comparison to their American corporate counterparts. The swift innovations to technology and shifting regulatory environment cause major changes to the way financial institutions conduct business with their customers.

In contrast, the US institutions are characterized by their high profitability and have already undergone their consolidation wave that their European counterparts are trying to fully implement. The US has a highly integrated domestic market and boasts one of the strongest economies in the world exhibiting a high efficiency rate, whereas Europe continues to be fragmented into many countries with economic, linguistic and legal differences (especially between EU and non-EU members). Due to these differences, more European banks are smaller with lower market capitalization and profitability.

PNC’s acquisition of BBVA’s assets in the USA clearly displays the differences and restructuring between European and American banks during the Covid-19 pandemic. BBVA will receive a large equity injection of $11.6 billion required for its survival and to sustain its weak earnings from the failure of their expansion in the USA, while PNC will continue to expand domestically on the acquisition, capitalizing on their increased economies of scale and market share and becoming the 5th largest bank in the US territory.

Deal rationale:

As regards the transaction perimeter here are the 4 main pillars:

- Sale of BBVA USA Bancshares, excluding Propel Venture Partners and BBVA Securities ($0.4bn BV)

- Transaction numbers (related to BBVA USA Bancshares): $102bn Assets, 637 Branches, $587mn 2019FY Results

- BBVA CIB business in the US will continue through the NY branch

- Prior to the closing of the transaction, the excluded businesses will be transferred by BBVA USA Bancshares to entities of the BBVA group

With this acquisition, PNC will accelerate its growth path and drive long-term value creation for shareholders thanks to the strategic deployment of the proceeds from the sale of the holding in BlackRock ($14 billion freed up in May). The takeover will add 21% to PNC’s earnings from 2022, and there will be a significant reduction in costs for the new entity. Moreover, this kind of expansion is vital in an industry dominated by behemoths such as JPMorgan and Bank of America. According to William S. Demchak, PNC’s chairman, president and chief executive officer, this transaction is an opportunity to accelerate PNC’s national expansion strategy and build an experience as a disciplined acquirer.

In the past few years, BBVA suffered from different crises (e.g. a Spanish real-estate bust and an expansion in Turkey) and before the announcement, its stock price reached a low not seen since the mid-1990s. After the PNC deal’s announcement, BBVA shares jumped more than 25%. The sale of the U.S subsidiary will see the bank losing about 10% of its current profits and thus the proceeds will be reinvested to compensate investors for the dilution caused by the transaction. Also thanks to the expected jump from 11.5% to 14.5% of BBVA common equity Tier 1 ratio after the sale. Moreover, after exiting the U.S., much of BBVA’s business will be in emerging markets. For the next future, besides the expansion in other complementary markets, the acquisition of a domestic Spanish rival such as Banco de Sabadell SA might also be possible.

Deal structure:

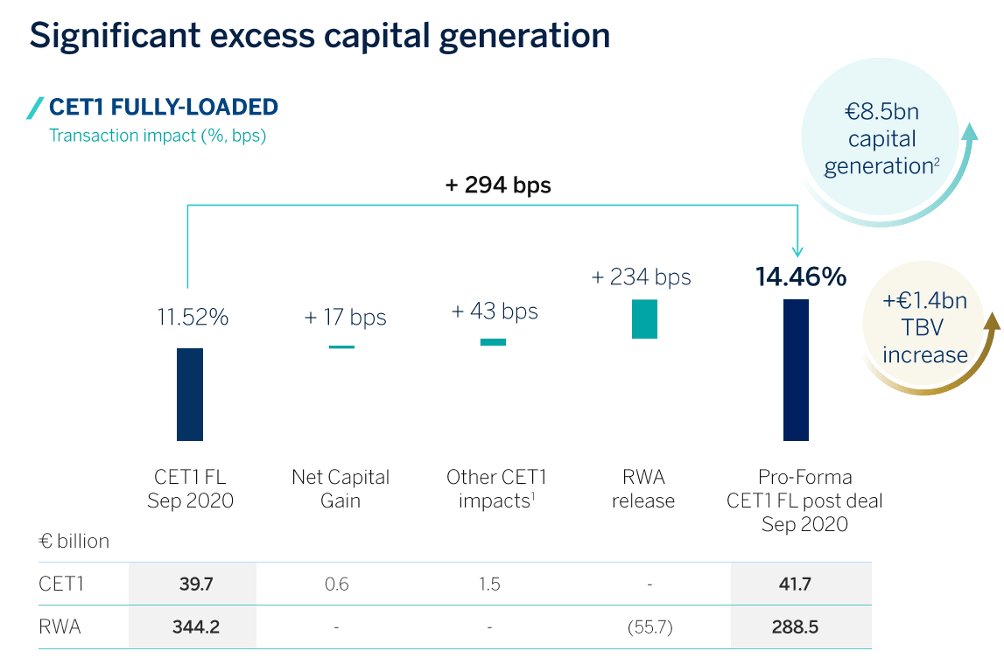

It’s an all-cash deal with a purchase price of $11.6bn (€9.7bn). The deal shows a 19.7x P/E ratio (with reference to 2019 earnings) and the purchase price is more than 2.5 times the average analyst valuation (€3.8bn). Moreover, the purchase price of BBVA’s U.S. subsidiary (which contributed to less than 10% of 2019 Group’s earnings) represents almost 50% of the BBVA’s actual market cap, and it is expected to have a positive impact on CET1 equal to €8.5bn.

Source: BBVA public reports

Based on BBVA’s balance sheet as of September 2020, the purchase price is estimated at 134% of BBVA USA’s tangible book value. With this acquisition, PNC will add to its balance sheet approximately $86 billion of deposits and $66 billion of loans. For the combined entity, in the post-closing scenario, the allowance for credit losses to total loans is estimated to be 2.85%, including reserves for the acquired loans from BBVA USA of 3.85%.

Moreover, merger and integration costs of $980 million are expected by PNC, inclusive of approximately $250 million in write-offs of capitalized items. On the other hand, PNC expects cost savings of over $900 million, through operational and administrative efficiency improvements. Upon closing, PNC intends to merge BBVA USA Bancshares into PNC with PNC continuing as the surviving entity.

On the PNC side, Bank of America, Citi, Evercore and PNC Financial Institutions Advisory acted as financial advisers; Wachtell, Lipton, Rosen & Katz as legal counsel. BBVA was represented by J.P. Morgan Securities plc as financial adviser and Sullivan & Cromwell LLP as legal counsel.

References: Company websites, Bloomberg, Factset, WSJ, Financial Times, Businesswire, KPMG, IMF, Bankinghub

To contact the authors:

Andrea Zenoniani

Christian Filipovic

Matteo Pavoni

Alberto Tricarico

You must be logged in to post a comment.