Introduction:

On the 17th of June, 2021 JPMorgan announced the acquisition of the robot-assisted investment management company Nutmeg for approximately $970 million. Since November 2020, JPMorgan and Nutmeg have been in a partnership releasing a range of ETFs under the name of “Smart Alpha”. The previous partnership and acquisition of Nutmeg will allow JPMorgan to form the foundation of their digital bank “Chase” set to release later this year in the United Kingdom.

Companies’ Overview:

JPMorgan

JPMorgan Chase & Co. (Market Cap: USD 510Bn), founded in 1799 and headquartered in New York, is one of the oldest financial institutions in the United States. The firm offers a range of investment banking products and services in all capital markets, including advising on corporate strategy and structure, capital raising in equity and debt markets and risk management, as well as corporate and the most classical commercial banking services.

The company operates through 4 main different segments:

- Consumer and Community Banking – serves consumers and businesses through personal services i.e. personal loans, home lending, auto loans and credit card services (3Q 2021 net income of $4.3Bn, up 12% YoY)

- Corporate and Investment Bank – offers a suite of investment banking, market-making, prime brokerage, treasury and securities products and services to a global client base of corporations, investors, financial institutions, government and municipal entities (3Q 2021 net income of $5.6Bn, up 29% YoY)

- Commercial Banking – delivers services to U.S. and multinational clients i.e. senior debt products, treasury solutions and broadly speaking credit and financing strategies (3Q 2021 net income of $1.4Bn, up 30% YoY)

- Asset and Wealth Management – comprises investment and wealth management, offers multi-asset investment management solutions across equities, fixed income, alternatives, and money market funds to institutional clients and retail investors (3Q 2021 net income of $1.2Bn, up 36% YoY)

Nutmeg

Nutmeg is a robot-assisted investment management service that operates online. It was founded in 2012 with the purpose of increasing transparency and offering a disruptive alternative to the more prevalent in-person engagement that is characteristic of wealth management. It was the UK’s first and now largest digital wealth management firm.

It uses one of the so-called robo-advisers, who provide clients with low-cost, easy-to-use online tools to assist them in choosing investments. In its fixed allocation mode, it allows users to create an account by answering a questionnaire about their goals, investment horizons and risk appetite. Then, the platform matches the investor’s profile with a pre-built investment portfolio that is managed and rebalanced automatically by trading only ETFs shares. In 2018, fully managed portfolios were provided, in which an investment expert monitors the investment and makes daily changes, allowing the firm to transition from fully automated to hybrid financial advisers.

Nutmeg is a large platform with a diverse set of products that attempts to appeal to a diverse group of investors. It provides a stock and shares ISA, a lifetime ISA, a Junior ISA and a pension program, besides general investment accounts.

Since its launch, the platform has grown significantly, with over £3.5 billion in assets under management for over 140,000 users as the firm continues to invest in revenue development, even though it is not able to turn a profit.

Industry Overview:

The COVID-19 crisis had a dramatic, global impact on the worldwide market, bringing significant volatility and spikes in trading volumes, including in the derivatives market. Investment banks have been under a lot of pressure to digitalize and lower their fees to attract and maintain their customer base as the crisis forced them to face significant cost and revenue challenges.

As a consequence of requiring lower fees to attract customers, investment banks have sought to automate and consolidate their portfolio offerings globally, turning to the acquisition of FinTech and online banking companies that are able to automate and perform AI-based or hybrid management of customers’ portfolios. Lower fees call for higher operating efficiency, economies of scale, tech innovation and a shift to a broader selection of portfolios in the digital economy. The demand for tech and digitalization can be observed within the M&A activity in the financial sector. From the Financial crisis of 2008 up to 2017, there has been extremely low activity; however, in 2018 the number of deals increased significantly with a major bump in 2021. Globally, 28,175 deals (27% YoY) valued at $2.82 trillion (a 132% increase from the first half of 2020) with 54 megadeals (valued above $5 billion).

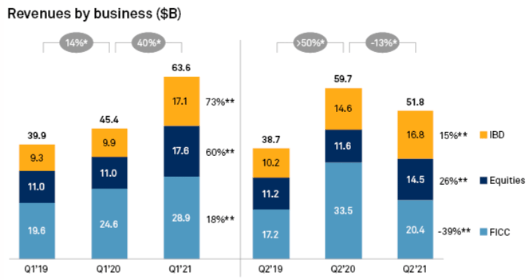

Large global investment banks such as JPMorgan, Goldman Sachs or Morgan Stanley reaped the benefits of this market volatility, achieving highest combined revenue for the first half in a decade. Total investment banking revenues exceeded $115 billion (10% YoY) in the first half of 2021, while at the same period in 2020 it was $105.3 billion. The second half is expected to be slightly lower due to lower client volumes and lower FICC (fixed income, currencies and commodities) due to a decreased market volatility and tightening of yield spreads.

The most significant aspect of booming revenues for investment banks in 2021 is the allocation of cash reserves that have been stored for rainy days. This “dry powder” has been valued at $3.3 trillion as of June 30th and their investment spree has begun since the beginning of 2021. The cash reserves have been a substantial source of M&A financing and the spending has been further intensified by a changing regulatory landscape. The potential of an interest rate benchmark increase would further pressure a pullback in financing activities, heightened scrutiny on megamergers and SPACs, and a potential increase in capital gains tax force financial institutions to conduct M&A transactions before any of these changes or regulations take place. Currently, regulators and CBs have been supportive of the market and the Fed has been keeping the interest rates close to zero to encourage spending and borrowing.

Nutmeg’s Pre-Acquisition Position:

The acquisition of Nutmeg by J.P. Morgan may seem reluctant at first glance. As a company that was established in 2012, Nutmeg has yet to close its losses and turn to profits. According to their 2020 financial results, the company has reported a loss of £15 million, a reduction of 30% from the £21 million loss incurred in 2019. Additionally, it has seen significant growth in the client base, increasing to 130,000, a 53% positive difference from the first quarter of the same year. Neil Alexander, Nutmeg’s CEO, has accredited such improvements to a surge of people opening to investing in order to consolidate financial security in the future of their families and themselves. This increase is also a successor of the company’s significant money allocation to marketing. As a result, throughout the years of its existence, Nutmeg has constructed a name for itself among other major firms. However, despite the combination of positive developments for Nutmeg, the firm is far from having established a solid ground for making profits leaving J.P. Morgan’s decision questionable.

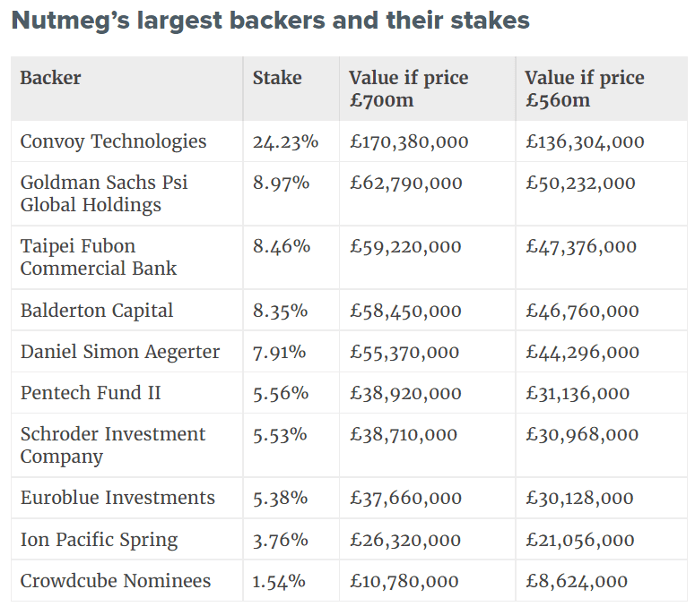

The main winners of the loss-making firm’s acquisition have been Nutmeg’s Hong Kong-based shareholders, who first invested in the company in 2016. Interestingly, two of Nutmeg’s founders, Nick Hungerford and William Todd offloaded their stakes at least 18 months before the sale to JP Morgan.

Crunchbase reports that Nutmeg has had a total of eight funding rounds, raising a total of $153.6 million (£112 million). In October 2019, Nutmeg raised £2.6 million through an equity crowdfunding campaign on Crowdcube, crushing its £1 million funding target. In January 2019, Nutmeg had its Series E funding round, where it raised £45 million. Goldman was one of the prominent investors in this round and Goldman’s partner Rana Yared had joined Nutmeg’s board. She said: ‘Nutmeg has already established itself as one of the fastest-growing wealth managers in the UK.

Deal Rationale:

On June 17, 2021, JP Morgan acquired the robo-adviser Nutmeg. Reuters reported that “Financial terms of the deal were not disclosed, but a source close to the transaction said it valued Nutmeg at close to £700 million ($972.79 million)”. However, the last time Nutmeg raised external funds prior to sale was in 2019, where it had a post-money valuation of £331 million. Which begs the question, why would someone potentially pay more than double the valuation to acquire this company?

The M&A decision may be tied to J.P. Morgan’s grand plan to establish their own retail bank called “Chase” in the UK. The project was kept secret but speculated as the firm began hiring developers and technology-specialized staff to work on a single and undisclosed project. Considering this new development, Chase lacks brand awareness when it comes to other UK savers. This was seen when the launch was compared to Marcus saving accounts, established by their rival, Goldman Sachs. To compete with Goldman, JP Morgan would have to build something completely from scratch. This would cost a lot of money and would also take an enormous amount of time and effort. Furthermore, to make sure customers choose Chase over Goldman, JP Morgan would have to offer a stronger selling proposition. The Nutmeg acquisition fits well with the idea of the full-service offering; in the UK, not only can you go to Chase bank for your personal banking needs, but you can also invest your savings and find professional investing advice at the same place.

In fact, JPM currently does not have a consumer presence in the UK. The Nutmeg acquisition gives them access to an established customer base. JP Morgan dabbled with a D2C platform in the UK, which closed in 2014. Since that time, they have been intermediated and do not have the skillset required to deal with a retail customer directly. Acquiring the knowledge and culture to do so is arguably more important than getting the requisite technology, and buying Nutmeg gives JP Morgan 140,000 customers and a team of people well-versed in supporting them. The online bank in the UK would serve as a pilot for similar operations in other countries. The acquisition of Nutmeg and the launch of the online bank are also in line with Jamie Dimon’s vision to ward off the threat of FinTech companies, which suffer less from legacy systems and regulatory controls, compared to banks.

With all the factors in mind, the acquisition of Nutmeg by J.P. Morgan has a central strategic element to the decision. An already established brand name of Nutmeg, the majority of which comes from the first-mover advantage, including its technology will allow J.P. Morgan to utilize and incorporate such assets into their own retail bank Chase and its upcoming online banking project.

Sources: Financial Times, Nutmeg, Investopedia, S&P Global Market Intelligence, PwC, Deloitte

Authors: Christian Filipovic, Alberto Tricarico, Andrea Zenoniani, Kiril Perfiliev, Akshay Shrivastava

You must be logged in to post a comment.