Introduction

On May 17th 2021, AT&A announced a $48 billion deal to merge Discovery and WarnerMedia, uniting the companies under the name Warner Bros. Discovery. The merger should provide substantial synergies and an improved leadership team that will strengthen the streaming and content creation verticals, enabling the company to compete with companies such as Netflix or Disney.

Companies overview

WarnerMedia

WarnerMedia is an American multinational mass media and entertainment corporation that owns many well-known brands, such as Warner Bros, HBO, Boomerang, Cartoon Network, Boing, TNT, Cartoonito, and many others. It was created in 1990 by the merger between Time Inc. and Warner Communications under the name of Time Warner.

In 2016, AT&T announced the offer of 85 billion dollars to acquire Time Warner, but the deal was blocked by the U.S. Department of Justice (DOJ) because of antitrust reasons. In 2018 the merger was finally approved, and the name of the company was finally changed to WarnerMedia. The merger pushed WarnerMedia into the market of streaming services with their new direct-to-consumer streaming platform HBO Max.

The last year has been really tough for WarnerMedia, as the pandemic caused the near-universal shutdown of TV and film production and cancellation of marquee events like the 2020 NCAA Final Four. In such a period of uncertainty, the subscription business is becoming more and more important, especially for WarnerMedia. Consumers and businesses have more than 225 million monthly subscriptions, representing nearly 60% of AT&T’s total revenues.

Discovery

Discovery, Inc. is an American multinational mass media factual television company. It was founded in 1985, and it has always been based on reality and lifestyle television brands. The company’s leading brand has always been Discovery Channel, first launched on June 17, 1985. Discovery’s portfolio of premium brands also includes HGTV, Food Network, TLC, Investigation Discovery, Travel Channel, Turbo/Velocity, Animal Planet, Science Channel, and Eurosport.

Discovery is a global leader in the entertainment industry available in 220 countries and 50 languages. It is focused on innovation, and it has followed the trend of direct-to-consumer opportunities with its streaming platforms Discovery+, Eurosport Player, Discovery kids play! and many others. The focus of revenue is on advertising, which comprises more than 50% of net revenues for this segment.

The pandemic had an indirect impact on Discovery. Advertising partners of Discovery continue to reduce their promotion spending, and there have been problems related to live sporting events revenues. Advertising revenues fell after the postponement of the Olympic Games, a big source of revenue for Discovery’s brand Eurosport.

Industry Overview

The Media & Entertainment (M&E) industry has changed over the last few years and is still in a state of transformation, as both old and new companies continue to coexist. The factors that have disrupted the industry in the last years are interactivity, digitization, multiple platforms, multiple devices, and globalization of services. The pandemic has accelerated trends that were already underway. For example, major studios are making first-run movies available directly to consumers through streaming services. Customer retention has become very important, as providers are starting to offer a broad range of content, such as video, music, games, and podcasts.

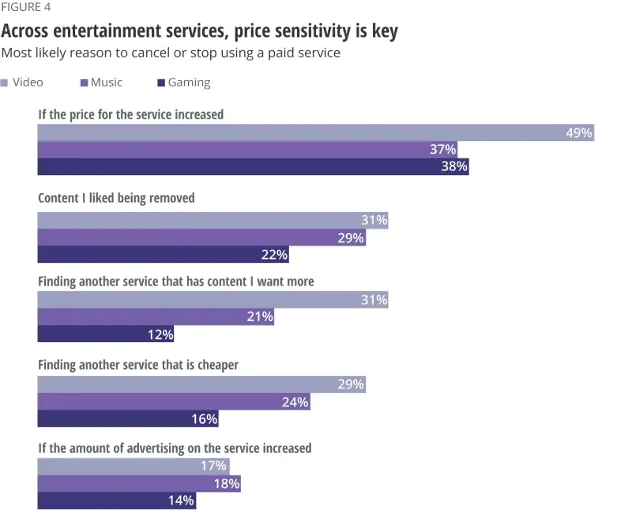

The Media & Entertainment industry has become increasingly competitive during the last year, and customers are aware of the alternatives available and want tailored options in terms of content and pricing. The churn rate among OTT services in the United States rose from 35% in Q1 2019 to 41% in Q1 2020. Also, aggregation seems inevitable to retain customers and concentrate the market because customers are less willing to rely on multiple entertainment services. According to Deloitte’s COVID-19 Digital media trends survey, 39% of respondents reported a decrease in their household income since the pandemic began. Consumers who lost income during the pandemic were more than twice as likely to cancel a streaming service because of the cost compared with those whose income was unchanged.

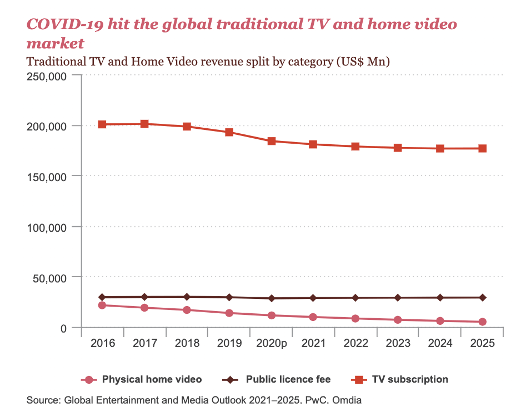

Looking at the Traditional TV and home video services, the industry where TimeWarner and Discovery had the most exposition, COVID-19 had a largely negative effect on the global pay-TV market. Thus, this accelerated the trend of consumers moving away from traditional delivery towards the internet, and the setbacks created a physical barrier to on-premises installation and the rollout of infrastructures. The pandemic accelerated the decline of satellite and cable, which is under pressure in North America due to high prices and in Asia-Pacific due to competition from IPTV. North America remains the largest traditional TV and home video market with a 42.3% share of global revenue in 2020. However, revenue is falling, and the region will account for just more than a third of the global market in 2025. Of the four forms of distribution, cable, IPTV, satellite, and pay-DTT, cable has seen the largest decline in terms of household, losing 81mn households over the last five years.

The US telecommunications network did a great job of adapting and driving changes to how people live, work, learn and play since the COVID-19 pandemic. In the next year, the role of the industry will be even broader as 5G wireless technology begins to gain traction among consumers. 5G wireless technology will provide new opportunities to transform how enterprises operate and deliver products and services. For example, in the entertainment industry, there is a shift towards the implementation of Internet of Things services, such as sensors. The move to next-generation wireless technology, such as 5G, will create a competitive advantage for the entertainment industry and will unlock opportunities for innovation.

Deal rationale

Although there were some weeks of regulatory uncertainty due to the sheer size of the deal, the green light was eventually given in September. The new company, only recently officially renamed Warner Bros. Discovery, will be led by Discovery CEO and President David Zaslav. He hopes to make use of valuable synergies, particularly concerning brand recognition and customer base. It will be big enough to compete with recently dominating media giants Netflix and Disney, as the two merging companies spend on content more than both of these rivals last year. Crucially, the merger will enable AT&T to better cover multiple steps along the value chain in the media industry, most prominently production and distribution. Furthermore, Zaslav already laid out concrete ambitions by Warner Bros. Discovery to differentiate itself by combining classic streaming entertainment with rigorous sports and news coverage. The aim for the new company is to eventually supply 400 million homes across the world with content, which would roughly quadruple the current combined customer base of WarnerMedia and Discovery. Discovery’s strong European customer base is viewed as an ideal complement to WarnerMedia’s grip on the US market.

However, one element of the deal that should not be swept under the table is that this spin-off merger is by many considered a reversal of the huge $100 billion acquisition of WarnerMedia, at that time still Time Warner, by AT&T. Back in 2016, the telecommunications giant thought that acquiring an entertainment powerhouse would propel it to a next-level corporation that could compete with the big technology giants through effective usage of consumer data and preferences. In hindsight, critics believe this move proved to be slightly overambitious, leaving the WarnerMedia unit somewhat stranded in AT&T’s company portfolio that also includes CNN and HBO.

Apart from this potential, subtle admission of wantonness, AT&T’s decision to merge its content unit WarnerMedia with Discovery also fits into the general trend of consolidation in the media industry. The media and entertainment industry and especially the streaming industry saw multiple large mergers in the last few years. Disney took over 21st Century Fox and acquired its majority stake in Hulu. This enabled Disney to enter the streaming market and Disney+ quickly became one of the leading services. Similar reasoning triggered Comcasts’ merger with Sky to create Peacock. AT&T took over Time Warner to set up WarnerMedia and launch HBO Max.

The main rationale behind all the recent mergers is increased competition with big industry leaders like Netflix and Prime Video. Customer habits and market structure imply a critical size for successful players. Firstly, customers prefer to have only a few subscriptions giving them access to a large amount of content. Secondly, the production of its own content, which offers a USP over competitors, requires big investments which are not feasible for smaller players. In contrast to the early stage of streaming, significant customer base growth to achieve this critical size can nowadays only be achieved when merging players. Moreover, perhaps the most important reason for consolidation is the access to additional content. The amount of content is undoubtedly the most important decision criterion for customers. However, media licenses and rights are usually concentrated at one company and often only accessible on this company’s streaming platform. A merger offers the opportunity to quickly expand the content catalogue and appeal to customers. Additionally, with increasing size operating efficiencies arise and can unlock incremental capital. This can be invested in growth, better technology and especially more content or own productions.

Because of the stated reasons, the trend of consolidation is likely to continue in the near future. Aside from growing existing players, M&A also presents a favorable option for more traditional players in the media industry to enter the streaming market and expand the reach of their content. A similar case recently also took place within the circle of the big tech giants like Apple. These companies are highly interested in their own share of this multi-billion market and might fuel the market with additional capital.

Deal structure

The deal will be pursued through an all-stock Reverse Morris Trust transaction. Essentially, that means that WarnerMedia will be split off to AT&T’s shareholders via dividend or through an exchange offer and simultaneously merged into Discovery. Thus, the transaction is expected to be tax-free to AT&T and its shareholders.

Discovery will be contributing 100% of its business and will receive 29% of common equity in the new company. Its current multiple classes of shares will be consolidated into a single class with one vote per share. On the other side, AT&T will receive $43billion in a combination of cash, debt securities, and WarnerMedia’s retention of certain debt. Its shareholders will gain 71% ownership of the NewCo.

This is a simple scheme of the deal structure:

The newCo expects to use the cash flow resulting from the combination to rapidly de-leverage to about 3.0x within 1 year, with a target of a longer-term leverage target of 2.5x. LionTree and Goldman Sachs served as financial advisors to AT&T, while Allen & Company and J.P. Morgan were financial advisors to Discovery. The transaction is expected to close in mid-2022, subject to approval by Discovery’s shareholders and regulatory authorities.

The market’s initial reaction was positive, with Discovery’s shares rising 3.1% the day after the announcement. After an initial uplift, shares of AT&T fell 2.7%, as investors became concerned about the expected dividend cut. In fact, AT&T will reduce its dividend due to the loss of WarnerMedia’s free cash flow. The company said it expects to pay an annual dividend payout ratio of 40-43% on the anticipated free cash flow of over $20 billion, instead of the 55% payout ratio its shareholders had received in 2020.

Sources: Deloitte, The Verge, CNBC, NBCNews

Authors: Kurt Niklfeld, Edoardo Zanetta, Giulia Zanetello, David Landau, Stefano Stompanato, Marco Cavalieri

You must be logged in to post a comment.