Introduction

On 23/11/2020, Crédit Agricole Italia S.p.A. (“Crédit Agricole Italia”) announced a voluntary public tender offer on all shares of Credito Valtellinese S.p.A. (“Creval”) with a total deal value of €876.87m. The deal was closed on 21/04/2021. Crédit Agricole Italia offered a price of €10.50 in cash per Creval share which represents a 20.76% premium over Creval’s closing price on 20/11/2020 (€8.97) and a 53.02% premium over Creval’s closing share price on 23/10/2020 (€6.86), one month prior to the announcement.

Company Overview

Crédit Agricole Italia

Crédit Agricole Italia is an Italy-based banking group engaged in providing various banking services and a 75.6% subsidiary of Crédit Agricole SA (“Crédit Agricole”). As of right now, the CEO of Crédit Agricole Italia stands to be Giampiero Maioli and the company is ranked as the 11th largest bank by total assets in Italy. Crédit Agricole is a France-based and publicly listed provider of financial services in retail and wholesale banking services, property, casualty and life insurance, and asset management. The company was founded in 1894 and is headquartered in Montrouge, France. The operating segments of the company are the following: Asset Gathering, Large Customers, Specialised Financial Services, French Retail Banking – LCL, and International Retail Banking.

Credito Valtellinese S.c. (“Creval”)

Credito Valtellinese is an Italy-based regional and formerly listed bank offering banking services as well as asset management, private banking, leasing, and insurance services. The company is a leading banking group focused on households and SMEs in Italy with total assets of €24bn as of September 2020. Prior to the bidding, the company has operated 363 branches located in the Northern Italy, 133 branches located in Sicily and 40 branches in Marche and Umbria with a few more around Italy.

The company operated through the following segments:

- Commercial Banking – Comprises the company’s complete service portfolio of lending products including factoring as well as investment and transfer services. The segment is sub-divided into retail and corporate customers.

- Finance, Treasury and ALM – Comprises the management of interbank, loans, and institutional funding as well as funding in securities.

- Equity Investments and Other – Comprises the company’s management of group’s equity investments and non-classified investments.

COVID Impact

Among many other companies worldwide that have suffered from the devastating effects of COVID-19, Crédit Agricole Italia has likewise experienced the uncertainty and losses brought by the pandemic. Nevertheless, the group has been swift and competent in addressing personal complications while supporting their stakeholders and other charitable organizations. Crédit Agricole Italia have begun immediate approval of loan requests up to €25,000 for companies with a total of €4bn that has been dedicated for usage in medium-term financing. This plan of action includes those firms with a turnover of less than €3.2m.

Moreover, for small businesses, SMEs and corporate clients, the group has announced a 6 months loan repayment moratorium, with a possible 6 months extension. All of this is accompanied by other charitable responses, such as donating €2m to the Italian Red Cross in order to help with the effects of the pandemic.

INDUSTRY OVERVIEW

Over the last two decades, Europe’s banking sector has seen significant transformation. Even if the EU countries have gone at their own pace in revamping their banking systems in the past, consolidation is a vital feature of every country. Innovation technology, disintermediation, deregulation processes, and globalization of real and capital markets are among the key drivers of the consolidation, as well as the introduction of the European currency. As a matter of fact, it is possible to find a positive correlation between the increase in the number of M&A operations in the whole European banking industry and the initiation of the Monetary Union.

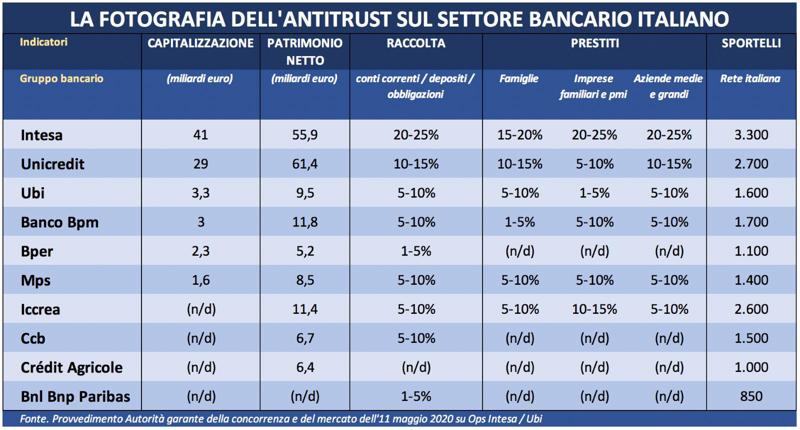

The Italian banking sector, at the beginning of the 2000, was characterized by a large amount of small and high skilled banks, which were deep-rooted in limited areas. The consolidation’s process, that began at the end of 1990s, affected almost half of the Italian banking system leading to a big reduction in the number of operating banks. In the time frame of 1993-2014, the number of operating banks noted a reduction of 35%, from 1037 banks and down to 672. The most relevant falls occurred in 1993-1995, 1998-2004 and in 2007-2014, with the last stage highlighting the birth of big banking groups such as UniCredit S.p.A and Banca Intesa San Paolo. These groups from the beginning got a large market share in Italy. In 2017, indeed, the first five institutions detained a combined market share of 43.3%, with Intesa leading the way with a 20-25% of market share, followed by UniCredit with a 10-15% of market share. This index is pretty much in line with the average within Europe, depending on the country. In Spain, for instance, the first five banks detained a market share of 63.7%, while in Germany they hold only 29.7%. Another trend, that happened in Italy and in the rest of Europe, was the reduction of the number of branches and occupants. Italy recorded a reduction of the number of branches by 33.1%, about 9600 branches, from 2009 to 2017. In the same period, the resources applied declined by 21.8% with a drop of 86,000 occupants in the banking industry. Nevertheless, at the end of 2016, the ratio between the number of branches per inhabitants was among the highest, with 50 branches for every 100,000 inhabitants.

The consolidation process was the outcome of a strategic decision made by numerous banks in order to stay afloat. To remain competitive, every bank had to maintain a high degree of efficiency, which necessitated expanding policies aimed at cost reduction, diversification, and exploitation of economies of size and scope. There are 2 different growth routes:

– Internal: the bank is attempting to increase its reach and activities by leveraging its own internal resources and existing structure.

– External: Through mergers and acquisitions, the bank hopes to grow its size.

The external path is faster, and it is the one that the vast majority of banks choose to adopt in order to meet increasing competitive pressures and prevent losing market share.

The Italian banking industry has recently been shaken by a fresh wave of consolidation spurred by the low-rate and inflationary environment, which has piqued the interest of the second-tier segment in particular. Because they have limited business diversification and rely heavily on net income, traditional mid-sized commercial banks have struggled greatly with long-term low interest rates. An inflation rate of 6.5 percent in March 2022, the highest in 31 years, has put more pressure on banks’ profits as operational costs rise. Because mid-sized banks have limited capacity to cut costs on their own, consolidation could result in cost savings through the rationalization of internal operations and processes, the reduction of branches and offices, and the availability to cheaper funding. The main drivers of this new consolidation wave in Italy’s second tier banks are improving profitability and enhancing sustainability, as well as adding complementary distribution capabilities, expanding geographical coverage and local footprint, and boosting solvency levels and credit ratings. Nonetheless, BPER Banca’s acquisition of bank Carige shown that profits aren’t the only motivators. Consolidation can be an effective technique for resolving crises in smaller banks and absorbing failing business models, especially if the government provides incentives to favor the acquisition.

A total of USD 847.2bn has been spent on European assets in 2020 across 6,658 deals, representing a 5.6% rise by value versus 2019 (USD 802.3bn). This was largely due to the recovery seen in the second half, with USD 552.7bn recorded, 87.7% higher than the USD 294.5bn seen in the first six months of 2020. The number of deals, however, has remained fairly subdued throughout 2020; There have been 6,658 deals announced in Europe, its lowest annual deal count since 2013 (5,915 deals).

With restrictions limiting international travel and the traditional methods of conducting M&A, the majority of European M&A in 2020 was conducted internally. Foreign investment into Europe represented 37.8% of the total European value and 15.4% of the volume, representing its lowest value share since 2015 and lowest volume share since 2009.

To summarize, in a complicated and constantly evolving regulatory framework as well as a digitalized world, dimension is a critical aspect in ensuring long-term sustainable growth and returns by providing additional opportunities to capitalize on external growth prospects.

DEAL RATIONALE

The success of the tender offer has allowed Crédit Agricole Italia to continue its growth in Italy, both in terms of size and market positioning. The integration of Credito Valtellinese has created a new, robust and profitable Italian banking group that has benefited from a strengthened local footprint. The transaction is consistent with Crédit Agricole’s strategy to prudently scale up the group’s moderate retail and commercial franchise in Italy, the group’s second-largest market after France. Central to its strategy has been increasing cross-selling of group products, in particular asset management, life insurance, consumer finance and corporate and investment banking in Italy. The acquisition added about 0.7 million of customers to its existing 2.1 million Italian customers.

Fitch Ratings reported that this acquisition is a major deal for Crédit Agricole Italia as it has led to a 30% growth of its total assets from €76 billion at end-September 2020. Crédit Agricole Italia’s franchise has benefited from the integration of Creval’s retail branch network, reinforcing the group’s position in northern Italy, especially Lombardy, where Crédit Agricole Italia’s market share by number of branches has doubled to 6%. It is also notable that Crédit Agricole and Creval already have an exclusive distribution partnership in life insurance in Italy.

Prior to the transaction, it was speculated that the acquisition of Creval would help Crédit Agricole Italia improve its profitability, which at the time was below the latter’s 2022 target, through both revenue synergies derived from cross-selling of group products to a larger retail base and cost synergies from the integration of Creval’s operations into Crédit Agricole Italia’s platform. Creval’s profitability has been impacted by the recent de-risking strategy. This transaction represents Crédit Agricole’s second external acquisition in Italy in the last three years in the retail and commercial space after the acquisition of three small regional banks in 2017 and a private bank in 2018. Crédit Agricole Italia enjoys a sound record in integrating past acquisitions.

DEAL STRUCTURE

Regarding the deal structure of Credit Agricole Italia’s voluntary public tender offer for all shares of Credito Valtellinese (CreVal), the bank opted for a stock purchase. A tender offer is a public bid for stockholders to sell their stock. In M&A, there are typically three main methods of deal structuring: asset acquisition, stock purchase, and merger. Each method has its advantages and disadvantages. Credit Agricole Italia offered to control all ordinary shares of Credito Valtellinese S.p.A., bringing its ownership up to 91.17% of the company from its already owned 2.45%. Credit Agricole Italia paid 12.27 EUR per share, ex dividend. CreVal also paid a dividend of 0.23 EUR per share on 28 April 2021, raising the total offer price to 12.50 EUR per share. This acquisition calculated an expected ROI above 10% by year 3, solely including cost and funding synergies. Additionally, it would have an accretive effect for Credit Agricole S.A.’s stock, Credit Agricole Italia’s controlling shareholder. On 20 November 2020, three days before the deal was announced, CreVal’s stock traded at 8.652 EUR. After a couple of addendum, the new offer of 12.5 EUR per share represented 44.5% premium.

With a stock purchase acquisition, the bidder acquires most of a seller’s voting shares. The buyer then gains control of the seller’s assets and liabilities. Some advantages of a stock purchase acquisition are that it may be less costly than a merger or asset acquisition, it is a less time-consuming process because negotiations are more straightforward, and the taxes, especially for the seller, are minimized. Some disadvantages include the possibility of uncooperative minority shareholders that refuse to sell their shares or other legal and financial liabilities involved in a stock purchase acquisition.

Authors: Christian Filipovic, Arne Hochheim, Fabio Tessiore, Alberto Tricarico, Andrea Zenoniani, Kiril Perfiliev, Akshay Shrivastava

Sources: Credit Agricole Italia, Credito Valtellinese, ECB Europa, Fitch Ratings, PWC, Reuters

You must be logged in to post a comment.