ONE OF THE LARGEST LBOs IN HISTORY ACCEPTED – WILL IT GET TO THE FINISH LINE?

On April 25th, several days after acquiring a 9.2% stake in Twitter, the richest man in the world, Elon Musk submitted a takeover offer at $54.20 per share, implying a total equity value of $43.4bn, to take Twitter Inc. private. The takeover offer would represent one of the largest LBOs in history, with a 38% premium to the company’s closing price on April 1st. After launching a poison pill defence to fend off the bid, the Board accepted the takeover offer as Elon Musk unveiled the $45bn financing package.

ELON MUSK

Originally from South Africa, Elon Musk initially founded several successful start-ups, including Zip2, a company that provided maps for businesses, and X.com, today better known as PayPal. Once he sold these businesses, he founded one of the leading private aerospace companies, SpaceX, and Tesla, the world’s most valuable automaker with a market capitalization of nearly $1 trillion. Elon Musk is currently the richest man in the world, with a net worth of $250bn.

COMPANY OVERVIEW

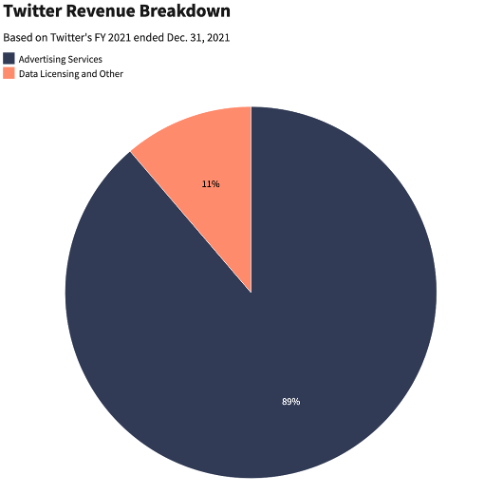

Founded by Jack Dorsey in 2006, Twitter is a social media company typically used by important figures like politicians, celebrities, and renowned entrepreneurs. It provides users a place to conduct a debate, share their thoughts, and interact with each other using the so-called Tweets. Subscription to the platform is free, requiring only the creation of an account. The company generates revenues mainly from two outputs: the sale of advertising services, which represents the vast majority of the company’s revenue, and other services such as data licensing. In 2021, advertising services generated 89% of Twitter’s revenue, about $4.5bn. The products sold include Twitter Amplify, Follower Ads and Promoted Ads. Advertisers have the possibility to target their ads by using Twitter’s algorithms based on multiple criteria, such as searches, likes, and comments. Data licensing and other services generated $571.8mn, just 11% of the total revenue, with a 12.3% growth from the previous year.

BID HISTORY

In the last decade, the company has grown at a slower pace compared to other social media platforms, including LinkedIn and Facebook, and reported lower profitability than in the previous years. Twitter has previously received several potential bids to be acquired, citing its undervalued price and high potential as a social media platform. Back in September 2016 Salesforce, the cloud-based marketing company, mediated a potential offer, due to their interest in creating synergies between Twitter’s data and its own services, creating a potential deal worth around $26bn. Together with Salesforce, Disney, Alphabet and several private equity funds, Twitter discussed other potential offers with shareholders. However, none of the companies decided to proceed with a formal bid, due to concerns about “bullying and uncivil forms of communication that could spoil the company’s image”.

This is a prime example of why Elon Musk is motivated to buy the firm; having a broadly inclusive public platform b where everyone can conduct a democratic debate, putting emphasis on the promotion of free speech. Several weeks after the bid, Twitter investors launched a poison pill defence in order to protect the shareholders’ rights. This type of defence allows an existing investor to have the option of buying additional shares at a discounted price if a particular event occurs (e.g. a hostile takeover). The consequence of this plan would include the dilution of the share value, making it impossible for a raider to obtain significant control or a majority stake of a given company.

CURRENT SHAREHOLDERS

The current shareholders are mainly institutional investors. The largest stake is controlled by its co-founder Jack Dorsey, who owns 9.4% of the company’s shares, The Vanguard Group, a global investment manager with 10.3%, investment bank and asset manager Morgan Stanley with 8.4%, BlackRock with 6.5% and State Street Corp., an institutional services provider, with 4.5%.

Deal Rationale

Musk’s main line of argumentation is that every successful democratic society needs an independent platform promoting free speech, which he does not see provided for by current management. This is also the reason he cites when asked why he ended up declining to join the Twitter board after initially accepting an according offer in the wake of his 9% share acquisition in March. A position on the board would have prevented Musk, who is an avid Twitter user himself, from ever owning more than 15% of the company.

Critics are voicing concerns that this private takeover will in practice have the reverse effect, placing too much decision-making power in the hands of a single individual. Additionally, speculation and debate about a potential Twitter comeback of Donald Trump under Musk’s ownership flared up. High-ranking politicians of both the Democratic and Republican parties are having their say on the matter, easily distinguishable by their contrasting opinions. Such discussions highlight the public interest in this deal and its consequences, which in turn, is free PR for the Tesla CEO. Initially, many believed that this saga was a high effort publicity stunt. After all, Elon Musk had theoretically been able to withdraw his offer at any time, but the recent conclusion of the transaction has put an abrupt end to this theory.

According to Elon Musk, he “does not care about the economics of it at all”. At an acquisition cost of around $44 billion dollars, this is at least partially doubtful. In practice, owning Twitter could allow Musk to smoothly promote his visions and products in an even more noticeable fashion, effectively creating the ultimate marketing platform. While the entrepreneur has vowed not to abuse Twitter’s user base of 330 million people for his own purposes, the potential venues of intensified advertising are limitless. What is probably true is that the billionaire did not acquire Twitter based on its financial performance. The company has been notoriously struggling to be profitable, with the years 2018 and 2019 representing exceptions that most do not expect to repeat anytime soon.

In a recent TED Talk, Musk had already laid out his rationale and potential plans of action before his takeover bid went through. By taking the company private, he believes the necessary amendments to Twitter can be made away from shareholder/stock market pressure and profit orientation, unlocking the company’s “extraordinary potential”. The improvements proposed include technological tweaks such as an edit button and an open-source algorithm but also a shift in corporate policy, entailing higher tolerance in tweet-removal and less moderation. It remains to be seen how big of a revolution Musk will actually kickstart after his Twitter takeover. While certain aspects of the acquisition do make sense from a strategic point of view, the financing and public pressure of this deal were and will continue to be hurdles that should not be underestimated. Musk himself admitted to being wary of both of these concerns, stating “I’m not sure I’ll actually be able to acquire it…If I acquire Twitter and something goes wrong, it’s my fault 100%.”

Deal structure

The takeover of Twitter would be the biggest acquisition financing ever put forward for one person. Not by chance, Elon Musk has accustomed us to many surprises. The board of the company stated on April 25th its willingness to sell the company for around $44 billion ($54.20 per share), after Musk announced last week he had secured a financing package of around $46.5 billion for the Twitter bid. The purchasing price represents a premium of 38% to the closing price at the beginning of April. The buyout would be structured in reverse to how typically LBO investors do it. In fact, more than two-thirds of the financing package would come from Musk’s own assets, with the remaining part will be represented by bank-secured loans using Twitter’s assets as collateral. Normally, the majority of the financing is represented by secured debt and not by equity. In this case, banks, including Morgan Stanley, have agreed to provide $13 billion of secured debt to finance the acquisition. However, those creditors have hesitated to provide more secured debt against Twitter, complaining that the social media platform does not produce, up to this date, enough cash flows to justify further expense. Musk has therefore committed to providing $33.5 billion, split between $21 billion of his own equity and $12.5 billion of margin loans against his stock of Tesla. This loan is very risky since the agreement is that, if Tesla’s share drop by 40%, Musk would have to repay the loan in full. Additionally, interest and amortization expenses can potentially go up to $1 billion annually.

But now the question arises: where would Musk take that $21 billion of cash from? It is unclear whether he has enough cash immediately available, and whether he would have to cash out some of its assets, including stakes in Space X, Boring Co., or even Tesla. Regarding the latter one, if we look at the commitment letter signed along with the margin loan, it is written that Musk “may sell, dispose of or transfer” unpledged Tesla stocks at any time. Given the difficulty in covering the equity financing, Musk may seek help from additional partners. According to the news, PE investors like Thoma Bravo and Apollo Global Management have shown interest.

PEER ANALYSIS

Did Elon Musk overpay Twitter?

The offer of $54.20 per share proposed by Elon Musk and accepted by the board is made at a significant premium compared to the current level of peers on the market. The operation values Twitter at a 6x EV/Revenue FY23 and 28x EV/EBITDA FY23 level, higher than the sectoral median at a 3.5 EV/Revenue FY23 and 17.0 EV/EBITDA FY23 level. For comparison, Pinterest, Snap, and Meta Platforms (Facebook, WhatsApp, Messenger, Instagram) are valued at 3.5x, 3.9x, and 8.0x for next year’s EV/EBITDA FY23 and 15.7x, 8.4x, and 60.0x for EV/EBITDA FY23 level, respectively.

For the last years, the company’s results have not been brilliant. In 2021, despite the rise of advertising revenues by 40% and global revenue by 37%, the cash generated by operating activity decreased by 37% to reach $633 million. Compared to the median of its peers, Twitter demonstrates a lower sales growth of 36.7% (vs. 41.2%) but a higher EBITDA margin of 21.0% (vs. 17.6%). The company is still lagging on the Return on Invested Capital, reaching only 2.04% vs. 4.38% for the median of its peers. In a market concentrated with a significant advantage for the market leader, Twitter is still underperforming compared to Meta, which achieved better results with 37% sales, 47% EBITDA margin, and a tremendous 25.90% ROIC. Some analysts estimate that Elon Musk overpaid Twitter as the operation has been performed on significant multiples. However, some acquisitions based on higher valuations have been observed in the past. In 2016, Microsoft purchased LinkedIn for $26.2 billion at a 7.2x EV/Revenue LTM and 79x EV/Revenue LMT level. Microsoft has significantly improved the social network’s management and fostered its long-term growth in the last years. Knowing whether Twitter was overpaid or not may be assessed in the light of the future transformation results of the company.

A shadow of its former glory with few users and low ARPU!

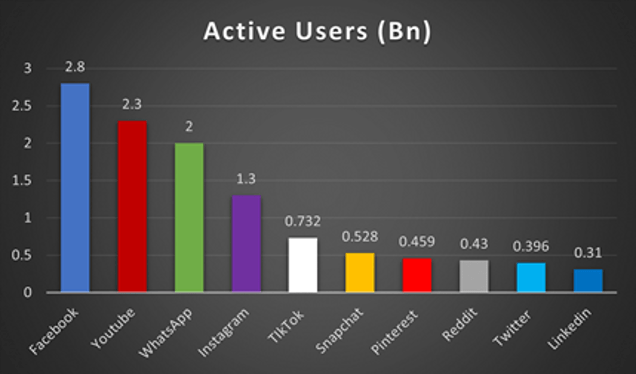

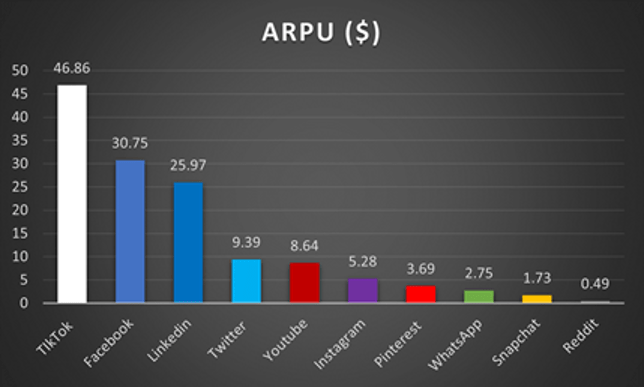

After being a pioneer in the social media industry, Twitter is currently a shadow of its former glory, lagging behind the leaders in many active users, revenue, and Average Revenue Per User (ARPU). With only 396 million active users, a number comparable to Reddit or LinkedIn, Twitter is positioned as a “niche” social network mainly used by a small number of highly engaged users. However, despite this particularity, which should theoretically ease the platform’s monetization, Twitter only generates an ARPU of $9.39. In comparison, LinkedIn has an ARPU of $25.97.

WHAT IS GOING NEXT FOR TWITTER?

A significant and highly risky bet!

Although Elon Musk affirms that this acquisition is uniquely motivated by his willingness to defend democracy and promote freedom of speech, this operation is an absolute financial and operational bet. This operation represents a bet on the company’s side and Elon Musk’s wealth. Elon Musk has contracted a $12.5 million margin loan collateralized with the billionaire’s participation in Tesla. He pledged more than $65 billion in value in Tesla shares representing more than a quarter of his current Tesla ownership, to secure his loan. According to Audit Analytics, Musk has currently pledged more than $90 billion value of shares reserved for its different loans.

Improving the company’s performance on both operational and financial sides will become an imperative necessity after the buyout. The deal structure to acquire the company triple the company’s leverage, adds $25 billion of supplementary debt, and charges $845 million of additional yearly interest rate expenses for Twitter. Consequently, to face the interest expenses, the company will have to improve its cash flow generation significantly, as in 2020m Twitter only generated $632 million of operating cash flows. Furthermore, it is essential to note that most of the debt contracted by the company is based on floating rates. A rise in the interest rates may represent a significant risk for the group’s financial stability.

How to revamp Twitter’s financials?

As previously stated, revamping Twitter’s financials will be a critical point for the operation’s success. For most analysts, one of the current weaknesses of Twitter is its revenue structure. The company is highly dependent on advertising and data licensing, which are threatened by either systemic conditions or long-term changes in the legislative framework. Advertising is a highly cyclical and unstable market. For instance, in case of bad buzz linked to the platform, there is a significant risk that advertisers and communication agencies may reduce their spending on the platform. Second, the data licensing business is increasingly vulnerable to new regulations restricting business possibilities, such as the EU’s GDPR (General Data Protection Regulation) and DSA (Digital Services Act). Until now, all the company’s attempts to diversify its revenue streams have failed. Recently, Twitter Blue, the platform’s subscription service launched in June 2021, has been unable to provide clear advantages and attract clients.

Although Elon Musk did not formally disclose any official plan, some insiders have already revealed some potential evolutions that may happen after the deal’s closure. Elon Musk announced during presentations to banks that he wants to reduce costs and perform job cuts. He also mentioned in several tweets that he is planning to eliminate the boards’ remuneration to save $3 million and reduce the stock-based compensation plan amounting to $630 million last year. Apart from those elements, the magnitude of potential economies is still unclear at the current point. The increase in the company’s revenue and particularly the ARPU would be a more efficient way to improve its finances than cutting its actual costs.

The billionaire has already announced his ambitions to reduce the part of advertising in Twitter’s revenue and set up a more solid subscription-based model. Some insiders also inferred that Twitter might charge a fee for a third-party website that wants to embed a tweet from verified individuals or organizations. Some external analysts also suggest other strategies. The most cited include: reviving Twitter Blue subscription with more interesting functionalities, allowing payment in dogecoin on Twitter, or transforming the platform to leverage the development of WEB 3.0.

Sources: BBC, Financial Times, Investopedia, New York Times, Bloomberg, Wall Street Journal, Reuters, CNBC

Authors: Kurt Niklfeld, Edoardo Zanetta, , Giulia Zanetello, Paul Thiriot, Stefano Leone

You must be logged in to post a comment.