About Celanese

Celanese was founded in 1910 and grew to become a global firm with 7,700 employees, 25 production plants and 6 research centres around America, Europe, and Asia. It is a Texas-based global chemical and plastic producer, especially in the field of polymer and high-value materials revolving around plastic.

It has a wide portfolio of materials, offering:

- POM (“polyoxymethylene”, often known as “polyacetal”): High stiffness plastic often used in mechanical gears, electrical engineering and vehicles. To illustrate, BIC lighters are made of POM.

- UHMW-PE (“Ultra-high-molecular-weight polyethylene”): A thermoplastic polyethylene resistant to corrosive materials (15 times more than steel in some instances) and low friction. It is often transformed into fibers in instances such as personal and vehicle armor, climbing, diving and sailing cords. To illustrate, UHMW-PE is often used in the production of PVC windows.

- Polyester, a category of polymers often used to produce clothes.

- Nylon: A family of synthetics polymers that can be easily processed into fibers for various uses such as clothing, resins and military supplies.

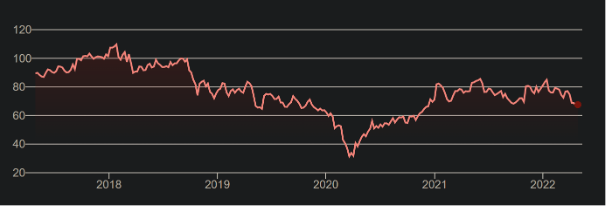

These are examples of materials that it sells but it has many other offerings. It is to be noted that while its offering revolves around materials commonly known as “plastic”, their wide range of products enable them to have clients working in many other industries, making their business model more predictable, less dependent on the ups and downs of a single sector. As such, it sells solid plastics but also preservatives or sweeteners and it serves clients working in the automotive sector, infrastructure, construction, healthcare, food and personal care industries. It is operating in a fast-growing segment of the chemical industry, the “Downstream” segment which, while it is dependent on the price of raw materials used in the production process, it is positioned to be able to differentiate itself through innovative materials that it can sell with higher-margins than in the “Upstream” segment. The strategy of Celanese is to consolidate its leadership position in some materials by ever increasing the quality offering to clients and with external acquisition. The stock price evolution of Celanese underlines the strong growth in the chemical industry as the economy restarted following the COVID-19 pandemic.

About Dupont

Dupont is a company created in 2015 after the merger of The Dow Chemical Company (“TDCC”) and E. I. du Pont de Nemours (“EID”). It is one of the largest chemical groups in the world with subsidiaries in 60 countries and manufacturing facilities in 25 countries. Its main products/reporting lines are the following:

- Electronics and industrials: Supplies materials for a broad range of consumer electronics. This is a very specialized segment as it requires capabilities to offer differentiated materials for producers of printing systems, semiconductors for LEDs or OLED screens. Thus, the challenge here is to be able to respond to consumer requests of materials for ever increasing complex products such as flexible screens.

- Water and protection: The goal of this business line is to manufacture products for industries such as workers’ safety, water purification, transportation, and energy. This business segment is known for being the rightsholder of the “Kevlar” brand.

- Mobility and materials: Produces various materials such as thermoplastics, adhesives, silicon encapsulants and films used in transportation, electronics, renewable energies. More precisely, it is comprised of 3 product lines: Advanced Solutions, Performance Resins, and Engineering Polymers. This product line was created in February 2021 by joining multiple activities described as “non-core”, in sign of the future divestment analysed here.

As can be seen below, the investors’ confidence in Dupont is not very strong and the stock price trend is lagging behind other competitors, such as Celanese. One problem of Dupont is that its portfolio of products is less diverse than some competitors, making its margins more dependent on the price of raw materials.

About the industry

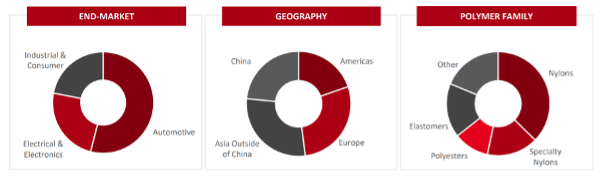

The Mobility & Materials (M&M) product line of Dupont is quite diverse and its main competitors are other diversified chemical conglomerates such as BASF, Celanese, EMS Chemie, Henkel, and Mitsubishi.

Competitors differentiate themselves in 2 ways:

- Intellectual property: Increasing IP capital is crucial as companies operating in that sector are trying to sell differentiated products. In this area, Celanese and Dupont are among the leaders with widely recognised products such as Mylar, Betaseal, Delrin and Tynex for the M&M product line and Clarifoil, Celanex, Polifor, Santoprene and Vectra for Celanese.

- Geographical reach: Both companies sell their products globally but it is to be noted that the M&M product line of Dupont is very strong in Asia (with about half of its sales occurring in this region), Celanese is strong in developed markets such as North America and Europe.

Following the COVID-19 pandemic, the chemical industry has seen strong growth with high customer demands as the economy restarts. Hence, Lori Ryerkerk, the CEO of Celanese declared “The early 2022 order book reflects continued strong demand for our products across most end markets”. However, this industry is very sensitive to the price of upstream raw materials. To preserve margins in an inflationary context, they have to be able to pass on increased cost down the line to its customers by increasing prices.

Deal structure

This is an all-cash acquisition of $11.0bn, financed largely by debt. Thus, DuPont will not be a participant in future synergies that will be generated by this deal. The deal is expected to close during 2022. This deal is not a merger per-se. It is the purchase of a business line of DuPont by Celanese. Celanese negotiated with DuPont for the purchase of some of its products lines that DuPont did not see part of its core business.

The deal involves most of the Mobility & Materials product line of DuPont but some businesses are excluded from the transaction such as Delrin and POM. Together, the business sold is estimated to generate $900m EBITDA pre-synergy in 2022. Thus, this business is valued in this transaction at 12x EBITDA and 2.9x forward sales.

Quite rare in this sector, the preliminary contract states that future liabilities caused by potential chemical damages (known as “PFAS liabilities” for “polyfluoroalkyl substances”) will have to be re-paid by DuPont. Such liabilities have not been rare in the past so PFAS liabilities probably played an important role during negotiations.

Celanese has been advised by Kirkland & Ellis (legal advisor) and Bank of America (financial advisor). Dupont has been advised by Skadden and Arps (legal advisors) and Goldman Sachs (financial advisor).

Deal rationale

The strategic rationale is described through 4 pillars by Celanese:

- Transforming Celanese in a larger, more diversified, and more profitable business. Celanese pinpoints the 23% estimated EBITDA margin of 2022, the diversified geographies of the sales of this business line.

- The complementary product portfolio and Celanese and the M&M division being sold. Very often, the products of the M&M business lines are variant of products existing in Celanese portfolio, creating some potential cross-sales opportunities

- “Enhancement of the commercial and technical capabilities to drive growth”. Through this sentence, we expect Celanese to refer to potential economies of scale, especially in the research activities of plastic production and to new opportunities in the electric vehicles sector unlocked by this merger (the automotive industry is an important client of chemical products).

- Robust synergies expected by Celanese. After the initial execution expected to be achieved in 4 years, cost synergies are expected around $275m-$350m per year and revenue synergies are expected around $125m-$150m per year. In total, the NPV value creation from this acquisition is expected to be positive at “$4bn+”. We find it very optimistic at BSMAC, especially since the market reaction to this announcement has been muted with a decrease in Celanese’s share price of 5%.

Sources: Celanese, DuPont, SeekingAlpha, Bloomberg, IndustrialDistribution, Reuters

Authors: Paul Camincher, Luca Venturelli, Francesco Puricelli, Dietmar del Vecchio, Luca Crippa

You must be logged in to post a comment.