INTRODUCTION

On September 27th, 2022, the Royal Bank of Canada (“RBC”) announced the acquisition of Brewin Dolphin Holdings PLC, a multi-award-winning wealth management organization. The transaction was concluded at a final price of C$2.4 billion (£1.6 billion) on a fully diluted basis, representing 515 pence per share. As part of RBC, Brewin Dolphin will now be identified as “RBC Brewin Dolphin,” and will continue to be managed by CEO Robin Beer.

INDUSTRY OVERVIEW

Primer on the Wealth Management Industry:

Wealth management goes beyond investing, it involves a person’s financial life. Wealth management is the highest level of financial planning services. It generally includes comprehensive investment management alongside financial advice, tax guidance, estate planning and even legal assistance. In fact, many private wealth managers will coordinate with other financial experts — such as accountants or estate planning specialists — on behalf of clients to offer comprehensive financial advice. A wealth manager coordinates the services needed to manage customers’ assets and creates a strategic plan for their present and future needs, such as will and trust services or business succession plans. High-net-worth individuals may benefit from an integrated approach rather than integrating advice and services from separate professionals.

Following the financial crisis of 2008, both individual investors and the wealth managers that support them have had success over the following ten years. Client retention rates are at an all-time high due to larger client portfolios, deeper partnerships, and deeper client interactions. Asset-based fees are now the obvious economic model of choice, with advisor earnings being more closely correlated with client outcomes. Pricing also appears to be finding a new equilibrium despite having been tested recently.

Although the wealth management sector is expanding, several disruptions are increasing in prominence. Even though the pandemic hindered the performance of the wealth management sector for a substantial portion of 2020, the following months have given rise to the hope that the prerequisites for a sizable wave of innovation and experimentation across the wealth management ecosystem are in place. Rapid technology development, rapidly changing consumer needs and habits (driven by the pandemic), and an environment of economic stimulation are some of the factors. The rise of “robo-guidance” in recent years has contributed to raising the awareness of the significance and worth of human financial counsellors. Helping clients manage the anxiety and uncertainty of a worldwide pandemic, that human touch was on full show.

Future dangers and possibilities to advisers are becoming more significant. A protracted market downturn is something that customers have not had to endure during the previous ten years. Client attrition may increase for advisors who have not adequately mentally and financially prepared their customers for this impending reality. Advisers who were opportunistic in seeking out new partnerships outpaced defensive advisors in terms of revenue growth in the years following the 2008 bear market by 12 percent. Also, a hazard and an opportunity are changes in demographics. Client age is a significant organic growth driver from which many advisers are already reaping the rewards. The price structure has stabilised in the short term, but the basic economics of paying with assets is under scrutiny, and there is significant price volatility between transactional and fee-based accounts. Given the growing complexity of client interactions, efficient pricing will require advisers and organisations to consider price at the level of the entire household in the coming years.

Future Trends

The field of wealth management is booming. With a CAGR of 10.7% between 2021 and 2030, the worldwide wealth management business, which was valued at USD 1.25 trillion in 2020, is anticipated to reach USD 3.43 trillion by 2030. According to Bain, the wealth management sector, which combines asset management with financial planning and advice, will grow 67% from $137 trillion in assets under management in 2021 to nearly $230 trillion globally by 2030. Over the same period, it is anticipated that the market for asset management, which focuses more on investments and is already saturated, will rise by less than 40%, from $109 trillion to $152 trillion of assets under management. According to a new report, asset managers and brokerages are swarming into wealth management as “the rich get richer” and a rising tide of young DIY investors receive inheritances.

High net worth individuals (HNWIs) are in high demand, and there is fiercer competition than ever for their business. Businesses must therefore stay current with trends to remain competitive and take a bigger share of this changing market. Growing use of artificial intelligence is one of the market’s emerging trends (AI). Wealth management is one of the first industries in the financial services sector to significantly use AI-based technologies. AI may be applied in many ways to improve efficiency, productivity, and profitability for wealth management businesses, from client acquisition through portfolio management and compliance. The growth of robo-advisor wealth management services is another trend that has seen significant growth in recent years. A robo-advisor, to put it simply, is a category of online wealth management service that provides automated portfolio management. Customers often connect into their accounts and respond to a few inquiries about their financial condition, investment goals, and risk tolerance. Companies have experimented with numerous novel strategies throughout the years to connect with a younger audience. Financial institutions like banks and wealth management firms have been attempting to connect with millennials by customising their offers for this group.

Many millennials have no investing or retirement plans at all, even though this group is predicted to become the world’s largest HNWI section. It’s important to remember that millennials aren’t all the same. While some people are anxious to begin investing, others have less of an interest in doing so. Finally, many more businesses are offering digital-only services because of how deeply technology has permeated our lives. Digital-first businesses are increasingly common in the wealth management sector, and they completely eschew physical locations in favour of providing their services purely through digital channels including the internet and mobile applications.

M&A

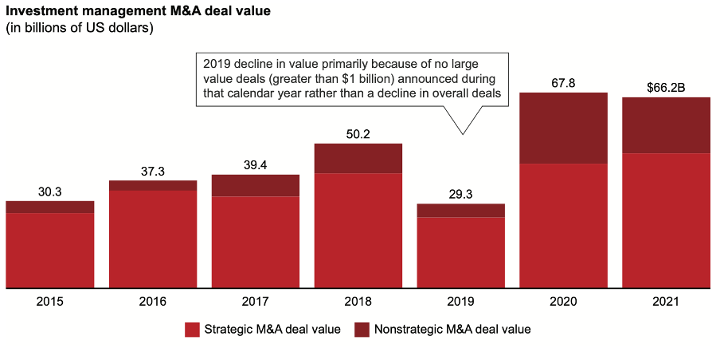

Wealth management M&A activity has seen an acceleration in recent years. In 2020 and 2021, firms set deal value records to produce notable shapeshifting in the industry. Corporations have been using scale and scope deals to stay current with the market. Consolidation brings brand and marketing benefits and the funds needed to engage in large-scale technological advancements. Scale alone isn’t enough for leadership, especially as firms develop through acquisitions.

(Source: Bain)

With the growth of wealth-tech businesses that service emerging and adjacent wealth management industries, scope deals are becoming more crucial. During the first three quarters of 2021, funding for wealth-tech assets increased to a record $12.7 billion, more than doubling the amount invested throughout the entire year of 2020. Increased private equity investment, incumbents’ search for higher growth adjacencies, and technical innovation are key market forces that result in the growth of M&A activity in this sector.

COMPANY OVERVIEWS

RBC

Founded in 1864, with over 89,000 employees and 17 million customers served across 34 countries, RBC is one of the Canada’s biggest banks, and among the largest in the world based on market cap.

Although RBC primarily functions as a commercial bank, it operates through 5 business units:

- Personal and Commercial Bank, which consists of retail investment services and personal banking operations.

- Wealth Management, which offers a broad range of investment, trust, and other wealth management solutions to wealthy, high-net-worth, and ultra-high-net-worth customers.

- Investor & Treasury Services, which caters to the requirements of institutional investors and offers custodial, advising, financing, and other services for customers to protect assets, maximize liquidity, and manage risk worldwide.

- Capital markets, which offers a broad variety of capital markets products and services across our two main business lines, Corporate and Investment Banking and Global Markets, to public and private enterprises, institutional investors, governments, and central banks internationally.

- Insurance, which provides several life, health, home, vehicle, travel, wealth, and reinsurance counseling services.

The business reported $45.24 billion in yearly revenues and a net profit of $13 billion in 2021. Nonetheless, unlike many European banks whose quarterly earnings soared thanks to rising interest rates, the unfavorable changes in the macroeconomic environment highly impacted RBC’s earnings. Due to lower earnings in the insurance, personal & commercial banking, and capital markets segments, as well as higher salaries, technology investments, and discretionary costs to support strong client-driven growth, they reported a net income of $3.6 billion for the quarter that ended on July 31, 2022, a 17% decrease from the prior year.

The most negatively impacted business unit, Capital Markets, saw its earnings fall by 58% from a year ago. This was primarily because of the impact of loan underwriting markdowns in the United States, releases of provisions on performing loans from the previous year, a decline in the origination of debt and equity, and a decline in loan syndication activity.

Brewin Dolphin

Founded in 1762, with over 30 offices throughout the UK, Jersey and Ireland, and about 2,000 employees, Brewin Dolphin is one of the largest wealth management firms in Britain. The company now serves three different sorts of clients: direct discretionary clients, indirect clients, and organizations. It has around £51.7 billion in AUM (Q3 2022).

Brewin Dolphin supports its direct discretionary customers throughout their lives by offering a variety of options, including:

- Brewin Portfolio Service, a ready-made investment service available to those who may be new to investing.

- 1762 from RBC Brewin Dolphin, an exclusive service for wealthy individuals with complicated demands who require professional guidance

- WealthPilot, a simplified financial planning advisory solution for those with simple needs

- Wealth management, core service that aims to maximize the value of the assets customers have already amassed.

Through a network of intermediary partners, they give indirect customers access to their investment management expertise. Moreover, they also offer services to charities and corporations.

The overall revenue for Brewin Dolphin thus far this year was £307.4 million, up 1.2% from the previous year. However, Brewin Dolphin’s companies were badly impacted by the volatile market we saw throughout the third quarter of 2022. They recorded a net income of £97.9 million, a 5.7% drop from the previous year due to worse market performance. As a result, their total funds fell by 8.2% to £51.7 billion during the quarter.

DEAL RATIONALE

RBC is strategically focused on growing its wealth management branch in their main markets, Canada, the United States and the UK. The acquisition of Brewin Dolphin, then, enables RBC to combine RBC WMI (its existing wealth business in the UK) with Brewin Dolphin to create the third biggest wealth manager in the region, with £64 billion of assets under management.

RBC is interested in the revenue synergies that the acquisition can bring by integrating its banking products. By owning Brewin Dolphin, RBC is transferring more than 80,000 clients across the wealth spectrum, including high and ultra-high net worth clients, to its portfolio, which will now have a relationship with the bank and might need other financial services or products in the future, which RBC can directly provide. This deal comes at a time where the wealth management industry in the UK is seeing great consolidation, as capturing these high-net-worth clients is very valuable for banks to enable them the cross-selling of products. In the words of Doug Guzman, head of RBC Wealth Management, “The UK business is only partway along the modernization path that North America is. There’s lots more work to do on digital, there’s lots more work to do integrating banking products in the interests of clients.” This new trend in the banking sector follows the business model of other multi-division banks with a strong wealth management presence, such as UBS.

Along with revenue synergies, RBC has identified various cost synergies that will arise from the acquisition, mainly in the back office of the bank: from overlapping functional and administrative areas to departments related to Brewin Dolphin being a publicly listed company (as RBC will be the sole owner of Brewin, it will be delisted from the stock exchange). Additionally, its executives remark the value of the prior investments in innovation and technology that Brewin Dolphin has been making for years, which can bring them greater operational efficiencies by increasing advisor capacity and client experience.

Furthermore, according to the ‘Scheme Document’ of the acquisition, the background, and reasons for the transaction from the perspective of both parties were stated as follows:

“RBC is strategically focused on evaluating opportunities to grow its wealth management operations in its core markets, namely Canada, the United States and Europe. The acquisition of Brewin Dolphin represents an exciting strategic opportunity for RBC to combine Royal Bank of Canada Wealth Management International (“RBC WMI”), its existing wealth business in the UK and the Channel Islands, with Brewin Dolphin to create a market leader with, on a pro-forma basis, £64 billion of assets under management (“AuM”), a combined annual revenue of £545 million for FY2021 and approximately 600 client facing professionals as at 31 December 2021. The Acquisition is transformational to RBC WMI in the UK, Ireland and Channel Islands and establishes an attractive platform for further growth. Following the Acquisition, RBC Wealth Management (“RBC WM”) will have a leadership position in the UK and North America. RBC highly values Brewin Dolphin’s position as a market leading advice focused wealth manager in the UK and Ireland with a longstanding record of delivering superior client service. RBC is also attracted to Brewin Dolphin’s position within the broader UK wealth sector as one of the foremost asset gatherers in a secular growth and consolidating market and its robust investment performance. RBC will combine the strengths of RBC and Brewin Dolphin, provide additional investment and leverage its global capabilities and banking expertise to extend the range of products and services available to meet clients’ needs at any point in their lives from bespoke to digitally enabled service delivery. RBC is confident that the excellent strategic fit is supported by complementary client-centric cultures and aligned values that will create an enhanced platform, delivering benefits from increased scale and accelerated growth opportunities to all stakeholders. Both businesses place a strong emphasis on integrity and behaviours which support a good organisational culture. The application of these cultural attributes will be key to the continued enhancement of the client and employee propositions.”

“The Brewin Dolphin Directors remain highly confident that the ongoing execution of Brewin Dolphin’s strategy will continue to deliver sustainable growth in the attractive UK and Ireland wealth management markets and create shareholder value. However, the Brewin Dolphin Directors recognise that the Acquisition provides Shareholders with a compelling value proposition. At 515 pence per share, the Acquisition represents a highly attractive 62% premium to the price of Brewin Dolphin Shares on 30 March 2022, being the Business Day prior to the Rule 2.7 Announcement, and a material premium to historical trading ranges of Brewin Dolphin’s Shares. Being satisfied in cash, the Brewin Dolphin Directors recognise that the Acquisition provides Shareholders with an immediate and certain value that would otherwise be realised over time and subject to inherent risks, including an uncertain macroeconomic and market environment.

As one of the largest global financial institutions, RBC represents a high quality and stable owner of Brewin Dolphin, with significant financial and intellectual resources providing opportunities for further investment in Brewin Dolphin. As a result, the Brewin Dolphin Directors believe that the delivery of Brewin Dolphin’s strategy will be accelerated under the ownership of RBC. Brewin Dolphin’s Directors see opportunities for additional growth through product diversification, the potential to accelerate Brewin Dolphin’s digital development through access to RBC’s broader systems, capabilities and network and the expansion of Brewin Dolphin’s distribution channels through leveraging RBC’s global presence.”

RBC’s choice of the UK for expansion has to do with Brewin Dolphin’s recent business performance. Net inflows of £1bn in the final three months of 2021 were the group’s best ever. Net inflows have averaged 3.5 per cent of AUM over the past three years, about double the growth at Rathbones. RBC clearly likes what it sees, paying the equivalent of 2.8 per cent of AUM or 22 times next year’s earnings. Based on the AUMs of Rathbones and Quilter, similar ratios would suggest values 70 per cent and 50 per cent higher, respectively, from their current share prices. Consolidation reflects the pressure on fees felt across the wider asset management sector. Brewin Dolphin’s revenues as a share of AUM have declined by 32 basis points over the past decade to 0.78 per cent in the latest financial year. The backing of a larger parent bank could provide a sturdier backstop for the combined wealth managers. RBC could achieve cost savings of between 20 and 30 per cent of overheads based on previous deals in the sector. Brewin Dolphin had already begun cost-cutting efforts to stem margin erosion. Pre-tax margins of 22.4 per cent last year have shed 2 percentage points in the past two years. RBC will need more than cost-cutting to get the most out of its purchase. It will need to maintain performance and retain staff. Brewin Dolphin shareholders should be happy with their own newfound wealth.

DEAL STRUCTURE

The deal was announced on 31st March 2022. RBC Wealth Management (Jersey) Holdings Limited (“Bidco”), a wholly owned subsidiary of RBC, had, had announced its recommended cash offer for the entire issued and to be issued share capital of Brewin Dolphin for 515 pence per share. According the Scheme Document on the RBC Investor Relations website, the Acquisition values the entire issued and to be issued share capital of Brewin Dolphin at approximately £1.6 billion on a fully diluted basis, and represents a premium of approximately:

- 62 per cent. to the Closing Price of 318.0 pence per Brewin Dolphin Share on 30 March 2022 (being the last Business Day before the commencement of the Offer Period); and

- 54 per cent. to the six-month volume weighted average price of 333.7 pence per Brewin Dolphin Share to 30 March 2022 (being the last Business Day before the commencement of the Offer Period).

The value placed by the Acquisition on the existing issued and to be issued share capital of Brewin Dolphin on a fully diluted basis is based upon 303,728,512 Brewin Dolphin Shares in issue. Included within this number is:

- 12,099,963 Brewin Dolphin Shares held by the Brewin Dolphin Employee Share Ownership Trust which are expected to be used to satisfy awards under the Brewin Dolphin DPSP, Brewin Dolphin LTPP and the Brewin Dolphin EAP; and

- 3,099,697 Brewin Dolphin Shares held in the Brewin Dolphin Holdings Share Incentive Plan Trust of which 3,098,671 Brewin Dolphin Shares are held on behalf of participants in the Brewin Dolphin SIP.

Furthermore, the Scheme Document stated that “if any dividend, distribution or other return of capital or value were announced, declared, or paid in respect of Brewin Dolphin Shares on or after the date of the Rule 2.7 Announcement and before the Effective Date, the Bidco reserved the right to reduce the Acquisition Price by the amount of any such dividend, distribution or other return of capital or value. If Bidco exercised its right to reduce the Acquisition Price by all or part of the amount of any dividend, distribution or other return of capital or value referred to above, Scheme Shareholders would be entitled to receive and retain such dividend, distribution or other return of capital or value.”

The deal was completed on 27th September 2022. Brewin Dolphin has now become a wholly owned direct subsidiary of the Bidco, and its shares have been delisted from the London Stock Exchange. Brewin Dolphin has a post-deal implied Enterprise Value of approximately £1.44bn, with a post-deal valuation of approximately £1.6 billion. It is now registered as a private limited company post its delisting, in accordance with the UK Companies Act.

Sources: Financial Times, RBC Investor Relations, Brewin Dolphin Investor Relations, Pitchbook, Private Banker International, Financial Post, Financial Express, McKinsey, Bain

Authors: Akshay Shrivastava, Maddalena Salterini, Enrique Rivero Vorokova, Andrea Zenoniani

You must be logged in to post a comment.