Introduction

In 2021, a market like no other, Cimarex Energy and Cabot Oil & Gas Corp decided to merge into a $17 billion company. Despite the expected downsides, the advisors convinced the managements to proceed with the all-stock merger of equals because the stability given by the balance of oil and gas would outweigh any drawback. Indeed, the companies believed in it, the shareholders voted towards it and Coterra was created.

Company OVERVIEW

Climax Energy

Cimarex Energy was founded in 2002 and it was based in Denver, Colorado. During the years, the company experienced horizontal integration acquiring competitors such as Magnum Hunter Resources ($2.1 billion), Chesapeake Energy ($294 million) and Resolute Energy ($1.6 billion). In 2020, Cimarex’s revenue was $1.558 billion but despite continually striving to maximize cash flow from operating activity, the latter was declining since 2018, going from $1.551 billion in 2018 to $1.344 billion in 2019 and $904 million in 2020. Even though this downturn might look scary, Cimarex actually handled the pandemic very well by “saving costs everywhere they could without sacrificing safety” and, at the same time, aiming at returning cash to shareholders with dividends.

Cabot Oil & Gas Corp

Cabot Oil & Gas Corporation was an independent oil and gas company focused mainly in the United States, with headquarters in Houston, Texas. Cabot, similarly to Cimarex, sustained a large and substantial acquisition when in 1994 they acquired Washington Energy Resources for $180 million. Overall, Cabot is a medium-sized energy company characterized by 303 employees and with a $1.5B annual revenue for 2020. A main advantage on its competitors is the unusually diverse demographic backgrounds and the above average employee retention (3.8 years). Uniformly with the industry, Cabot Oil & Gas Corp. revenues declined since 2018, with a fall of 5.57% to 2019 and 29.02% from 2019 to 2020

Industry Overview

2020 was marked by an unprecedented collapse in demand for oil spurred by the Covid 19 crisis. Rapid changes in behaviour during the pandemic and increasing pressure of governments towards achieving low-carbon future caused a downward shift in the expectations for future oil demand. Oil was the worst-performing commodity, falling behind even coal.

Traditionally, investments in the O&G industry follow oil prices. This trend was observed throughout recent years, until the oil price crash of 2020, which also slumped the O&G investment activity. However, both O&G capex and M&A decoupled from oil prices in 2021, largely due to a growing consensus that the long-term demand for hydrocarbons will follow a bearish trend.

The speed of the recovery of demand for oil was uncertain as the gasoline and aviation fuels demand was expected not to return to 2019 levels. The main reasons are: efficiency gains, shift to electric vehicles, and jet fuel demand expected to stay below 75% of the pre-pandemic levels. The O&G industry accelerated its energy transition during the pandemic, and many giants like BP and Shell doubled down on their net-zero goals. Coterra projected a 42% decrease in their greenhouse gas emissions intensity by 2022. 2021 saw a rebound of oil and gas prices, and earnings, in the fourth quarter. It was a year marked by good financial health for the oil and gas market, after the pandemic years. Time will tell how companies will respond to the new post-pandemic world. In 2022, especially after the start of the war between Russia and Ukraine, the oil and gas market seems as risky as ever. It has always been a highly volatile market, with constant up and downs, due to political, social and environmental factors, but 2022 increased the stakes and made it an even bigger challenge.

Deal Rationale

On May 24 2021 Cabot Oil & Gas Corp (COG.N) and Cimarex Energy Co (XEC.N) agreed a merger of equals to create a wide oil and gas firm, with an Enterprise Value of $17B. The deal was first seen as a “surprise” given the recent trend of US shale producers to focus on a single geography to optimize cost savings and attract investors. Because of that, some analysts expressed concern about the deal. The fear was that Cimarex would have been transformed in a gas producer and so it will not benefit from the rising oil prices. This partially explain an offer premium of less than 1%. However, the benefits of the merger compensated these risks. On September, Glass Lewis advisor recommended that shareholders of both companies to vote to support the merger: having a balance of both oil and gas production would benefit both Cabot and Cimarex, providing a more stable outlook for its financial performance. They predict that the deal will generate the same financial objectives as recent Exploration and Production deals. With Cabot’s approximately 173,000 net acres in the Marcellus Shale and Cimarex’s approximately 560,000 net acres in the Permian and Anadarko basins, the combined business will have a multi-decade inventory of high-return development locations in the premier oil and natural gas basins in the United States. In the environment in which the two companies operate, upstream companies must deal with significance challenges in finding and maintaining investor and clients.

Additionally, among the top 35 U.S independent upstream companies, the only ones which are able to maintain key investor metrics (showed below) are combined entities.

- Free cash flow yield plus annual production growth of greater than 10%.

- Reinvestment ratio of less than 60%.

- Net debt/EBITDA of less than 1.0x.

- Three-year cumulative free cash flow of greater than 30% of market capitalization.

- Market capitalization greater than $10 billion.

Therefore, the merger will bring together Cabot’s extensive gas resources in the US northeast and Cimarex’s oil-heavy acres in West Texas, creating a diversified energy leader company aimed to achieve more flexibility between those two assets that will be able to achieve the metrics shows upper. The Board of Directors of the two companies believe that the transaction will generate different synergies:

- The deal will create a financially strong and diversified energy company, capable of generating long-term value and delivering sustainable returns for the stockholders. High-quality assets and diversification will generate a cumulative free cash flow of $4.7 billion from 2022 to 2024.

- The company will be able to enhance the return of capital to shareholders by multi-faced program which will offer a base dividend of $0,5 per stock per quarter (2,8% dividend yeald) and plans to achieve a 50% return of quarterly free cash flow in the future years.

- The merge of the two entities will also increase the already strong financial position and capital structure of the two stand-alone entities by reducing at the minimum the near-term debt and the overall cost of capital.

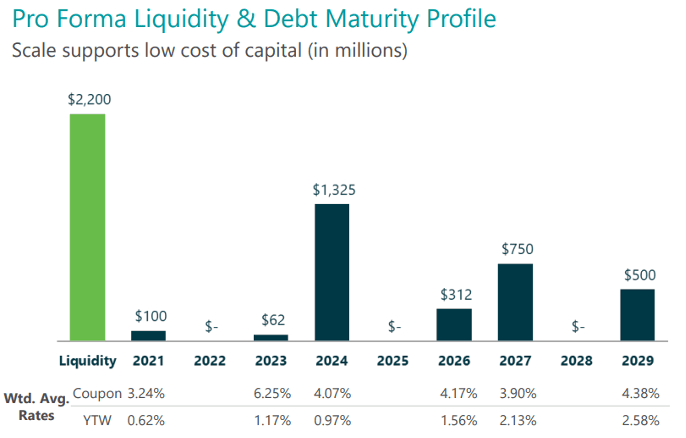

After the conclusion of the deal, the companied business will have a pro forma liquidity of 2.2 billion of dollar and a target pay-out ratio (net-debt to EBITDA) of around 1.0x. Due to the increase in the quality of debt and capital structure the company hope to generate a cost synergy of around $100 million in less than 18 months. Looking to a more detailed analysis, those financial synergies will be more valuable for Cimarex, as the financial risks of remaining a stand-alone due to the high volatility of its cashflows and high cost of capital are higher comparing to the one of the combined businesses. Cabot and Cimarex will also benefit of the share commitments to the environment stewardship; therefore the combined business will enhance the already strong attention to ESG risks and programs and is expected to show satisfying metrics to SASB and TCFD standards.

Deal Structure

The deal is an all-stock merger of equals. The companies said more than 99% of Cabot common shareholders and more than 90% of Cimarex shareholders voted in favour of the merger. Merger of equals are the prefect field for looking at complementarity. The idea is to create and make something big and relevant. The main problem in this kind of merger is that the governance become more complex (risk of stalemate on crucial decisions) and there is the risk that the two companies’ culture does not fit. The new company Coterra will be led by Chief Executive Thomas Jorden, who was formerly the CEO of Cimarex. Scott Schroeder, previously Cabot’s chief financial officer, will take the role at Coterra. The new company board will have 10 members, with equal representation from Cabot and Cimarex. The board includes Chairman Dinges and CEO Jorden. It is a forward merger (Cabot will absorb Cimarex) but the company decided to change its name to Coterra. It will still be listed on the NYSE but with a new ticker (CTRA). Term of the agreement:

- Cimarex shareholders will receive 0146 shares of Cabot common stock for each share of Cimarex common stock owned. They will own approximately 50,5% of the new company.

- Cabot shareholders will own approximately 5%

- Implied equity value of $7.4 billion, or $71.50 per Cimarex share, the deal reflects a less than 1% premium.

- 0,50$ per share as dividend as soon as the deal closes

Conclusion

In conclusion, the operation will merge two company which will provide geographic, asset and commodity-specific cycles diversifications which should increase the resiliency to market fluctuations and other macro factor which could impact any single business area of the two stand-alone companies. Thanks to the high talented and qualified operating management of Cabot and Cimarex, the new company will more than maintain all the previous projects and level of production of the two stand-alone companies by generating additional synergies through the development of collaboration and increase in the operating efficiency. Example of these are the reduction of supply and technical costs and the increase in production and sales. According to the management all of this will lead the company to become a leader in the field.

Sources: Reuters, Financial Times, Bloomberg, Statista, Cabot Oil and Gas financial statements, Cabot oil and gas website, Cimarex financial statements, Cimarex website, Coterra energy press release

Authors: Aldo Falco, Georg Giulini, Stefano Vione, Gabija Verbaite, Chiara Belmonte, Alessandro Monticone

You must be logged in to post a comment.