Orange and MásMóvil, two leading telecom groups in the Spanish markeT

Orange is a telecom group with over 120 years of history. It is the 8th largest global telecoms brand with over 5000 stores globally and an extensive network in Europe, the Middle East, and Africa, with a significant presence in France, Belgium, Spain, and Morocco. Orange’s business covers telecom services and infrastructures, relying on a network of 40,000 mobile towers in Europe and over 450,000km of submarine cables worldwide. The company operates in the fields of:

- Wholesale telecom (fixed and mobile connectivity, interconnections, and infrastructure solutions),

- Cybersecurity (secured data storage, attack monitoring, and security auditing),

- Financial services (Orange Bank, Orange Africa, and Orange Money),

- Medias (Orange Studios and OCS)

MásMóvil Group is one of the leading telecommunication groups in Spain founded in 2006, the company encompasses services and infrastructures. The company’s fixed network can reach 18 million homes with ADSL and over 26.8 million houses with fiber, covering 98.5% of Spain’s population. In 2016, the Group performed several notable acquisitions, including Pepephone and Yoiho, thus consolidating its position as the fourth-largest telecommunications operator in Spain. The Group continued its expansion in 2017 by purchasing Llamaya, a virtual mobile network operator offering prepaid services to the ethnic market segment. MásMóvil was a public company listed on Spanish Alternative Stock Market back in 2012 but went through a first leveraged buyout by three private equity funds: Cinven, KKR, and Providence Equity Partners.

European Telecom, a market highly fragmented

For the last decades, the global telecom market has been exceptionally dynamic. It grew from $2,642 bn in 2021 to $2,879 bn in 2022 at a compound annual growth rate (CAGR) of 9.0%. In recent months, the Russia-Ukraine war has disrupted the chances of global economic recovery from the COVID-19 pandemic and has dented the growth of the global telecommunications market. Consequently, in the coming years, the sector’s growth is expected to slow to a CAGR of 6.0% and reach $3,629 bn in 2026.

The Telecommunication sector is divided into two subsegments: Telecom Equipment (the largest) and Telecom Services. In recent years, Telecom Equipment, which includes towers, has particularly attracted the scrutiny of infrastructure funds in search of a high return on investment. Other Equipment encompasses fiber-optic cables (including submarine cables), routers, and traditional copper-based ADSL networks. Telecom services instead focus on the final consumer, providing fixed-and mobile network services, data, Internet, and voice. Although Telecom Services is a crucial industry segment, it has lower returns due to the competitive environment and price war between service providers.

Shifting the focus to the European continent, the European Union constitutes a competitive and highly fragmented market. A critical data that sustains the latter affirmation is the number of providers per country, which amounts to 4 in most countries. In addition, we can add that each European country has its distinct telecom market with its specific regulation, frequency standard, and attribution process. Consequently, there is currently no real cross-border consolidation in the sector in Europe. The only players that have demonstrated an actual capacity to scale up and effectively develop their activities in several countries of the continent are Vodafone, Deutsche Telecom, Orange, and Iliad. In contrast, the market is highly concentrated in the United States over three nationwide operators: AT&T, Verizon, and T-Mobile, which share a need of 330 million people.

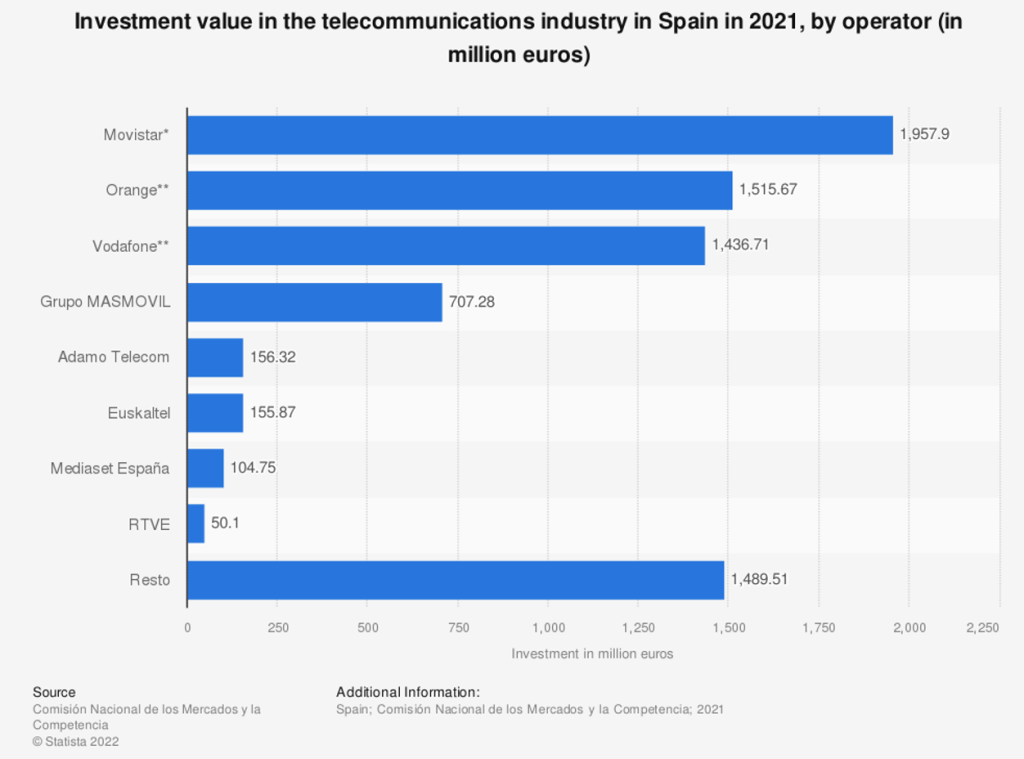

In the chart below are expressed the leading providers in the EMEA region by revenues in December 2021:

The Orange-MásMóvil deal, a transforming operation in the Spanish market

The merger between Orange’s Spanish activities and MásMóvil fits into the current consolidation trend within the European telecommunications sector. This movement result from the current market conditions faced by providers, which face low profitability, price war, and essential investments for the deployment of 5G and fiber networks. This transaction may also dramatically transform the market equilibrium and the long-term dynamics in Spain. Thus, observing the reshuffling of market share will be interesting if competition authorities approve the merger.

Historically, Telefonica, the former state monopoly, had dominated the Spanish market with a prominent infrastructure and commercial position. Currently, the market is shared between an oligopoly constituted by four companies: Telefonica, Orange, Vodafone, and MásMóvil, which own respectively 28.24%, 22.91%, 22.26%, and 20.55% of the market shares.

Primarily, the Orange-MásMóvil deal aims at creating a player better equipped for the intense competition in the Spanish telecommunications and broadband sector. If the regulator approves, the merger will create a giant in Spain, controlling over 40% of the telecom market in the country. This new dominant position could allow the company to perform cost synergies, decrease its investments in new infrastructure and benefit from reduced competitive pressure. In particular, the operation would allow the new Group to accelerate its investments in 5G and assemble the two leading FTTH networks into the new company.

Orange and MásMóvil CEOs are optimistic that antitrust and all other relevant authorities will give their green light for a deal that would represent “an important step in the development of Spanish telecommunications infrastructure and innovation, benefitting customers across the country.”

The combined entity would generate more than €7.3 Bn in revenue and more than €2.2 Bn in core operating profits per year. In addition, Orange expects the combined entity to benefit from synergies amounting to €450 m per annum, four years after the deal’s completion. Consequently, Orange group could benefit from this operation, which may help the French group to consolidate its position in a country in which it struggled to differentiate itself from its competitors in recent years.

A combination that may liberate significant financial margins for Orange

The merger between the two companies values the combined entity at €18.6 Bn with respectively €10.9 Bn for MásMóvil and €7.8 Bn for Orange Spain. The entity’s equity distribution and controlling power will be distributed evenly between the two companies’ shareholders. A €6.6 Bn debt package from a large syndicate composed of international banks will support the transaction.

The operation also includes a €5.85 Bn euros payment to the current shareholders of Orange Group and MásMóvil, with €4.2 Bn going to Orange. The asymmetric distribution favoring Orange reflects the higher indebtedness level of MásMóvil and the difference in the two operators’ infrastructure size. According to Orange executives’, the operation also allows a deleveraging of the combined entity with a target 3.5x net debt/EBITDA ratio.

The deal also includes a 2-year stock lock-up period after the merger to prevent Orange and MásMóvil from selling their shares. At the end of the two years, Orange has the option to take control of the combined entity. In the long term, this deal also opens an opportunity for performing a potential future IPO in the coming years. This operation could offer an exit opportunity for the funds while allowing Orange to maintain significant control over its Spanish subsidiary.

Orange, a group in the middle of a strategic transformation

This deal arises at a strategic time for Orange, which is currently getting through a historical transformation and profound changes in its governance. The company has recently appointed Christel Heydemann as the new CEO in April 2022. This nomination follows the resignation of its former emblematic leader, Stephane Richard, condemned by French justice following the arbitrage of the Tapie affair.

The new CEO has since started a strategic review of the operator’s activity to improve Orange’s profitability and satisfy the exigences of the financial markets and the French state (which currently owns 23% of the telecom company). The company has notably unveiled that it will focus on its Telecom Provider and Cybersecurity activities. On the contrary, the company also announced that it would reduce its investments in its activities in the Financial Services and Media sectors. This strategy places Orange at the center of attention in the M&A market both as a buy-side and sell-side player. In the following paragraph, we will discuss the implications of this new strategy for Orange in its different markets.

In the Retail Market, Orange has already consolidated its assets in Belgium by increasing its participation in its Belgian subsidiary to 77% in May 2021. The same year, the company agreed with Nethys to acquire 75% of VOO, valuing the company at €1.8 billion for 100% of the capital. This purchase allows the company to become a more significant player in the Belgian market by expanding its triple-play and quadruple-play offers, leveraging on new synergies. In the coming years, further acquisitions may also be performed in several European countries to support the company’s expansionist ambitions.

In the Cybersecurity segment, the French provider is also a major player on the European continent thanks to its “Cyberdefense” division. This year, Orange has acquired the two Swiss companies SCRT and Telsys for an undisclosed amount to strengthen its position in the Swiss and German markets. In the future, Orange could become one of the leaders and a consolidator of the fragmented European cybersecurity market. The company is presented in France as a potential bidder for acquiring Atos’ cybersecurity division. However, Orange is still a medium-sized player in the cybersecurity segment which is a highly fragmented market.

On the media sector, Orange has entered talks with Canal+ Group to sell its OCS on-subscription activities and Orange Studios’ production capabilities. The final purchasing agreement, as well as the terms of the cession, are expected to be made public during the first semester of 2023. However, the session should be realized on low multiples, given that the division is currently not profitable and that the distribution agreement of HBO’s catalog of series will expire by the end of 2022.

On financial services activities, Orange has engaged in multiple talks with several traditional incumbent banks to sell its financial division partially or entirely, but all attempts have failed. In recent weeks, rumors have intensified about Cerberus’ interest in acquiring Orange Bank. According to “Les Echos,” the American found that previously bought the French retail activities of HSBC would be willing to pay as much as €1.6 Bn to acquire the digital bank.

The consequences of Orange’s new strategy

It remains unsure whether implementing the new strategy will allow the group to restore its financials and improve its performance in its core markets. In fact, Orange is facing intense competition in its traditional retail telecom market in Europe and particularly France, and Poland. The company is also suffering in the African markets where continental leaders are emerging. The dominant groups on the continent include MTN, Airtel, Vodacom/Vodafone, Gio mobile, and Econet.

However, it appears clear that the new activities developed during the last decade in the media and financial services sectors have both failed to reach profitability. The potential divestiture could help the group cut unprofitable divisions and support the development of the new company’s core activities. Also, the MásMóvil deal represents a significant opportunity for the Group both in the short and long term. In case of success, Orange could use the €4.2 Bn of proceeds to finance new investments. In the future, the combined entity’s potential IPO may also generate additional cash flows to strengthen the group’s financials. Overall, Orange can also rely on its robust propriety infrastructure to guarantee its development. In fact, the group is one of the last European telecom providers controlling its tower and owning its network of submarine cables.

A deal that may initiate a wave of consolidation in Europe.

This deal is also crucial for the European telecom landscape. In fact, the operation is inscribed in the context of the evolution of EU antitrust regulation. Whereas in the past decades, the European Commission has strongly advocated for intense competition to benefit the customers, the doctrine is progressively evolving towards more consolidation in order to allow the emergence of more substantial European companies. The pivot engaged aims to ease infrastructure investments and enable faster deployment of 5G and optic fiber networks. According to market analysts, this deal could pave the way for similar operations to reduce the number of operators from 4 to 3 in other countries such as Italy, France, or Portugal. Several other deals are under review by the European Commission, including the acquisition of 75% of the Belgian operator VOO by Orange Belgium.

In the future, we can estimate that growing consolidation in the European telecom provider landscape can help to create synergies between companies to lower costs, concentrate assets in equipment, and increase the sector’s profitability.

Source: Orange, MásMóvil, Bloomberg, Reuters, FitchRatings, Statista, European Parliament, Yahoo Finance, Les Echos

Authors: Kurt Niklfeld, Meriç Çavuş, Stefano Leone, Yuxi Cheng, Paul THIRIOT

You must be logged in to post a comment.