The luxury fashion industry has experienced impressive changes in the past four decades: numerous firms were formed, and a substantially harder competitive landscape arose. Consolidation also played a crucial role in this phenomenon. This article focuses on the causes and consequences of the consolidation trends in the luxury fashion industry, and the evaluation of the industry’s independent brands attractiveness, amongst others, through specific case studies.

A consolidating industry

Already in the 1900s, there were consolidation merger waves in the mining and manufacturing sectors. Ever since, this consolidation trend has become almost a standard phase in the life cycle of industries and moves from industry to industry. Consolidation can be seen as either the process of making a position of power stronger to ensure its existence or the process of joining two things together into one. In M&A, it relates to the latter, the union of smaller companies into one larger company. There are various factors driving companies to pursue consolidation. Corporations may use M&A to gain size and scale (especially common in mature markets), enhance operational efficiency, and penetrate new markets. Secondary benefits of gaining size and scale include improved access to capital and increased pricing power. Moreover, consolidation is also driven by the desire of firms to attain access to certain capabilities and competencies that they are unable to readily develop.

Consolidation is likewise a trend evident amongst luxury fashion brands. Since the mid-1980s, numerous luxury fashion brands have increased M&A expenditures to expand and boost competitiveness. This has caused an increase in concentration in the luxury fashion industry year after year, particularly in Europe. M&A activity even more than quadrupled in the two decades after 2000. LVMH, Kering, Richemond, and Michael Kors are examples of luxury fashion brands that have made the most significant and expensive acquisitions in the last twenty years, developing diversified portfolios to strengthen their market position. Amongst the most valuable acquisitions were Kering’s acquisition of a 42% stake in Gucci Group for c. EUR 2.7bn in 1999, the Arnault family’s acquisition of Christian Dior for c. EUR 12bn in 2017, and Michael Kors’ acquisition of Versace for c. EUR 1.8bn in 2018. Such transactions have enabled LVMH, Kering, and other consolidators to attain brands across luxury industries, ranging from wine and jewellery to fashion, allowing them to attain a strong foothold in the luxury industry. This consolidation has in turn resulted in a more and more oligopolistic luxury industry.

Figure 1. Main conglomerates with key brands

Teaming up is attractive for the luxury conglomerates but also for the independent brands. The large luxury conglomerates continue to buy luxury fashion brands with strong reputations, assets, and a well-defined history to expand their luxury empire. The conglomerates offer luxury brands significant financial resources to advertise their brand and materialise their ideas globally. Moreover, acquisitions by conglomerates generally preserve the brand’s creative independence and identity while adding centralised support functions (e.g., IT and finance) and initiatives (e.g., sustainability).

Deloitte’s “Fashion Luxury Private Equity and Investors Survey 2022” report underlines this drive for consolidation in the luxury market as well as investors’ increased interest in the sector. Overall, 284 luxury M&A deals were documented in 2021, with 156 personal luxury goods deals – 22 deals more than in 2020. As the graph shows (Graph 1), most of these personal luxury good deals are Apparel & Accessories related, accounting for 88 deals in 2021. Compared to prior years, the characteristics of M&A activity in this market have changed. In the last year alone, the average deal value in the luxury market has increased by 667%, with the Apparel & Accessories sector showing an increase of 428%. This is coherent with the notion that due to the consolidation process the companies left for sale increase in size and value. This is also confirmed by the fact that we see a 10% increase in large and medium sized targets while the small sized ones decreased by 7%.

Graph 1. Number of deals in 2021 – breakdown by sector

Source: Deloitte, Fashion Luxury Private Equity and Investors Survey 2022

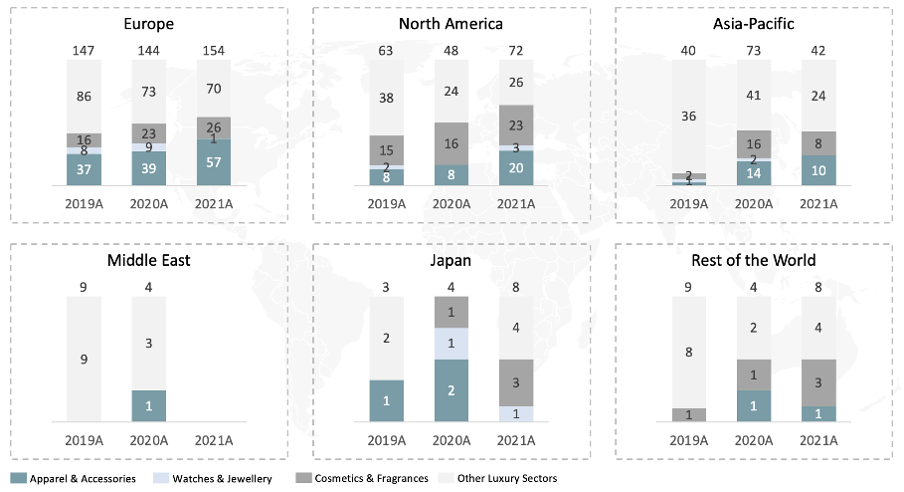

Considering the geographical luxury market split, most transactions have annually taken place in Europe. In 2021, 154 transactions were registered in Europe compared to 72 transactions in North America. North America showed the highest increase in transactions, registering an increase of 24 deals (Graph 2). Both in Europe and North America, the highest growing subsector is the apparel and accessories sector, demonstrating the growing interest in the subsector and the ongoing consolidation activities.

Graph 2. Overview of the luxury sector deals from 2019 to 2021

Source: Deloitte, Fashion Luxury Private Equity and Investors Survey 2022

The macro-economy at play

To understand the luxury fashion M&A landscape, it is crucial to analyse the macro-economic conditions and its impact on the industry. Because high income consumers are less impacted by economic downturns than other individuals, luxury is often perceived as immune to recessions. Companies with some of the most high-end products, including LVMH and Kering have therefore reported strong sales in their last quarterly reports, with substantial year-on-year improvements. However, rising inflation, interest rate hikes, and uncertainty still have a considerable impact on luxury fashion M&A.

A critical economic index that needs to be examined to comprehend M&A trends is inflation, which reached a 40-year high in the US and in the UK in the past few months. Its main drivers include supply chain bottlenecks due to COVID-19 lockdowns, and soaring food and energy prices, in part due to the Russian invasion of Ukraine. Therefore, companies’ operating costs have drastically risen, margins have fallen, and M&A markets tend to exhibit significantly lower purchase prices. However, as luxury fashion revenues are resilient to increases in operating costs, the effect of inflation on this industry’s M&A activity is limited, according to a 2022 Bain & Company study. Yet, inflation can be argued to have non-negligible indirect consequences on the luxury fashion companies’ attractivity for both financial sponsors and strategic buyers.

Another factor to be considered is interest rates. Interest rate hikes are considered to be inflation’s most consequential indirect effect. Both the FED and the ECB have considerably adjusted monetary policies to keep inflation expectations in line with their target of 2%, as explained by Fabio Panetta, member of the Executive Board of the ECB. This increases the cost of borrowing and makes it more difficult for investors to meet their desired internal rate of return, making deals more difficult to execute. While the luxury fashion sector is less susceptible to the direct effects of inflation than other sectors, luxury fashion is not insensitive to these indirect effects. As such, various experts, including PwC, expect luxury fashion M&A activity to suffer from interest rate hikes and from the bear market in 2022 and possibly in 2023 as well.

Current state of the luxury fashion industry: how are independent brands succeeding

The luxury fashion industry is currently dominated by conglomerates. Its three biggest players, LVMH, Kering, and Richemont control more than 33% of the market. Even though it is evident that there is a general trend towards consolidation within the luxury fashion industry, there are still many brands that remain independent. By analysing Burberry, Ermenegildo Zegna, Chanel, Hermès, and Prada, it is evident that there are various common factors that these independent luxury companies share.

First, companies that are owned by their founders or their founders’ families are far less willing to cash-out from the business than their counterparts. Chanel was founded in 1910 by Pierre Wertheimer and is controlled by his grandchildren, Alain and Gerard Wertheimer, who act as chairmen and controlling shareholders. Thiery Hermès started Hermès in 1837, and to this date the Hermès family still controls more than 60% of the company. Giorgio Armani established Armani in 1975 and acts as the CEO and is the sole shareholder of the company. Similar cases can be observed in Prada, Ralph Lauren, Salvatore Ferragamo, and many other companies.

Second, individual luxury brands aim to have stronger relationships with their customers than companies owned by conglomerates. This is particularly important because repeat customers increase the revenue of a business by spending more than new customers. There is no unique way to achieve these relationships. For instance, Hermès positions itself as a brand of superior luxury and quality with a model of exclusivity and scarcity. Each product is made by hand with a single person in charge of the whole manufacturing. It sells some of the most expensive handbags in the market, but also offers some cheaper products that allow consumers to feel as part of the company at a relatively accessible price point. It has considerably fewer brick-and-mortar stores compared to other luxury fashion brands, to increase the feeling of scarcity, and even has a minimum purchase value to be eligible for the higher-end products. Burberry exemplifies another way to achieve stronger customer-brand relationships via technology. It has been using artificial intelligence and big data for more than 5 years to gain an understanding of its consumers’ preferences to provide higher satisfaction online and in-store. It also uses technology to determine with exactitude whether a product is counterfeit or not, thus strengthening the trust of customers.

Last, to strengthen operations and increase the resilience of supply chains, independent luxury brands have been increasingly acquiring suppliers and subcontractors with the aim of achieving vertical integration for a better control of their supply chain. Subcontractors are considered luxury’s weakest link since they cannot be fully controlled. Moreover, contractors can sometimes cause scandals about poor working conditions or fail to comply with quality guidelines, thus disrupting their clients’ value chain. Chanel and its long history of acquiring suppliers is a perfect example. It bought four different French silk suppliers in 2016, and a Spanish-based leather supplier, Colomer, in 2018. More recently, in 2021, it took a majority stake in Paima, an Italian knitwear company who had been working with Chanel for over 25 years. Similarly, Prada acquired a minority stake in the leather supplier Superior this year. In 2021, Prada partnered with the Zegna Group to take a controlling stake in the Italy-based cashmere producer Filati Biagioli Modesto to secure a domestic supplier and manufacturer.

Whilst independent luxury fashion brands exhibit attractive characteristics, not all brands will be able to stay independent forever. For instance, after reaching a certain stage of growth, independent and often family-owned brands enter a new phase with an ambition for international expansion and desire to acquire a higher market share on the international scale. There are various alternatives these brands may face to gain the required funding:

- Be acquired by a conglomerate

- Attract investment from a financial sponsor

- Go public via an IPO

According to Deloitte’s “Fashion Luxury Private Equity and Investors Survey 2022” report, the average EBITDA margin in the luxury fashion sector in 2019 was 24.1%, the net profit margin was 10.8%, and return on assets was 7.4%. These metrics have remained relatively constant over time but were hit by the COVID-19 pandemic. From 2021, they have been slowly recuperating and approaching pre-COVID results. From the set of analysed companies, only Hermès has outperformed relative to the average. Hermès reported an EBITDA margin of 69.1% in 2019, which was surpassed in 2021 (71.3%). Similarly, reported net income margins were above average at 22.2% in 2019 and 27.2% in 2021. Chanel is also slightly outperforming but not as much as Hermes. Burberry, Chanel and Zegna are all below the average for the industry.

Spotlight: past M&A transactions

To gain insight into how the above factors play out in practice, two past M&A transactions are highlighted.

VF Corporation acquired Supreme

In 2020, VF Corporation reached the definitive agreement to acquire the street fashion leader Supreme valuing the company at USD 2.1bn. VF Corp is an American conglomerate with brands such as Vans, North Face, and Timberland under its management. Despite VF Corp’s corporate culture and the polar opposite street influence of the brand, the deal had several key features that made sense.

First, there has been a long-lasting collaboration between Supreme and a few of the conglomerate’s brands, which have been highly successful in the past. In addition, Supreme generated more than USD 500m in revenue right before the acquisition in 2020, up from USD 200m in 2017. To continue fuelling high revenue growth, Supreme stood to gain from VF Corp’s international scale and experience. In particular, the independent brand would benefit from the supply chain and digital improvements, as well as international visibility in under-penetrated markets. Moreover, the acquisition was a fitting exit opportunity for Supreme’s creative founder and PE firm that previously invested in the street fashion brand.

Estée Lauder acquired Tom Ford

On November 15th, 2022, Estée Lauder acquired the prominent Tom Ford for USD 2.8bn. Estée Lauder is an American cosmetic company that owns brands across perfume, makeup, and other cosmetic product categories. Prior to the acquisition, Tom Ford had several key partnerships driving its business. First, the independent brand had a partnership with Estée Lauder for its luxury and renowned scents line. Additionally, Tom Ford has a licensing agreement with Ermenegildo Zegna and Marcolin for its fashion and eyewear businesses, respectively.

Thus, the first key reason for the acquisition would be continuing to explore synergies arising from the partnerships. Out of USD 2.8bn, Mercolin contributed USD 250m to continue the Tom Ford Eyewear licensing agreement. Meanwhile, Zegna will acquire the Tom Ford fashion business which is necessary to perform its obligations as a licensee, and Zegna already has a 20-year licensing agreement with The Estée Lauder Companies which allows for automatic renewal for a further 10 years. Overall, the acquisition aims to capitalize on the different areas of the Tom Ford brand and yield operational synergies. For Estée Lauder, the acquisition will allow them to eliminate royalty payments on beauty upon closing, gain a new licensing stream of revenue, increase speed and agility, and expand into digital and international markets. Based on estimates, Estée Lauder will save between USD 60m to 70m in annual pre-tax royalties. Moreover, Tom Ford has seen double-digit net sales growth on a compound yearly basis from 2012-2022, so the new owners will have the opportunity to help continue this growth. Finally, the idea is also an excellent exit for the brand’s founder – Tom Ford.

Current state of the luxury fashion industry: an analytical take

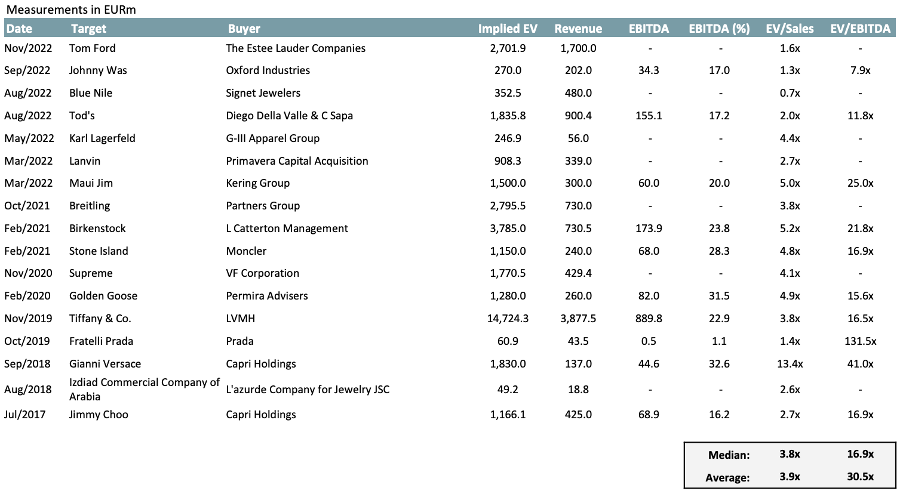

To get a more granular understanding of the value of luxury fashion brands, publicly listed fashion brands are analysed, as well as transactions in the space. Correspondingly, the CCA and CTA can be found in Table 1 and 2. The median EV/Sales and EV/EBITDA multiples observed in transactions in the last 5 years are 3.8x and 16.9x, respectively. Yet, significant variance can be observed amongst the multiples. The 25th percentile and 75th percentile EV/EBITDA multiples are 14.7x and 29.0x, respectively.

Table 1. Comparable Transactions Analysis (CTA)

Source. Mergermarket

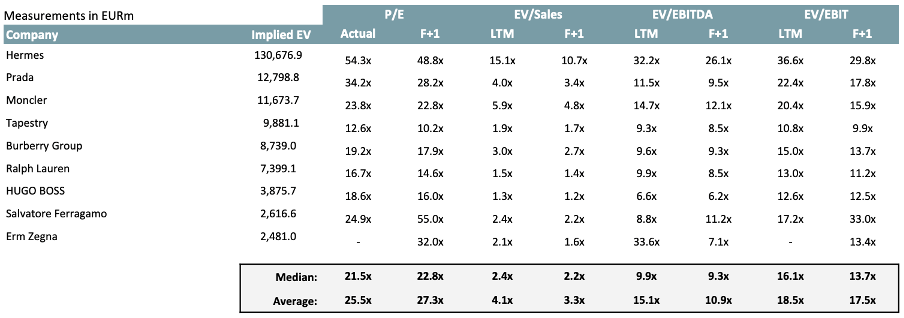

A similar analysis is conducted based on publicly listed fashion brands. As one could expect, higher multiples are observed in the CTA than the CCA. The median LTM EV/Sales and LTM EV/EBITDA multiples observed in among publicly traded companies are 2.4x and 9.9x, respectively.

Table 2. Comparable Company Analysis (CCA)

Source: Bloomberg

*financial results as of Nov 30th, 2022

All in all, multiple facets of the luxury fashion industry have been highlighted, with a specific focus on the ongoing consolidation trend. As a result of past consolidation, the industry has become dominated by numerous conglomerates. Despite the consolidation, there are still plentiful brands that remain independent, including Burberry and Chanel. As highlighted before, not all brands will stay independent forever despite the benefits that being independent provides. However, given the current economic conditions, it is unlikely that significant acquisitions will happen in the coming period as M&A activity is likely to suffer from high inflation and high interest rates. Only the future will tell how much and how quickly the luxury fashion industry will further consolidate.

Authors: Pim van der Klei, Nicole Eberhardt, Guil Hayoun, Andrii Yerokhin, Gabriele Palmieri

References:

https://www.bain.com/insights/retail-m-and-a-report-2022/

https://www.investopedia.com/terms/c/consolidationphase.asp

https://www.pwc.com/gx/en/services/deals/trends/2022.html

https://www.investopedia.com/ask/answers/why-do-companies-merge-or-acquire-other-companies/

https://www.pwc.com/gx/en/services/deals/trends/2022.html

https://www.luxurytribune.com/en/luxury-enters-a-consolidation-cycle

https://www.luxurytribune.com/en/luxury-enters-a-consolidation-cycle

https://www.luxurytribune.com/en/luxury-enters-a-consolidation-cycle

https://www.pymnts.com/news/retail/2016/is-burberry-heading-for-a-takeover/

https://www.asos.com/men/asos-basics/cat/?cid=21508

https://www.nssmag.com/en/fashion/28720/industria-moda-acquisizioni-oligopolio

https://www.ft.com/content/5af71c3d-54b3-4e57-b3a7-cc4985214b94

https://www.nssmag.com/en/fashion/28720/industria-moda-acquisizioni-oligopolio

https://www.retaildive.com/news/estee-lauder-acquires-tom-ford-multi-billion-dollar-deal/636659/

https://www.mergermarket.com/intelligence/view/intelcms-mvpj2w

You must be logged in to post a comment.