INTRODUCTION

The energy industry is one of the most critical sectors in the world and has a significant impact on the global economy. It is an essential component of most economic activities and plays a vital role in producing, transporting, and consuming most goods and services. The industry is also known for its complexity, which mainly arises from the wide range of available energy sources and the sector’s extensive regulation. There exist different levels of consolidation in the energy sector. For example, the fossil fuel industry is highly consolidated, with a few multinational firms sharing most of the reserves and production. At the same time, the unique variety of technologies and sources of the renewable energy field leaves room for a more fragmented market.

DEAL-SPECIFIC INDUSTRY OVERVIEW

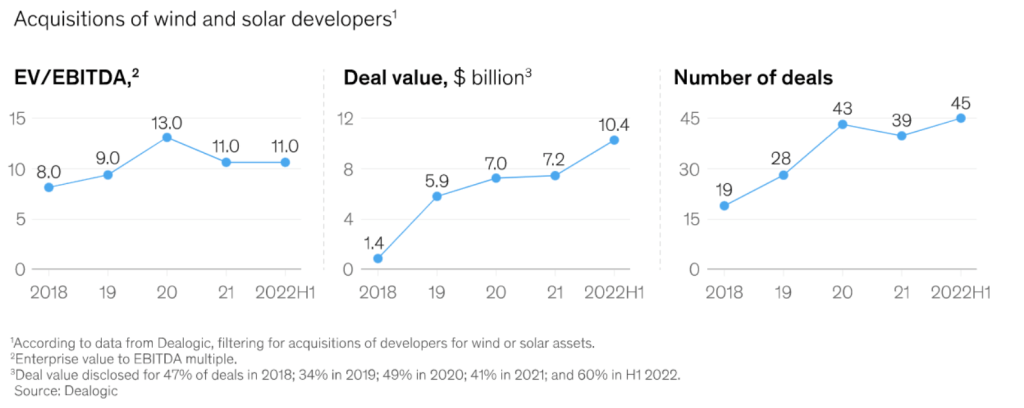

Recent trends towards renewable energy are expected to result in an increasingly consolidated sector. Indeed, driven by environmental issues, technological progress and growing governmental regulations and incentives, renewable energy sources, such as solar and wind power, are becoming increasingly competitive with more traditional energy sources, such as oil and gas. This rapid shift directly impacts M&A transactions in the energy industry as established players seek to benefit from this significant change and hedge against the programmed decline in demand for heavily polluting energy sources. Therefore, the observed trend is the acquisition of smaller, dynamic and technology-focused companies operating in renewable energies by larger multinational enterprises, which can benefit from a diversified energy portfolio and gain expertise in high-potential technologies. The following tables further exemplify this trend.

To illustrate this trend, we will analyze the recent acquisition of Con Edison Clean Energy Businesses Inc., a prominent American operator of solar energy generation, by RWE, a German multinational energy company. The investment is one of RWE’s most significant transactions and one of the biggest green deals in the US market so far. After the acquisition,

RWE will be the fourth largest US player in renewables, and solar energy will account for a 40% stake in RWE ́s US portfolio, given the actual 3% quota.

COMPANIES OVERVIEW

Con Edison Clean Energy Business Inc.

Con Edison Clean Energy is one of the largest investor-owned companies in the energy sector in the USA, founded in 1823 in New York. Its business covers many energy-related products and services run through its subsidiaries in electric, gas and steam utilities. The company operates mainly in New York and Westchester County, serving over 10 million customers and covering about 44% of New York State’s electricity needs. The company is considered the most reliable energy provider in the US.

In 2022 the total value of assets reached $69.07 billion, with a 9.43% increase from the previous year. Revenues amounted to $15,67 billion, representing an increase of 14.58% compared to 2021. Con Edison aims to become carbon neutral by 2040 and plans to invest over 3.5 billion dollars in green projects between 2023 and 2025. The aim is to invest in programs improving system efficiency and energy use management to decrease emissions and energy usage.

The company’s renewable portfolio is composed mainly of solar and wind energy. Furthermore, the company holds a wide range of infrastructures for energy distribution, such as an enormous system of more than 89,000 miles of underground cables, 34,000 miles of overhead lines, 250,000 manholes and service boxes, 25,000 underground transformers and 201,000 utility poles.

The ESG rating by Sustainalytics of Con Edison is 23.1, categorizing Con Edison in the group of medium-risk companies.

RWE AG

RWE is a multinational company founded in 1898 in Essen, operating globally among Europe, Asia-Pacific and US, covering up to 20 million customers. Its three core businesses are energy generation, energy trading and energy retail. Furthermore, RWE offers services related to energy efficiency and storage solutions. For what concerns the first sector, RWE relies both on unrenewable sources such as coal, gas and nuclear and renewable sources like hydropower, biomass, and off- and onshore wind and solar. In particular, this diversified portfolio of conventional and renewable energy allows RWE to rank globally as number two in offshore wind power and number three in renewable energy.

The company is listed on the Frankfurt Stock Exchange and several other stock exchanges. Its total revenues amounted to €38,569 billion, and its total assets to €138,548 billion as of 2022.

The company is intensely engaged in leading the way to a green energy world. The latest ESG score of the company provided by Sustainalytics amounts to 22.7, classifying RWE as medium risk.

DEAL STRUCTURE

The acquisition price of Con Edison Clean Energy is $6.8 billion, including debt. The valuation multiple of Con Edison (EV/EBITDA) of 11x is almost double that of RWE. Despite the significant acquisition premium, the deal is earnings accretive from year one, bringing an extra $600 million yearly to RWE’s EBITDA that originates from Con Edison solar parks and wind farms. RWE has proposed maintaining an unaltered dividend of €0.90 per share for the fiscal year 2022. The decision is subject to passing a resolution at the Annual General Meeting on 4th May.

The acquisition was funded through debt instruments and equity capital measures undertaken by RWE. RWE performed a mandatory convertible bond issuance of $2.43 billion to a Qatar Investment Authority (QIA) subsidiary: Qatar’s sovereign wealth fund. QIA took around 10% of RWE’s share capital in return, resulting in a 9.09% stake post-conversion, making the fund RWE’s largest single shareholder. The conversion into 67.6 million new ordinary bearer shares happened on 15th March 2023.

DEAL RATIONALE

In the following, we analyze the main reasons why RWE acquired Con Edison Clean Energy.

First of all, thanks to this acquisition, RWE has expanded its presence in the renewable energy sector in North America, to expand its business coast to coast in the coming years to increase its presence and strength throughout the territory. RWE has chosen Con Edison Clean Energy for its strong and recognized position in the US market, with a portfolio of assets in key regions, including New York and California. The acquisition helps RWE to establish a strong foothold in the US market and capitalize on the growing demand for renewable energy, which is now one of the fastest-growing sectors in the world. The extended tax breaks for green projects have probably played a role in determining such an attractive acquisition price. These fiscal benefits result from the Inflation Reduction Act, signed into law in August 2022. The law includes significant climate change legislation and almost $370 billion dedicated to green programmes.

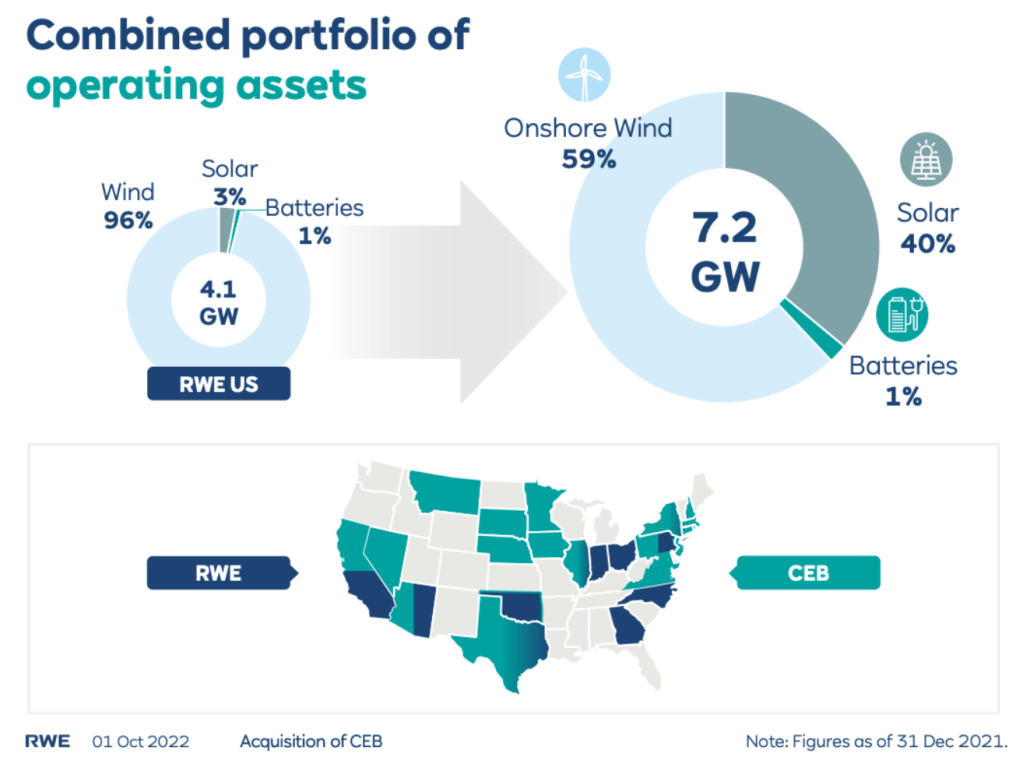

Secondly, with the acquisition of Con Edison Clean Energy, RWE aims to increase its renewable capacity and accelerate growth in the US market. In addition, this consolidation is the result of combining the two portfolios, which significantly increased the diversification and rebalancing of RWE’s US portfolio assets. Before the acquisition, RWE had a portfolio of 96% wind energy. After the acquisition, the portfolio will be characterized only by 59% wind energy, 40% from solar energy and 1% of battery energy (which is expected to increase to 25% by the end of 2030). This operation will lead RWE to become one of the top four renewable energy companies and the second largest solar operator in the United States with a total capacity of over seven gigawatts and creates the prospect for structural growth in the coming years to reach thirteen gigawatts of renewable energy capacity in the portfolio only by the end of 2023. The following chart further illustrates the development, diversification, and expansion in the US market.

Besides the opportunities mentioned above in the US, there are further vital reasons why RWE acquired Con Edison Clean Energy. Con Edison has solid experience investing in new technologies such as battery storage, extensive platform development and storage financial positions, which will improve RWE’s technological capabilities in most cases in offshore wind and solar energy, helping it stay ahead of the competition. In addition, Con Edison Clean Energy has an outstanding track record in developing, building, and managing renewable plants.

CONCLUSION

The recent trend shows that established players acquire smaller and technology-focused companies in the renewable energy sector to diversify their portfolio and expand their knowledge. RWE did precisely this with the acquisition of Con Edison Clean Energy. The investment helps RWE establish a strong foothold in the US market and capitalize on the growing demand for renewable energy. RWE will benefit from Con Edison ́s know-how and economies of scale that will enable the company to achieve its long-term goal of becoming one of the leading companies in the renewable sector, reaching €50 billion gross capital by the end of 2030 and becoming a 100% carbon-free company by 2040.

Sources:

McKinsey, RWE investor relations (press releases), RWE annual report 2022, Con Edison consolidated report 2022, Reuters, Financial Times, Renewables Now

Authors:

Irene Bencini, Lorenzo Cundari, Alessandro Monticone, Louis Paget, Lukas Brendel

You must be logged in to post a comment.