Year by year, financial sponsors account for a significant share of the global M&A activity. Yet, in 2022, this share fluctuated and differed starkly between the first and second half of the year. This pattern can generally be explained by changes in the macroeconomic environment, where interest rate hikes took centre stage in 2022. As such, a general “pause” in deal activity can be observed and the endurance of this “pause” into 2023 will depend on how promptly macroeconomic uncertainties stabilise. This article serves as a brief primer on private equity and will zoom in on how private equity activity developed over 2022 and will develop into 2023.

Private Equity Primer

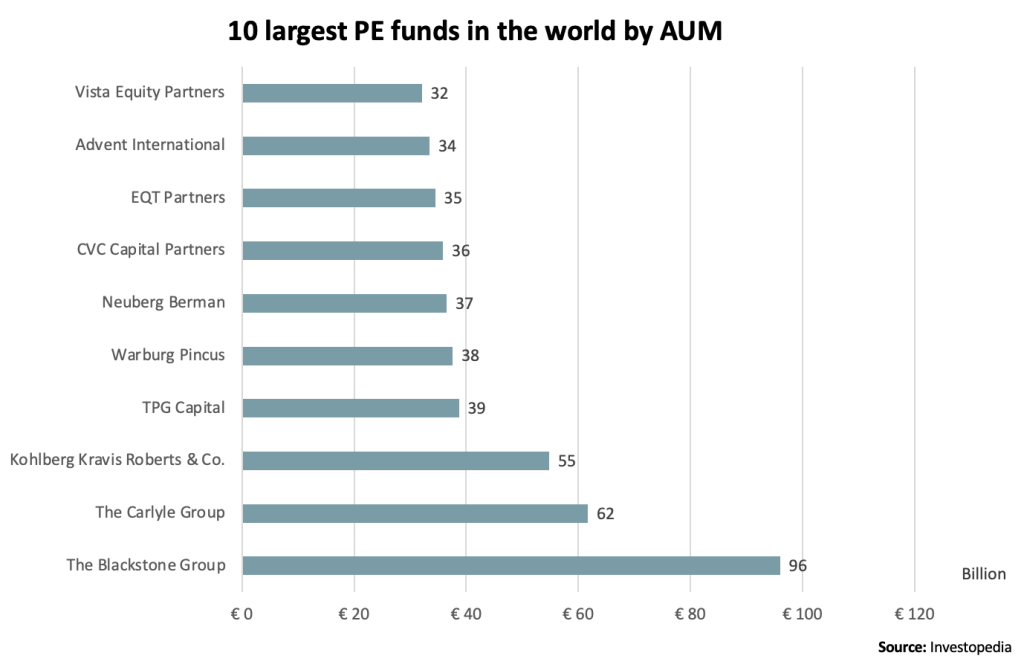

Private equity (PE) is an alternative asset class: a supplemental investment strategy to traditional long-only positions in stocks, bonds and cash. It generally occurs on private markets in which funds and investors directly invest in companies or engage in buyouts. The aim of PE firms is to acquire ownership in companies with the intent of increasing their value over a certain period of time and then selling them for a profit. Private equity investments are typically available to high-net-worth individuals (HNWIs) and institutional investors. In addition, PE can have various forms, from complex leveraged buyouts to venture capital. PE firms are typically ranked by their assets under management (AUM) and success in returning gains to investors. Currently there are more than 18,000 PE funds in the world with a nearly 60% increase in just the last five years. PE currently has $4.4 trillion in assets under management and the size of these funds has more than doubled since 2016. As such, the PE landscape has taken the below shape.

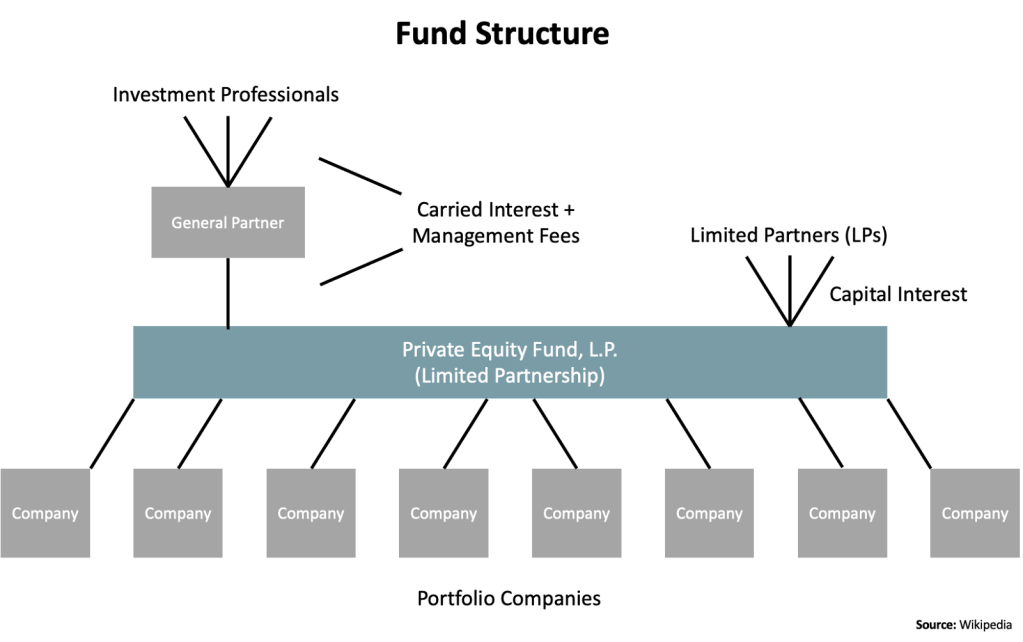

To create a private equity fund, money is raised from limited partners (LPs). During the fund raising, investors make commitments and then the fund seeks investment targets. They only draw the funds once they have found an investment opportunity. After reaching their fundraising target they close the fund and invest in (private) businesses. The General Partner (GP) is the term used to refer to the private equity company. GPs execute and oversee the fund’s operations as well as secure investment commitments. PE funds usually hold a collection of separate company investments that are made over a prescribed time. This collection makes up the PE fund’s portfolio. The majority of capital used by PE companies comes from Limited Partners, who can be either institutional or individual investors.

There are several types of private equity investment strategies and some PE firms specialise in a particular deal category. The main ones are: leveraged buyouts, venture capital and growth equity. In a leveraged buyout (LBO), significant debt is used to fund the purchase of a business with the intention of enhancing operations and ultimately selling it for a profit. Venture capital entails making investments in start-up businesses with the potential for rapid growth and substantial returns. Due to the less established operations and revenue streams of early-stage businesses, these investments are usually riskier than LBOs. However, if the business is successful, they also have the potential to yield higher returns. Growth equity investments involve providing capital to established businesses that want to grow their business or penetrate new markets. These investments generally carry lower risk than venture capital, because the company already has a successful track record, and yield lower returns than venture capital. In addition to the ones already described, other PE investment strategies include: secondary buyouts, distressed investing, carve-outs and mezzanine financing.

Private Equity in 2022: A Year in Review

2021 was a record-breaking year in terms of PE activity, and the first half of 2022 followed the same trend. However, during the second half of the year, deal flow suffered a sharp falloff. Compared to 2021, the global buyout deal count only decreased by 10% to a total of 2,318 transactions, but the fall in global buyout value was considerably larger: it totalled $654 billion, representing a 35% decline. Nevertheless, it is important to highlight that the activity in 2021 was out of the ordinary. Compared to the average from 2017 to 2021, the deal value in 2022 was higher by 12%. Another fact to point out is that most of the activity took place in the first half of the year. H1 2022 and H2 2022 tell two completely different stories.

Before 2022, PE funds benefited from an advantageous macroeconomic environment that had held for more than a decade: low inflation, expansive monetary policy, increasing globalisation, restrained volatility, and abundant market liquidity. However, at the start of the year, inflation rates began to increase, the Russia-Ukraine war broke out, and geopolitical tension with China grew. Regardless of these headwinds, H1 2022 started off the same way 2021 ended. As expected, the leading 3 PE transactions with the highest deal value were announced in this period. The top spot was held by the Benetton family and Blackstone offering to buy the Italian highway operator Atlantia for €42.7 billion. It not only was the biggest PE deal, but also the second biggest transaction globally and the largest take-private deal ever for a European-listed company. In the first 6 months of the year, PE generated a total of $512 billion in buyout deal value worldwide. By continuing at this pace, PE would have achieved its second-highest annual total ever, just behind the all-time record set in 2021. The 18-month total of $1.7 trillion is the strongest period in the industry’s history.

The stark contrast between the first and second half of the year was marked by the announcement of a 75 basis point interest rate increase by the Federal Reserve (Fed) in June. The central banks of the largest economies started delivering similar policies, which resulted in the end of cheap debt globally. Aggregate deal value in H2 2022 was close to a third of what it had been in H1 2022.

Not a single region escaped the downturn. Asia-Pacific was particularly hit hard due to the repeated market shutdowns caused by Covid-19 restrictions in response to new outbreaks. Deal value in the region decreased by 59% in comparison to 2021. Excluding North America (-30%) and Europe (-28%), deal value in the rest of the world plummeted by 72%. Similarly, most sectors suffered from the slowdown; the ones hit the most were telecommunications, retail, and consumer products. Only the services and transportation industries grew when compared to the previous year. A trend that did not change was the technology sector holding the largest share of buyout deals.

Unsurprisingly, the fall in deal activity was not the only evidence of a slowdown in PE. Fundraising experienced a significant decline on a global scale, falling by 15% to $655 billion, and marking the lowest amount collected by the asset class since 2017 (with the exception of the pandemic-driven deceleration in 2020). All of the main PE strategies underwent a decline in fundraising by more than 10%. Buyouts recorded an 18% decrease, while growth equity and venture capital experienced a decline of 17% and 11%, respectively. Performance followed a similar trend: for the first time in 6 years, PE was overtaken by other private markets asset classes in terms of performance. All PE strategies achieved negative returns: buyouts returned -6%, and those more exposed to the technology sector, growth and venture capital, returned -14.9% and -14.7% respectively. These disappointing results were caused by an unprecedented mix of macroeconomic forces: high interest rates in response to rising inflation, increasing geopolitical tensions, real economy downturn, and overall uncertainty.

However, it is undoubtedly the inflation accompanied by the rising interest rates that caused the biggest hit to the industry. During 2020, in response to the Covid-19 lockdown, the Federal Reserve cut interest rates twice in March, by a total of 150 basis points. These measures allowed the US to bounce back from the pandemic, but, among other factors, led to the highest and most persistent inflation in 40 years. In 2022, the Fed and the European Central Bank (ECB) followed very similar policies in their attempt to tame inflation. Starting in June, the Fed started aggressively hiking interest rates (which it had not done at that degree since the 1980s) and the ECB raised interest rates for the first time in 11 years. By the close of the year, the Fed had increased interest rates by 425 basis points and the ECB by 250. It comes as no surprise that the slowdown in PE activity occurred in the second half of the year: it was a direct cause of the interest rate hikes.

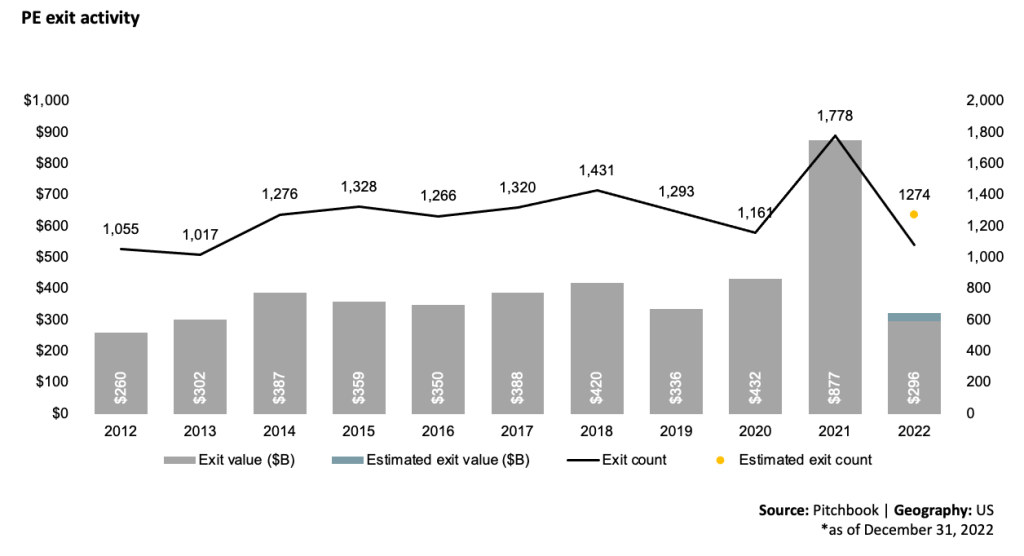

The tight monetary policy had numerous effects on different aspects of the PE industry. In previous years, the PE market thrived with cheap debt, which allowed for higher deal count and deal value. The interest rate hikes marked the end of inexpensive debt financing. If a LBO was carried out using floating-interest rates, their debt expense increased significantly, and therefore, the return on the investment was greatly diminished. Another way that interest rates impacted returns were through valuations. Higher interest rates are generally associated with lower stock valuations, resulting in falling PE exits. The aggregate value of PE exits was down 32.1% from 2021. Particularly, private equity backed IPOs fell by 68% in aggregate value, and from 196 to 52 in deal count. Moreover, not only were banks offering more expensive debt, but they were reluctant to give out loans at all. PE firms who wanted to take advantage of the lower valuations to make an investment had to turn to direct lenders who could offer smaller loans for smaller transactions. Consequently, deals worth less than $1 billion gained a larger share of the total value and the average deal size dropped by 23% to $964 million.

Private Equity in 2023: An Outlook

The big question now is what M&A activity from PEs will look like going further into 2023. As discussed earlier, there are many different drivers influencing this, which makes predicting the future hard.

One of the most important things to look at are the interest rates set by the central banks as part of their monetary policy. As interest rates are set to battle inflation, it is important to delve a bit deeper in the current trends surrounding this topic. Although inflation decreased from its highest levels of 9 to 11% YoY achieved in many of the major Western economies around June and July 2022, it is currently still high around the world and has not been slowing as quickly this year as central bank officials expected. Declining energy prices and the earlier-than-expected opening of China in beginning 2023 helped brighten the outlook, but there are still no signs of inflation nearing the 2% target level set by the Fed and other major central banks. At this pace, that target is not expected to be achieved for at least two more years.

This means interest rates are not expected to decrease in the short term. The last rate hike of the Fed was earlier in March this year, bringing its benchmark borrowing rate to a new 4.75-5% target range. Chairperson of the Fed, Jerome Powell, said that “participants don’t see rate cuts this year”, indicating that rates will at least remain at the current level in 2023. Rather, market participants are anticipating a 75 basis point cut in early 2024, which is still far from now. The Organisation for Economic Co-operation and Development (OECD) also forecasts a tight monetary policy rate across all major economies going into 2023 because inflationary pressure is still largely there, although it is cooling off.

For private equity funds this means that financing will most likely remain expensive the coming year, which does not brighten the outlook for deal activity in the industry. However, there are some tailwinds expected to boost M&A activity of PEs in the coming year. During 2022, when acquisitions dropped significantly, PEs were still raising a lot of money, as investors were looking for downside protection in private market deals (private markets tend to perform better than public markets during recessions). That means that at the moment PEs have a lot of dry powder which will need to be deployed sooner or later, as LPs pay management fees to GPs for them to make investments. Therefore, doing nothing with the capital will leave investors dissatisfied. At the moment, any further slowdown in their investments could jeopardise the ability of PEs to invest all the funds that they have committed to do.

Another potential tailwind for the coming year are the many delayed IPOs from last year which are still looking to raise funds. Last year, equity markets performed very badly due to macroeconomic and geopolitical factors previously mentioned. Consequently, many firms looking to go public via an IPO postponed this. Many of these firms are still looking to raise funds, and since equity markets have not recovered to their glory days of before the interest rate hikes, firms are increasingly considering raising capital through the involvement of PE firms. All in all, macro-economic drivers are still not pointing in the direction of a sudden increase in M&A activity by PEs, but there are some factors expected to speed up this activity going forward in 2023.

Private Equity: Trends and Case Studies

Besides evaluating the PE activity in 2022 and forecast for 2023, various trends will be highlighted. Specifically, PE exits, ESG and alternative financing options will be discussed.

Exits and Continuation funds

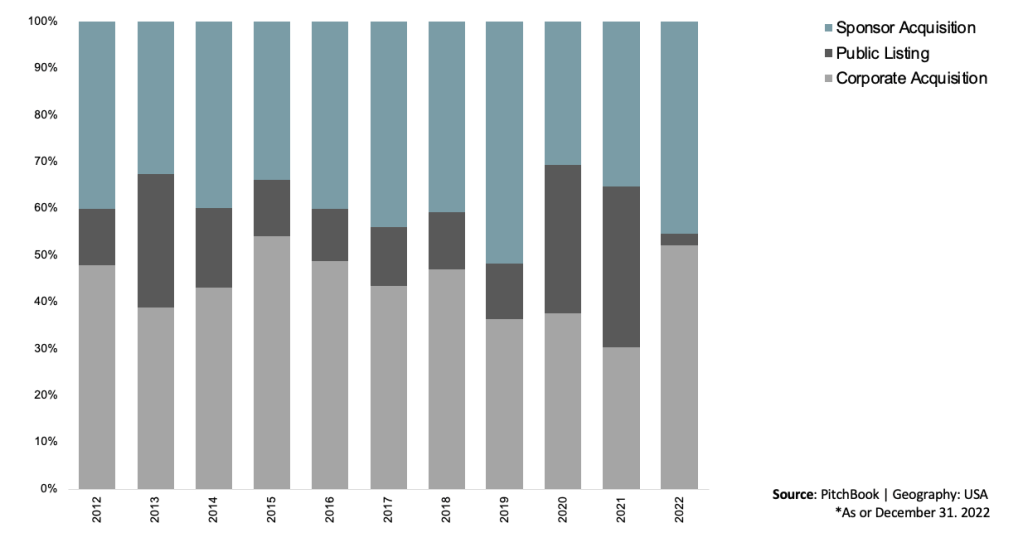

One of the most impactful trends in PE exit activity is the decline of initial public listings (IPOs) as a viable option for funds. In 2022, public listings only accounted for 2.5% of exit value, while they were around one-third of exit value in 2020 and 2021. The drastic shift reflects increasingly changing sentiment towards the bear market as the public markets look less appealing due to lower valuations compared to those in the past few years. With IPOs off the table, PE firms looked for exits to other sponsors and corporates, which have been in line with historical levels.

In 2022, GPs exited 547 companies to other sponsors, totaling $134 billion. Sponsor-to-sponsor deals accounted for 45.3% of US PE exit value, a significant increase from the 10-year average of 38.8%. Increasing preference towards sponsor-to-sponsor exits instead of corporate buyers is a reversal of the trends seen over the last decade. Sponsor-to-sponsor transactions have gradually increased over time as a share of exit activity, and they are expected to make up a record portion of US PE exit value in 2023. The number of PE managers has steadily grown, while the number of corporate buyers has remained relatively stable, with sponsors more readily pursuing deals using their dry powder than corporate buyers focusing on protecting their balance sheets amid recessionary concerns.

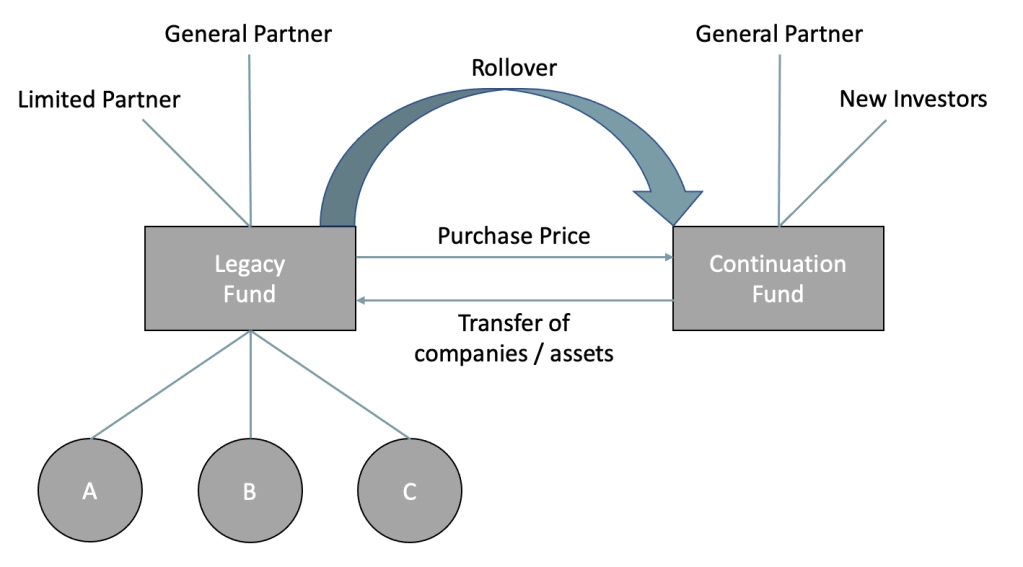

Continuation funds are a type of private equity fund structure that allows existing investors to realise value from an investment while providing an opportunity for new investors to gain exposure to a specific asset or portfolio.

In a continuation fund transaction, a new fund is created to acquire one or more existing assets from an existing private equity fund. This is typically done when a fund is approaching the end of its life but still holds assets that have not yet reached their full potential or are not ready for exit. The existing investors, or LPs, can choose to either cash out and receive liquidity, or roll over their investment into the new continuation fund. This enables the GP to continue managing the asset(s) with a longer investment horizon and additional capital if required.

Continuation funds can be beneficial for both GPs and LPs:

- For GPs: Continuation funds allow them to retain and manage assets they believe have more potential for value creation, without being forced to exit due to the end of a fund’s life. This can result in better alignment of investment timelines with the underlying assets, and potentially higher returns.

- For LPs: Continuation funds provide an option to either exit an investment and receive liquidity or maintain exposure to the asset(s) if they believe there is still potential for appreciation. This flexibility can be particularly attractive for LPs with specific liquidity needs or portfolio management considerations.

Continuation funds have gained popularity in recent years, as they provide a solution to some of the challenges faced by the private equity industry, including liquidity management and optimising investment timelines. This trend is likely to gain more momentum as market conditions worsen, valuations remain low, and GPs seek new ways to provide liquidity to their investors in a weaker exit environment.

In 2022, sponsor-to-sponsor exits were present across all sectors showing a YoY decline consistent with a general decrease in deal volume. The biggest deal of the year was the $17 billion acquisition of Athenahealth by PE firms Hellman & Friedman (H&F) and Bain Capital from Vertitas Capital and Evergreen Cost Capital. Another notable deal was the $8 billion merger of Information Resources and NPD Group. H&F was a majority investor in the company, while Vestar Capital Partners and New Moutain Capital were significant investors in the IRI. The newly created company is expected to deliver an analytics platform to visualise consumer behaviour and retail trends across a broad range of industries.

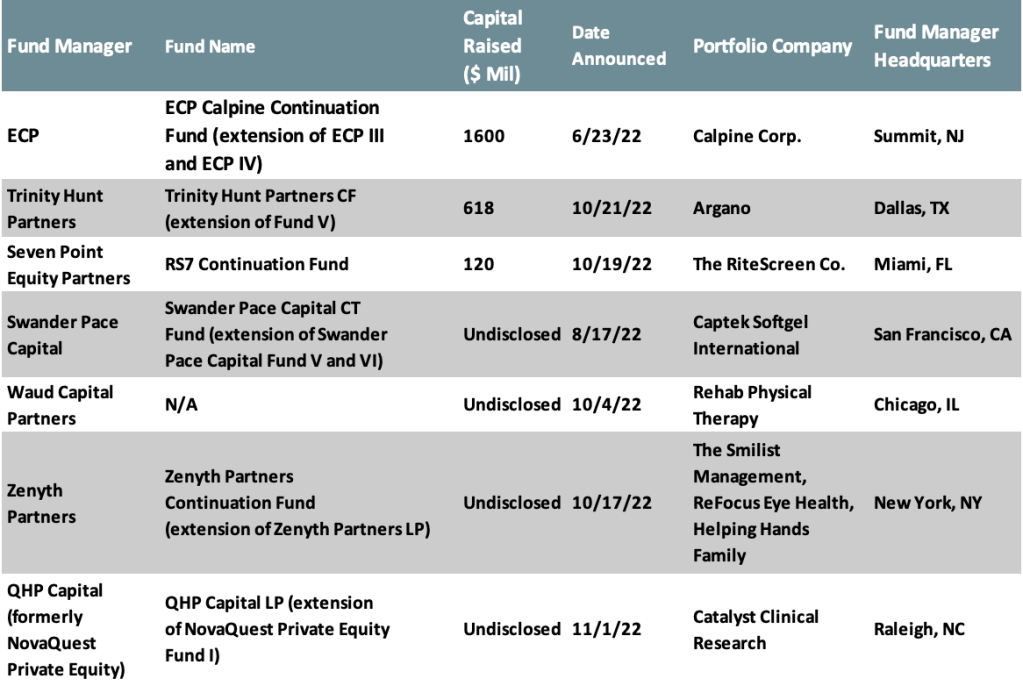

2022 Highlights: Continuation Funds

ESG and Private Equity: Investing in a Sustainable Future

Another big trend that has been coming up over the past few years and will most definitely continue into 2023 is the investments of PEs in companies related to the energy transition and decarbonisation of the world. Regulators and investors are increasingly calling for fund portfolios to be more ESG friendly, putting pressure on fund managers to meet certain sustainability linked criteria. However, this is generally not seen as a downside by PE funds. PEs are not just merely investing in sustainable companies for the sake of increasing exposure to ESG factors. They are investing with a clear strategy to take advantage in these unique times. The energy transition provides tremendous opportunities to capitalise on companies supplying the technology, products, and services that will drive the shift away from carbon energy across the global economy.

From 2017 to 2022, PEs worldwide have invested more than $160 billion in energy transition-related companies. An example of a notable deal is Blackstone’s $1.4 billion acquisition in 2021 of Sphera. Sphera is a leading SaaS software, proprietary data and consulting services provider helping companies manage and mitigate risks with their ESG data. PEs have also become more selective when it comes to their acquisition targets. According to a survey done by PwC, in 2022 72% of PEs always screen for ESG risks and opportunities at the pre-acquisition stage and 37% and 56% have turned down investments because of ESG related matters.

Alternative Financing Options

In the context of worsening macroeconomic conditions, sponsors are looking for alternative financing options to facilitate the deal flow.

Using equity and delaying borrowing:

Amid challenging market circumstances, a “purchase now, finance later” approach has been adopted by some sponsors, which involves all/mostly-equity transactions. Sponsors, in these instances, contribute sizable equity amounts with a view to increase leverage when market conditions improve. This strategy is exemplified by KKR’s takeover of April Group, the second-largest insurance broker in France. Specifically, the deal value of $2 billion was fully paid in equity by KKR with plans to negotiate debt down the line. In fact, CVC Credit, a credit-focused investment firm, has agreed to provide senior debt financing to help fund KKR’s purchase of April Group on April 11, 2023. By initially dedicating a significant portion of equity to the deal, KKR was in a position to secure the acquisition and subsequently seek opportunities to enhance the debt portion as the lending landscape turned more favourable. This particular deal is a great example of two recent trends: use of alternative financing and increase in sponsor-to-sponsor transactions.

Debt retention:

Another emerging trend involved in deal structuring is allowing a target company’s existing debt to remain in place post-transaction. An example is BDT Capital’s acquisition of Weber, a leading grill manufacturer. By keeping the existing debt intact, the transaction becomes more “debt-efficient,” although it may limit buyout opportunities to more modest transactions, such as capping new investments below 50%. This approach can also require moderating consent and board rights to avoid triggering change-of-control provisions.

Use of Seller’s Note:

In some cases, purchasers resorted to financing options provided by sellers, like seller notes, to bridge the financing shortfall. This approach is especially relevant when the seller is a substantial strategic organisation disposing of non core assets. A case in point is the acquisition of Netspend, a top prepaid card provider, by Searchlight Capital Partners and Rêv Worldwide from Global Payments, which was partially funded through a seller note issued by Global Payments. By extending seller-provided financing, Global Payments enabled the successful completion of the deal, while the acquirers managed to cover the funding gap without solely depending on conventional debt financing sources.

Conclusion

2021 was a record-breaking year for PE activity and the first half of 2022 continued this trend. However, during the second half of the year, deal flow decreased sharply due to changes in the macroeconomic environment. Specifically the rising inflation and interest rates hit the industry hard. Despite this decline, the deal value in 2022 was still higher than the average from 2017 to 2021. For 2023, it is uncertain what PE activity will look like. Yet, general expectations are that the deal activity will increase in the second half of the year. The most important drivers are the interest rates and inflations, which are not expected to decrease significantly in the short term. Consequently, financing will generally remain expensive in the coming year, negatively affecting the deal PE activity. Yet, potential tailwinds are formed by significant dry power that PE vehicles hold and the expectation of increased capital market activity.

Authors: Pim van der Klei, Nicole Eberhardt, Andrii Yerokhin, Antonio Maude, Tobias Van Winkel

https://www.nyujlb.org/single-post/to-continue-or-not-to-continue-the-rise-of-continuation-funds

https://www.eurazeo.com/fr/rise-gp-led-transactions-version-anglaise

https://www.bennettjones.com/Blogs-Section/Continuation-Funds-A-Growing-Trend

https://www.blackrock.com/institutions/en-us/insights/private-markets-outlook

https://pitchbook.com/news/reports/2022-annual-us-pe-breakdown

https://www.cvc.com/media/news/2023/2023-04-11-cvc-credit-supports-kkr-s-acquisition-of-april-group/

https://www.loanconnector.com/NewsDisplay/NewsDocumentContent?PublicdocId=5143145

https://www.investopedia.com/articles/markets/011116/worlds-top-10-private-equity-firms-apo-bx.asp

https://www.investopedia.com/terms/p/privateequity.asp

https://www.ey.com/en_gl/private-equity/pulse

https://news.bloomberglaw.com/bloomberg-law-analysis/analysis-how-private-equity-fared-in-2022

https://www.invesco.com/apac/en/institutional/insights/market-outlook/investment-outlook.html

Private Markets Outlook: A New World in 2023 and Beyond? | Russell Investments

Private Equity Report: 2022 Trends & 2023 Outlook : Cherry Bekaert (cbh.com)

https://www.blackrock.com/institutions/en-us/insights/private-markets-outlook

https://www.rsm.global/insights/profile-private-equity-investment-activity-we-expect-see-2023

You must be logged in to post a comment.