Introduction

The acquisition of Credit Suisse by UBS saw two of the largest banks in Switzerland joining to create one of the most influential lenders in Europe. However, amidst the turmoil in the banking industry along with uncertainties about the deal, the prospects of this operation’s future are filled with ambiguities and questions.

UBS has a long history in the Swiss banking industry, with roots of the company dating back as far as 1862 to the foundation of the Bank in Winterthur. Following a lengthy series of mergers and acquisitions, the institution under the name we know today was formed in 1998, preceded by a merger of Union Bank of Switzerland and Swiss Bank Corporation, the second and third largest banks in Switzerland at the time. The merger created the second largest bank in the world during that period and has stayed the largest lender in Switzerland to this day.

The emergence of Credit Suisse dates to the same period as the former, founded in 1856. Over the 19th and the 20th centuries the company consolidated its strong position in the European country, acquiring many Swiss and foreign banks to grow its size, with a considerably aggressive series of acquisitions in the 1990s. Having been one of the most influential banks in the world for countless years, its downfall and collapse is one where both the acquiring party and the banking industry will see a significant impact.

2022: A year of trouble

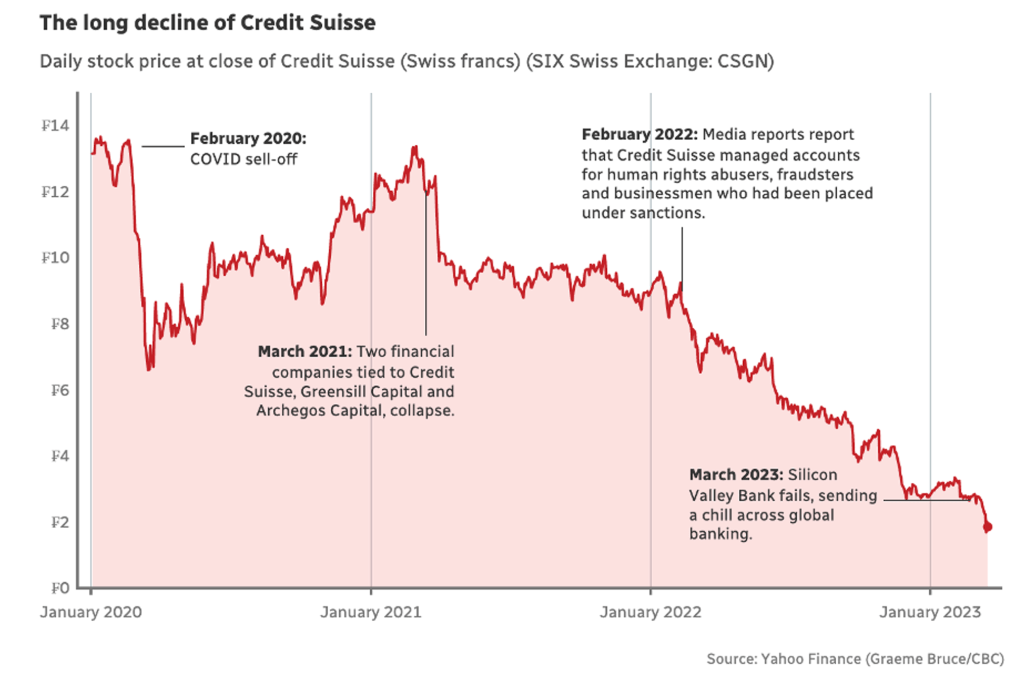

Following several scandals, Credit Suisse finished 2021 with a loss 1.57bn CHF, a much larger loss than what was expected. This was due to the several large-scale scandals that they had to face, prompting the company to take litigation provisions of 1.1 billion CHF. After such a challenging year, the lender was going into 2022 with plans to restructure and improve its situation.

This, however, was not the case, as the company reported a loss in Q1 of 2022 with further increases in its legal provisions, following further scandals and pressure from Russia’s invasion of Ukraine in February of that year. This was amplified by the revealing of the bank’s secrets, bringing to light over $8 billion held in accounts of criminals, dictators, and human rights abusers. 90% of the 18,000 accounts were already closed, but the spill of information had a substantial effect on the institution’s reputation and shook the confidence of investors and holders of accounts.

After rumours spreading on social media about the bank’s financial health, wealthy clients withdrew 63.5bn CHF, equivalent to roughly 10% of its total wealth management assets. This put the bank into a dire situation, reporting a consequent loss of 1.5bn CHF for Q4 of 2022.

Collapse and Acquisition

After the collapse of SVB bank igniting turmoil in the banking industry, Credit Suisse suffered further. To recover from the scandals experienced in the years prior, the Swiss lender requested more capital from its biggest investor, the Saudi National Bank. SNB rejected this request, as they held a stake of 9.88%, and were unable to exceed 10% due to Swiss regulations.

This was followed by a requested from CS to receive backing from the Swiss National Bank. It was stated that additional liquidity to the bank would be provided if needed. After this, the Swiss government was enticing UBS, the largest Swiss bank, to acquire the troubled company, offering its support.

On March 19 of this year, UBS had agreed to buy the bank for over $2bn in an all-stock deal, paying CHF0.5 a share. This was later increased to CHF0.76 a share to a deal of CHF3bn. This deal, as mentioned prior, was supported by the Swiss government, shown by the $100 billion liquidity line offered to UBS as part of the deal.

As a pragmatic and fast deal, the exact impacts on each company are hard to estimate, but UBS has stated that it plans to reduce the scale of the acquired company’s investment banking division. The rapid nature of this deal raises one major question: what are we to expect from this deal, and how will this newly combined business perform in this industry?

Industry Overview

The Swiss banking industry is one of the largest in the world, with assets under management (AUM) of around $6.5 trillion. It is also home to some of the biggest and most influential banks globally, including Credit Suisse and UBS. In 2023, UBS announced its acquisition of Credit Suisse, which sent shockwaves throughout the banking industry, particularly in Switzerland.

The Swiss banking industry has seen steady growth over the past decade. At the end of 2021, total banking sector assets in Switzerland stood at 3.9 trillion Swiss francs, equivalent to 520% of Switzerland’s GDP, the highest among developed countries, according to the 2022 Swiss Financial Stability Report by the SNB.

One of the key reasons behind the acquisition of Credit Suisse by UBS is the ongoing pressure on the banking industry, both in Switzerland and globally. In recent years, the banking industry has faced a range of challenges, including increasing competition, low interest rates, changing consumer behaviour as well as higher inflation. These factors have made it increasingly difficult for banks to generate profits, and many have been forced to cut costs and restructure their businesses.

Furthermore, uncertainty in the banking sector was greatly increased with the collapse of Signature Bank and Silvergate Bank, big banks in the crypto industry. Tech-lender Silicon Valley Bank also contributed to the turmoil, being the second biggest bank (by assets) in US history to collapse after a bank run.

Having said that, what caused the collapse of the 167 years old institution was mainly internal struggles and issues. These happened continuously, tainting the image of Credit Suisse, and leading to the loss of investor confidence. Losing financial support from its largest shareholder, Saudi National Bank, due to regulatory restrictions also caused the share price to drop to an all-time low.

The biggest impact on the industry was the frenzy caused when the merger deal included the wiping out of $17 billion worth of additional tier 1 (AT1) bonds. This was an unprecedented move as traditionally bondholders are senior to shareholders but in this case, AT1 bondholders would receive nothing while shareholders would walk away with $3.2bn. This caused investors to panic and for prices of other AT1 bonds in Europe to drop, with EU regulators having to step in to clarify that such a situation would not happen with other European banks.

The acquisition of Credit Suisse by UBS is expected to bring significant benefits to both banks, including cost savings, increased scale, and enhanced capabilities. For UBS, the acquisition will provide an opportunity to expand its wealth management business and increase its presence in the Swiss domestic market. For Credit Suisse, the acquisition will provide much-needed capital and support, enabling the bank to focus on its core businesses and improve profitability.

Regarding investment banking, the impact will be less felt as even prior to the collapse, Credit Suisse had already planned to spin off its investment banking division to Wall Street Dealmaker Michael Klein’s advisory firm, though UBS is unlikely to approve the deal now. UBS themselves have also reduced investment banking activity in favour of wealth management, which contributes to ~54% of its revenue. However, the acquisition is not without its challenges. One of the biggest concerns is the impact on jobs in Switzerland, particularly in the Zurich area, where both banks have significant operations. The merger is expected to result in significant job losses, with some estimates suggesting that up to 30% of the combined workforce could be affected.

Another concern is the potential impact on the wider Swiss banking industry. With UBS becoming the dominant player in the market, some analysts have raised concerns about the lack of competition and the potential impact on pricing and service quality. There are also concerns about the potential impact on smaller banks in Switzerland, who may struggle to compete with the larger, more powerful UBS.

Despite these concerns, the acquisition is expected to be a positive development for the Swiss banking industry, particularly in the long term. The consolidation of the industry is likely to result in a more efficient and competitive banking sector, with a stronger focus on innovation and customer service. It is also expected to create opportunities for new entrants into the market, particularly in areas such as fintech and digital banking.

Company Overviews

Acquirer – UBS

- Foundation: 1998

- Headquartered in Zürich, Switzerland

- CEO: Sergio Ermotti

- Number of employees: 74,022

- Market Cap: $65.7bn (19/04/2023)

- LTM Revenue: $34.4b

- LTM EBT: $9.5bn

- LTM P/E: 9.1x

- LTM P/BV: 1.1x

UBS is a financial services company headquartered in Zürich, Switzerland, the only country where it operates in all its four main business units. Founded in 1998 by the merger of Union Bank of Switzerland and Swiss Bank Corporation, UBS is the third largest bank in Europe with a market capitalization of $65bn, making it one of the eight global “Bulge Bracket Banks”. The company has a network of around 200 branches and 4,600 client advisors.

Sustained by modern digital banking services and customer service centers, UBS can reach approximately 80% of Swiss wealth and serve one in three households, high net worth individuals and pension funds, more than 120,000 companies, and around 80% of banks domiciled in Switzerland. The company is also characterized by a global and worldwide footprint, providing financial services in over 50 countries.

The company mainly operates through four divisions:

- Global Wealth Management: UBS is the world’s largest wealth manager, providing advice, solutions and services to families and individuals all around the world, including wealth planning, investment management, and both institutional and corporate financial advice.

- Personal & Corporate Banking: This business unit is a central element of UBS’s universal bank delivery model in Switzerland. It plays a supporting role for other business divisions by referring clients and growing the wealth of the firm’s private clients.

- Asset Management: UBS is a large-scale and diversified asset manager. Covering and operating in 22 countries, it offers investment capabilities and advice across all major traditional and alternative asset classes as well as platform solutions and advisory support to institutions, wholesale intermediaries, and wealth management clients. It is a leading fund house in Europe, the largest mutual fund manager in Switzerland and top foreign firm in China.

- Investment Bank: The IB unit is mainly focused on advisory services providing cross-asset research, along with access to equities, foreign exchange, precious metals and selected rates and credit markets. The Investment Bank is a crucial and key participant in capital markets flow activities, including sales, trading, and market-making across a range of securities.

Target – CREDIT SUISSE

- Founded in 1856, headquartered in Zürich, Switzerland

- CEO: Ulrich Körner

- Number of employees: 50,110

- Market Cap: $3.6bn (19/04/2023)

- LTM Revenue: $16.0bn

- LTM EBT: ($1.7bn)

- LTM P/BV: 0.1x

Credit Suisse sees its foundation in 1856 to fund the construction of Switzerland’s rail system. It also issued loans that helped create Switzerland’s electrical grid and the European rail system.

The company’s main services are widespread through four business divisions: Wealth Management, Investment Bank, Swiss Bank and Asset Management. These global and core divisions are complemented by four strong operating regions that are respectively: Switzerland, EMEA, APAC and Americas. This international approach helps reinforce the integrated model with global businesses and strong regional client accountability. It Is also worth underlining that Credit Suisse is a primary dealer and Forex counterparty of the Federal Reserve in the United States.

A relevant interpretation provided by eminent financial analysts, suggests that economic sanctions imposed by Switzerland on Russian individuals and businesses may have had a significant impact on the collapse of the bank. According to Bloomberg News, for example, Credit Suisse held about $33 billion for Russian clients, 50% more than UBS.

On 19th March 2023, fellow Swiss bank group UBS agreed to buy Credit Suisse for more than US$3 billion. The purchase of Credit Suisse by UBS has reportedly averted a greater crisis, according to SNB, preventing a chain collapse that could have affected the entire world’s banking system causing a crisis such as the one in 2008.

Deal Rationale

Both UBS and Credit Suisse have faced challenges in the current banking landscape, such as increased regulation, low interest rates, and the need to invest in technology and innovation. The acquisition was seen as an opportunity for the two banks to share resources and expertise to better navigate these challenges.

Credit Suisse’s decline has been a long time in the making. The bank had been connected to the collapse of two financial firms in 2021, Greensill Capital and Archegos Capital Management, which dealt the bank a significant financial blow. In addition to this, the bank has faced negative media attention in recent years for its reported dealings with clients with criminal backgrounds. The recent failure of Silicon Valley Bank sparked fear about the health of financial institutions worldwide, causing concerned investors to withdraw their funds from Credit Suisse and resulting in a sharp drop in stock prices. Despite a bailout from the Swiss National Bank worth over $68 billion US dollars, investors remain uneasy.

The acquisition is expected to improve the resilience and stability of the Swiss banking sector. The Swiss National Bank stated that the rescue would “secure financial stability and protect the Swiss economy” and that, along with the Swiss Federal Department of Finance and FINMA, the acquisition has their full support.

Overall, the acquisition of Credit Suisse by UBS aimed to create a stronger and more competitive entity in the global banking industry, driven by a combination of strategic, financial, and operational reasons. UBS CEO Ralph Hamers believes that bringing UBS and Credit Suisse together will enhance the bank’s ability to serve clients globally and deepen its best-in-class capabilities.

The acquisition of Credit Suisse by UBS was motivated by various reasons, including the creation of the world’s largest wealth manager, that would provide UBS with a significant advantage in the high-margin global wealth management (WM) industry. The move is being touted as a game-changer for the Swiss banking industry, as it will create a WM powerhouse that can compete with the likes of JPMorgan and Goldman Sachs. In addition, the acquisition would potentially lead to cost savings and synergies through the consolidation of their operations, which could enhance UBS’s profitability and ability to invest in growth areas. As mentioned before, the banking industry is facing increasing competition from fintech companies and other disruptors, which are challenging the traditional banking model. To remain competitive, banks need to invest in technology and digital infrastructure, which can be expensive. By acquiring Credit Suisse, UBS could potentially achieve cost savings through synergies and economies of scale, which would enable it to invest more in technology and stay ahead of its competitors.

Furthermore, the acquisition would strengthen UBS’s investment banking and trading businesses, especially in areas such as M&A advisory and equity capital markets, where Credit Suisse has a strong franchise. Additionally, the acquisition would allow UBS to expand its presence in Asia, particularly in China and Hong Kong, where Credit Suisse has a strong foothold, and accelerate its growth in the region. This is a significant opportunity for UBS, as the Asian market is expected to continue growing in the coming years.

In summary, the acquisition of Credit Suisse by UBS can be seen as a strategic move to consolidate UBS’s position as the world’s largest wealth manager, gain access to new markets, diversify revenue streams, and achieve cost savings. However, the combination of two such financial giants is not an easy matter, in fact, the acquisition also poses significant challenges and risks, and it remains to be seen whether UBS can successfully integrate Credit Suisse and realize the expected benefits.

Deal Structure

Negotiations regarding an acquisition began on the 15th of March. Swiss authorities asserted that a deal had to be done before the 20th of March, to stop the panic from spreading around the world. “If we as a country, where finance makes such a large part of GDP, are not able to send out a signal like that ‘we can stop this’ —then we can close down,” said one of the Swiss officials. “Nobody in the world will believe us any more.”

The acquisition was coordinated by the so-called Swiss “trinity” of the Federal Department of Finance, Swiss National Bank, and Swiss Financial Market Supervisory Authority (FINMA). The initial UBS offer on the morning of the 19th of March valued Credit Suisse at just 1 billion Swiss francs (i.e., 0.25 francs ($0.27) per share). The low price outraged the Mideast investors (three largest shareholders of Credit Suisse at that point are SNB part-owner Public Investment Fund, Olayan Group, and Qatar Investment Authority, together owning a quarter of the company). Later the same day UBS came up with a better offer of 0.50 francs ($0.55) per share, valuing Credit Suisse at just over $2 billion. Under pressure to get the deal done before the end of the very short deadline, the Swiss authorities threatened to remove Credit Suisse’s board if it did not sign off on the deal. Eventually, UBS agreed to boost its offer to 3 billion francs ($3.2 billion), at the same time negotiating for more support from the state (i.e., a liquidity line of 100 billion francs from the Swiss National Bank as well as a government guarantee for potential losses from risks associated with the transaction of up to 9 billion francs). The offer was accepted by the board of Credit Suisse prior to the opening of Asian financial markets on Monday morning.

President of Switzerland Alain Berset, Minister of Finance Karin Keller-Sutter, and Chairman Jordan alongside the chairmen of the two banks announced the acquisition in a 19 March 2023 press conference. The government said that its exposure to risk was low and considered the acquisition necessary for financial market stability in Switzerland and globally. Keller-Sutter emphasized that “This is no bailout. This is a commercial solution”.

According to the terms of the all-stock deal the Credit Suisse shareholders receive 1 UBS share for every 22.48 Credit Suisse shares they hold. The price still comprised just 1% of Credit Suisse’s record high value in 2007. Moreover, as part of the deal, FINMA ordered that the 16 billion francs ($17.2 billion) of additional tier 1 (AT1) bonds, a relatively risky class of bank debt, must be written down to zero. The move forced larger losses on bondholders than on shareholders of Credit Suisse and was done to placate international investors. It is important to note that previously, on the 19th of March 2023, the Swiss Federal Council exercised emergency powers to allow the merger to take place without the approval of shareholders. “AT1 holders were sacrificed so the finance ministry could try to save some face with international equity holders after denying them a vote on either side of the transaction,” says one of the bankers advising on the takeover.

Authors: Polina Mednikova, Lorenzo Villani, Akshay Shrivastava, Cleve Lim, Maddalena Salterini, Andrii Ovcharuk

Sources: Bloomberg, CNBC, Corriere Della Sera, Financial Times, Il Sole 24 Ore, Reuters, Swiss National Bank, The Economist, UBS, Wall Street Journal

You must be logged in to post a comment.